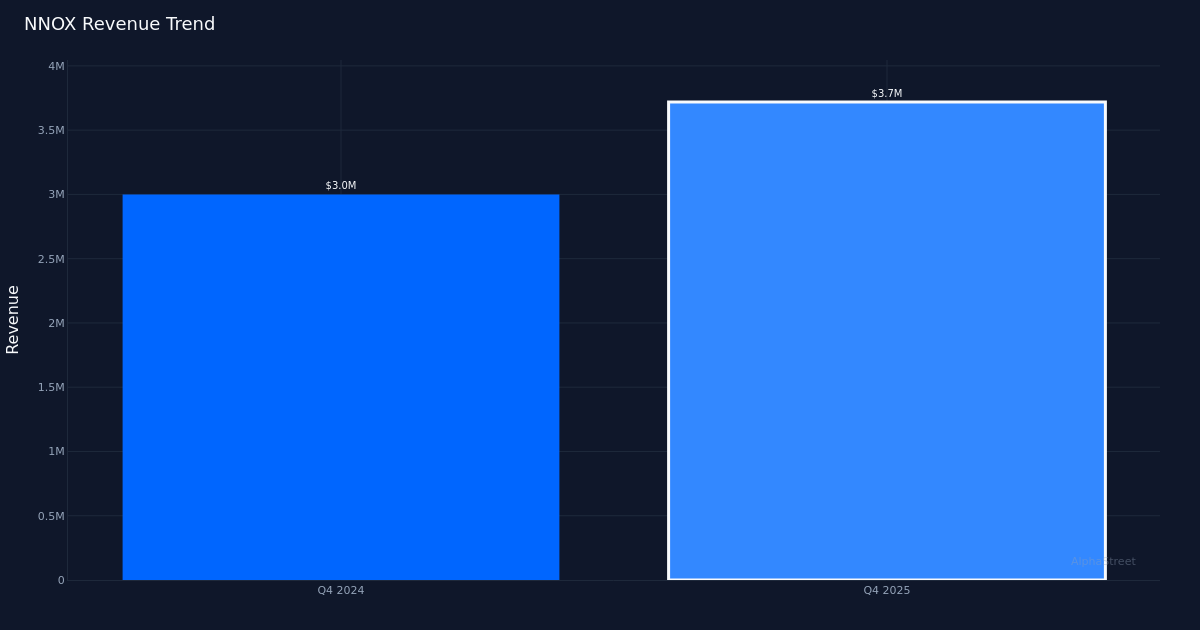

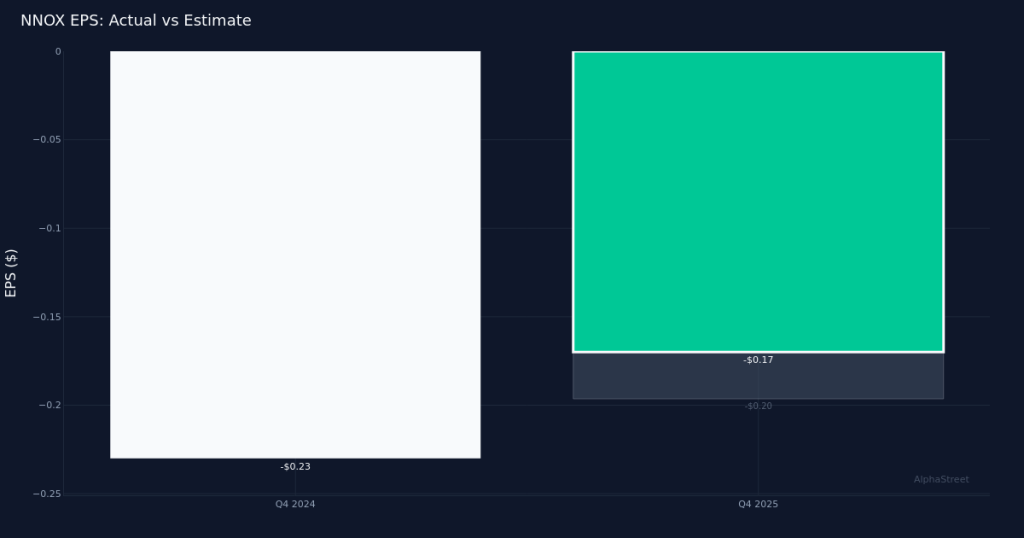

Nano-X Imaging topped expectations with a narrower-than-expected loss in Q4 2025, but the quality of the beat reveals deeper structural challenges masked by non-operating items. The medical device maker posted a loss of $0.17 per share versus the $0.20 loss anticipated by analysts, representing a beat by 15.0%. While the company delivered its first earnings surprise in recent quarters—achieving a 100% beat rate over the last quarter—the underlying fundamentals paint a more complex picture than the headline number suggests. Revenue reached $3.7M for the quarter, up 23% year-over-year, yet the company’s margin structure deteriorated significantly despite the top-line expansion.

