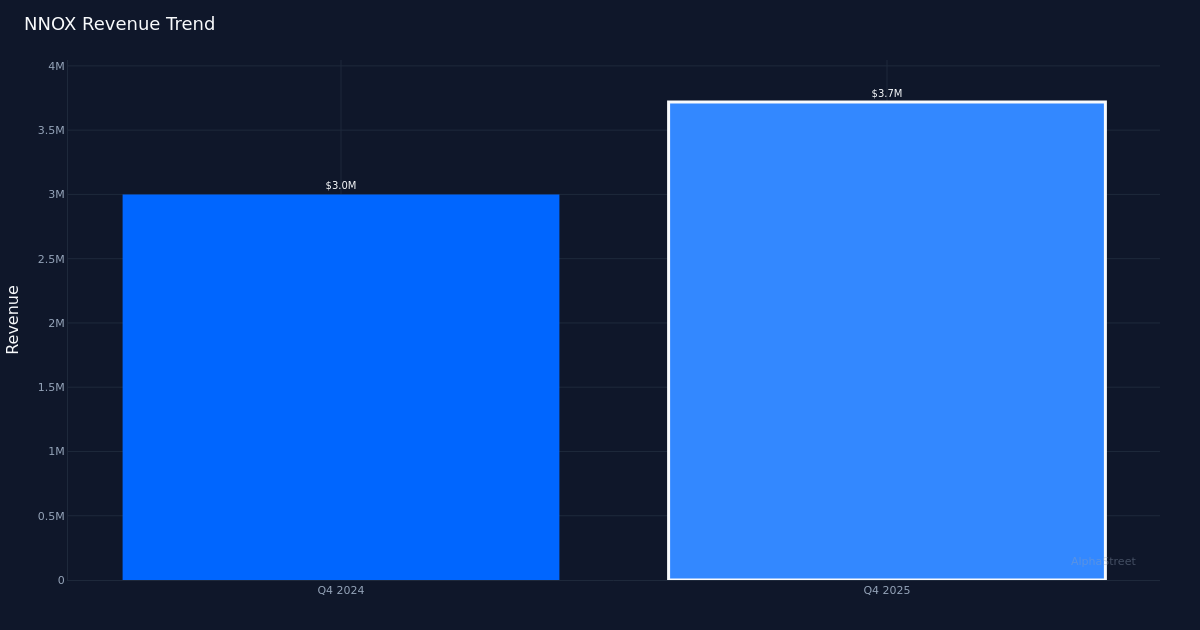

Better-than-Expected Quarter. Nano-X Imaging Ltd. (NASDAQ:NNOX) reported a Q4 2025 non-GAAP loss per share of $0.17, beating analyst estimates of a $0.20 loss by 15.0%. The medical device company posted revenue of $3.7M for the quarter, representing 24.0% growth from $3.0M in the year-ago period. The stock responded favorably, climbing 5.2% to $2.85 on the results as investors welcomed the narrower-than-expected loss and accelerating top-line momentum.

Deployment Progress Continues. The quarter saw Nano-X deploy 36 units of its Nanox.ARC systems, bringing the company’s total operational footprint to 36 systems at quarter end. This deployment metric represents tangible progress in the company’s strategy to commercialize its novel X-ray technology platform, which aims to disrupt traditional medical imaging with a lower-cost, AI-enabled alternative. The 24.0% revenue expansion suggests the installed base is beginning to generate meaningful recurring revenue streams, though the company remains in early-stage commercialization mode as it builds out its imaging-as-a-service model.

Path to Profitability. The bottom line showed a net loss of $11.2M for the quarter, though the narrower-than-expected loss per share suggests improving operational leverage as the business scales. The beat appears primarily driven by better expense management rather than a significant revenue surprise, which is typical for early-stage medical device companies still investing heavily in market development and regulatory expansion. As deployment volumes increase, the company will need to demonstrate that unit economics can support a path to cash flow breakeven while maintaining the pace of system placements.

Full-Year Outlook. Management provided full-year guidance calling for revenue of $35.0M, establishing a clear benchmark for investors to track execution through 2026. This guidance implies significant sequential acceleration from the $3.7M quarterly run rate, suggesting management anticipates a material ramp in both system deployments and utilization revenue as the installed base matures. The guidance will be critical for maintaining investor confidence as the company transitions from pilot deployments to scaled commercialization.

Wall Street Support. The analyst community maintains a constructive stance with a consensus of 6 buy ratings and 1 hold rating, reflecting optimism about the company’s disruptive potential in the medical imaging market. The 5.2% post-earnings rally suggests investors are encouraged by the operational progress and tightening losses, though the stock remains under pressure at current levels as the market awaits proof of sustainable revenue growth and a credible timeline to profitability.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.