Last week Conagra Brands (NYSE: CAG) and McCormick & Company (NYSE:MKC) reported their quarterly earnings results. Both food companies witnessed sales growth helped by pricing actions even as they faced pressures from inflation and supply chain headwinds. Here are a few trends to note from their quarterly performances:

Customer preferences

During the pandemic, people turned to having more meals at home and in the current environment, inflation seems to have made them stick to this trend. In this scenario, consumers are looking for healthy, flavorful and convenient meal options. These preferences drove demand for Conagra’s and McCormick’s products during their recent quarters.

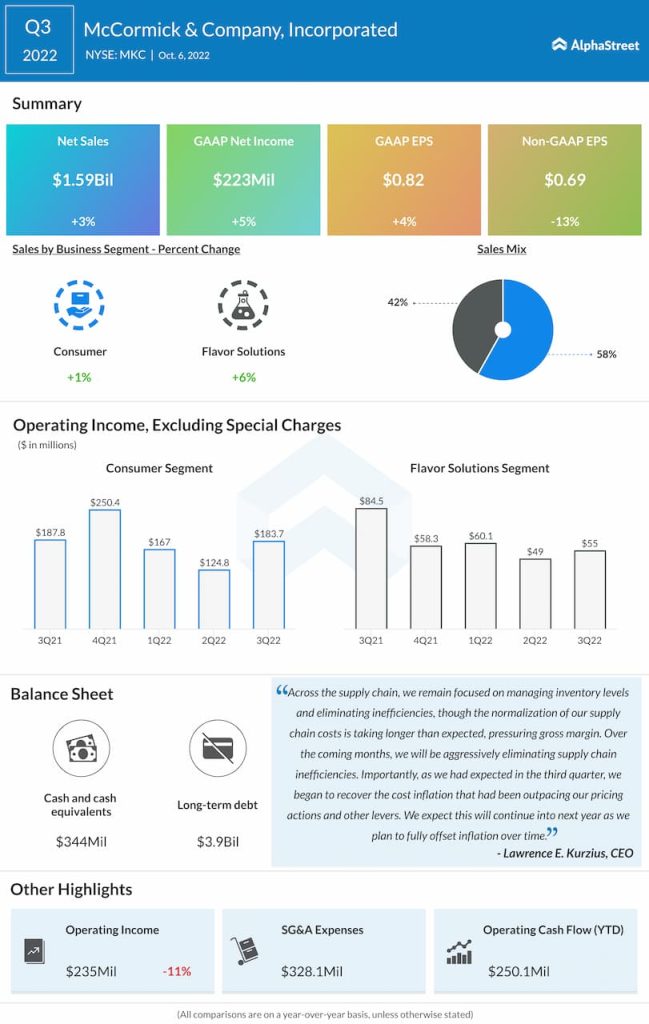

Conagra’s net sales rose 10% year-over-year to $2.9 billion for its first quarter of 2023. The company saw strong retail sales growth in its Frozen, Snacks, and Staples categories led by demand for single-serve meals, dinners and entrees, as well as plant-based protein, canned tomatoes, and microwave popcorn. McCormick saw net sales increase 3% YoY to $1.6 billion for its third quarter of 2022, driven by strong demand for herbs, spices and seasonings.

Inflation and pricing

Both food companies felt the pinch of inflation during their respective quarters as higher costs weighed on their profits and margins. Conagra’s gross margin dropped 58 basis points to 24.8% while its adjusted operating margin fell by 40 basis points to 13.7% in Q1 2023. However, a 7% growth in gross profit along with higher sales helped drive a 14% increase in adjusted EPS during the first quarter.

Higher cost inflation led to McCormick’s gross profit margin dropping by 320 basis points in Q3 2022. This gross margin compression caused an 11% decline in operating income. Adjusted EPS dropped 13% during the quarter due to lower adjusted operating income.

Both Conagra and McCormick rolled out price increases to tackle inflation, which helped drive sales growth but resulted in volume declines. Looking ahead, both companies expect inflation to persist through the remainder of their respective fiscal years.

Conagra expects the inflationary environment to continue but moderate through calendar year 2023, resulting in a low-teens inflation rate for FY2023 weighted towards the first half. The company also expects to see volume declines in Q2 2023 as recent pricing actions take effect.

McCormick expects its profits for FY2022 to be impacted by cost inflation. While sales are expected to increase due to pricing actions, volumes are anticipated to decline. The company expects pricing to outpace inflation in the second half of the year and continue into next year.

Supply chain

Conagra and McCormick both faced supply chain headwinds during their respective quarters which in turn impacted their margins. Conagra continues to make progress on its supply chain productivity initiatives although a full normalization is yet to be achieved. The company expects its Q2 2023 volumes to be impacted by supply chain disruptions.

McCormick remains focused on managing its inventory levels and eliminating inefficiencies across its supply chain although the normalization of supply chain costs are taking longer than expected, which in turn is putting pressure on gross margin and profit realization. The company expects supply chain headwinds to impact its bottom line for FY2022.

Click here to read the full transcripts of Conagra’s and McCormick’s latest earnings conference calls