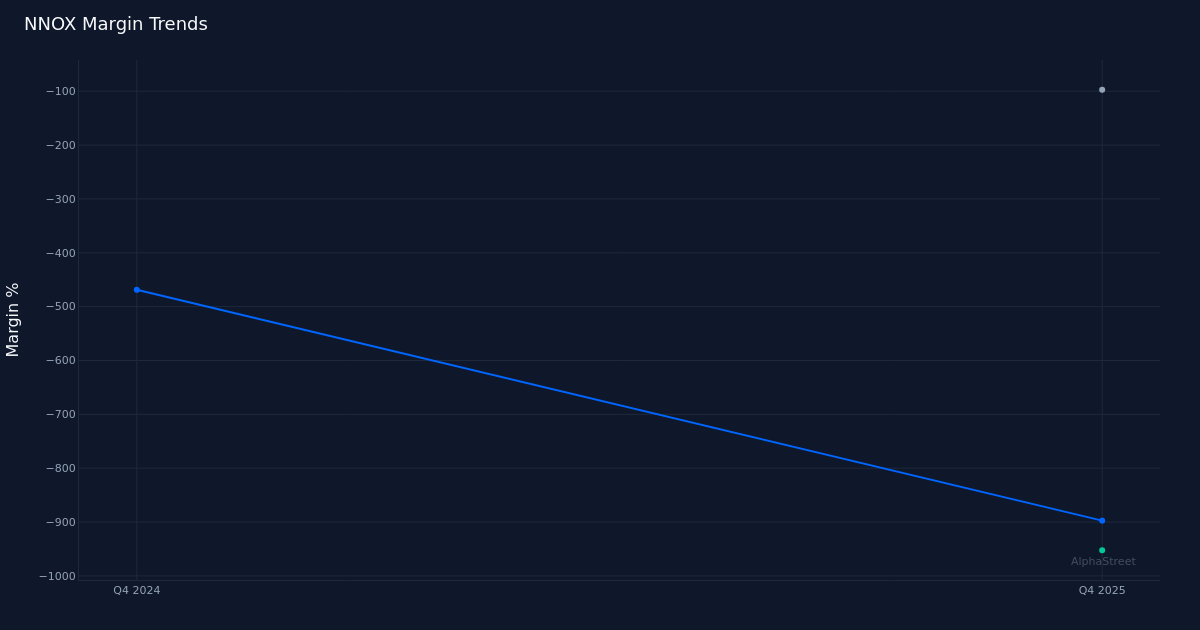

The earnings quality analysis reveals a troubling disconnect between revenue growth and profitability metrics. While revenue expanded from $3.0M in Q4 2024 to $3.7M in the current quarter, gross margin plunged to -97%, indicating the company lost nearly a dollar on every dollar of revenue generated at the gross profit level. The net margin of -902.7% compared to -470.0% a year ago represents a compression of 432.7 percentage points, suggesting the business model remains far from economic viability despite scaling efforts. Operating margin deteriorated to -957.2%, with operating loss registering at $35.4M. Management acknowledged the margin pressure, noting “The increase was also due to an increase of $0.7 million in the gross loss, increase of $1.1 million in the sales and marketing expenses and increase of $1.4 million in other expenses.”

Revenue composition reveals diversification efforts are beginning to bear fruit, albeit from a low base. Management attributed the growth to multiple sources, explaining “The increase of $0.7 million, increase of 23% in the revenues, stems from an increase of $0.3 million in our revenue from the teleradiology services and an increase of $0.4 million in our revenue due to the consolidations of Nano-X Health IT Inc.” The teleradiology services expansion and the Health IT consolidation together account for the full year-over-year increase, suggesting the company is broadening its revenue streams beyond pure hardware sales. The deployment metric of 36 Nanox.ARC systems provides a tangible indicator of market penetration, though the relatively modest installed base underscores the early-stage nature of commercialization.

Management’s FY 2026 guidance implies a dramatic inflection that will require scrutiny. The company guided to $35.0M in revenue for the full year 2026, which would represent a nearly tenfold increase from the quarterly run rate of $3.7M. An analyst probed this during the call, asking “when we look at the guidance for 2026, the $35 million, which is strong growth, can you talk about the cadence throughout the year?” The magnitude of implied acceleration suggests either a massive deployment ramp, significant one-time contracts, or additional M&A consolidation—none of which have been quantified in the available data. This guidance gap presents execution risk that investors will need to monitor closely through 2026.

Non-operating items significantly distorted reported results and obscure underlying operational performance. CFO Ran Daniel disclosed a major non-cash charge, stating “Besides the impairment expense that we recorded in 2025, which was the impairment of mainly whatever is related to the chip line in the Korean fab, which was amounted to $17.5 million in the non-cash expense.” This impairment alone exceeds annual revenue guidance and suggests writedowns of manufacturing infrastructure. The presence of such large non-cash charges makes it difficult to assess true operational cash burn and raises questions about prior capital allocation decisions.

Market reaction. At current levels, the market is pricing in successful execution of the multi-fold revenue ramp while discounting the margin deterioration and capital intensity questions raised by the Korean fab impairment. The valuation multiple on forward guidance appears modest, but only if management can bridge the gap between current quarterly revenue of $3.7M and full-year targets of $35.0M.

The path forward hinges on demonstrating unit economics at scale and managing cash consumption. With 36 systems deployed and gross margins deeply negative, each incremental deployment currently destroys value at the gross profit level. The company must demonstrate that these economics improve dramatically with scale, or that the teleradiology and IT services revenue streams carry materially different margin profiles. The sales and marketing expense increases referenced by management suggest continued investment in market development, which is appropriate for a growth-stage company but extends the timeline to profitability.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.