Shares of Mastercard Incorporated (NYSE: MA) stayed red on Monday. The stock has gained 8% year-to-date. The payments giant is set to report its earnings results for the third quarter of 2025 on Thursday, October 30, before market open. Here’s a look at what to expect from the earnings report:

Revenue

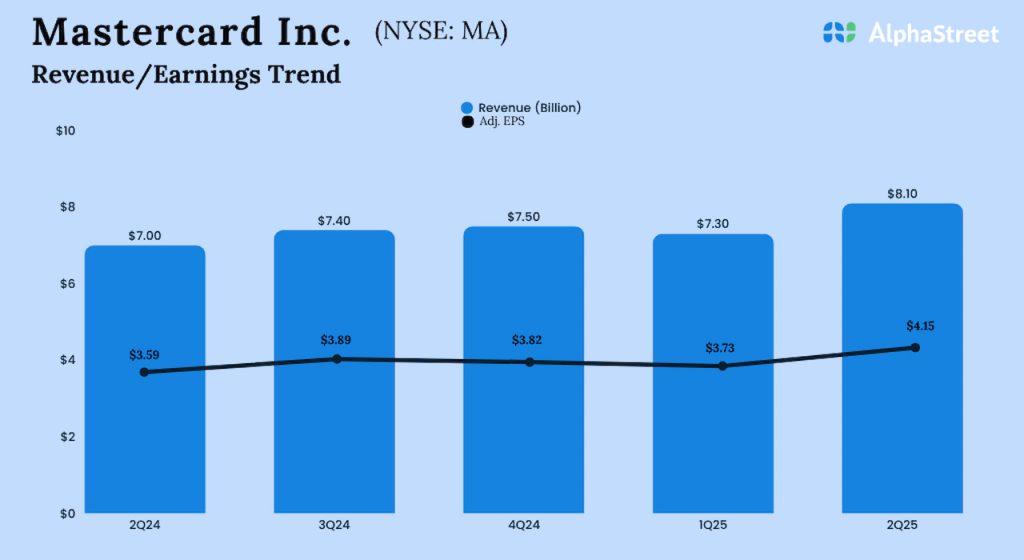

Analysts are projecting revenue of $8.53 billion for Mastercard in the third quarter of 2025, which represents a growth of 15% from the same period a year ago. In the second quarter of 2025, net revenue increased 17% year-over-year to $8.13 billion.

Earnings

The consensus estimate for earnings per share in Q3 2025 is $4.31, which implies a growth of nearly 11% from the prior-year quarter. In Q2 2025, adjusted EPS rose 16% YoY to $4.15.

Points to note

Mastercard expects net revenue growth in the third quarter, on a currency-neutral basis, to be at the high end of a low double-digits range, excluding acquisitions. In Q2, revenue grew 16% on a currency-neutral basis, driven by growth in its payment network and value-added services and solutions. The top line benefited from growth in gross dollar volume, cross-border volume, and switched transactions. This momentum is likely to have continued in the third quarter.

Mastercard anticipates consumer and business spending to remain healthy through fiscal year 2025. The company is expected to benefit from its portfolio, which is well-diversified across geographies as well as travel and non-travel spending. Its fee-based business model allows it to stay resilient in times of economic uncertainty.

The credit card company is expected to benefit from its partnerships with companies like American Airlines and Uber, as well as the launch of new programs in additional markets such as the UK and Germany. It is working on enhancing the customer experience, which in turn will help drive brand preference and incremental spend. It is also upgrading its value proposition with a set of premium benefits aimed at its affluent customers, who, on average, have higher spending patterns.

In addition, MA is investing in technological capabilities that help make transactions faster, easier and safer. These factors are expected to have benefited its performance in the to-be reported quarter.