Shares of Constellation Brands, Inc. (NYSE: STZ) were up over 2% on Friday despite the company delivering mixed results for the third quarter of 2024 and slashing guidance for the full year. The stock has gained 15% over the past year. Here are some of the main points from the earnings report:

Mixed results

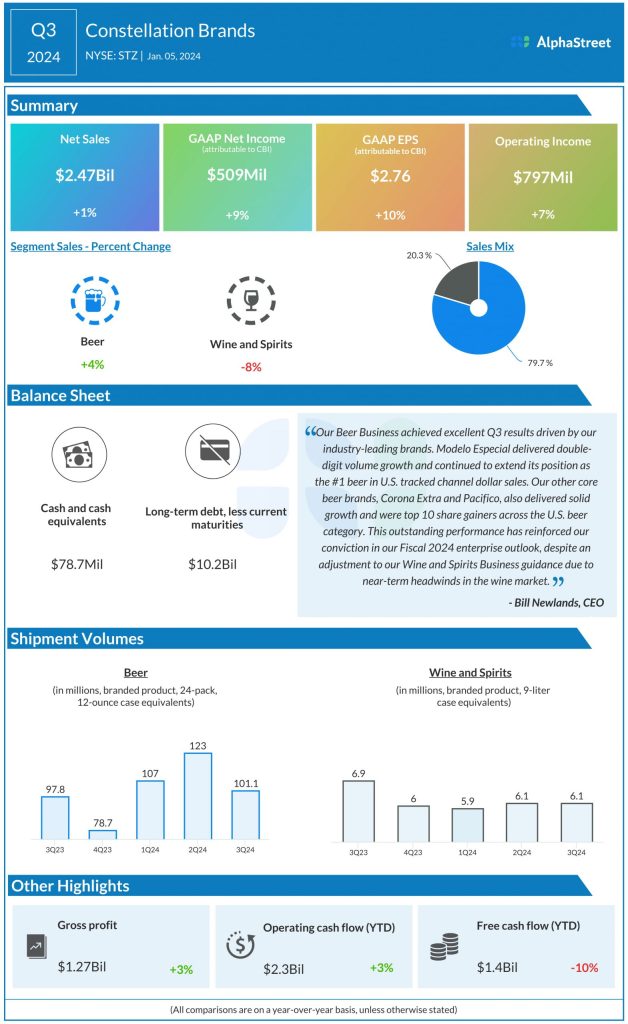

Constellation Brands reported net sales of $2.47 billion for the third quarter of 2024, which was up 1% year-over-year but below estimates of $2.54 billion. GAAP EPS rose 10% to $2.76. Comparable EPS increased 13% YoY to $3.19, beating projections of $3.00. Comparable EPS, excluding Canopy EIE, was $3.24.

Segment performance

The company’s Beer segment reported sales growth of 4% in Q3, driven by a 3.4% rise in shipments. Depletion volume grew 8.2%, fueled by strong demand across the portfolio. The segment benefited from gains in the Modelo Especial, Corona Extra, Pacifico, and Modelo Chelada brands. Modelo Especial, Pacifico, and Modelo Chelada posted double-digit volume growth during the quarter.

Constellation expects net sales to grow 8-9% for the Beer segment in fiscal year 2024. The company raised its outlook for operating income growth in this segment to 7-8% from the previous range of 6-7%.

On the flip side, the Wine and Spirits segment saw net sales decline 8% and organic sales decline 7% in the third quarter. Shipments were down 11.6% on a reported basis and 10.3% on an organic basis. Depletions decreased 10%. However, this segment saw strong performance from The Prisoner and Mi CAMPO brands during the quarter, and the DTC channel saw sales growth of 24%.

The company revised its outlook for this segment and now expects organic sales to decline 7-9% and operating income to drop 6-8% in FY2024. The updated guidance reflects broader marketplace deceleration and US wholesale underperformance.

Lowered outlook

Constellation slashed its reported EPS guidance for fiscal year 2024 to a range of $9.15-9.35 from the prior range of $9.60-9.80. At the same time, it reaffirmed its full-year guidance for comparable EPS, excluding Canopy EIE, of $12.00-12.20.