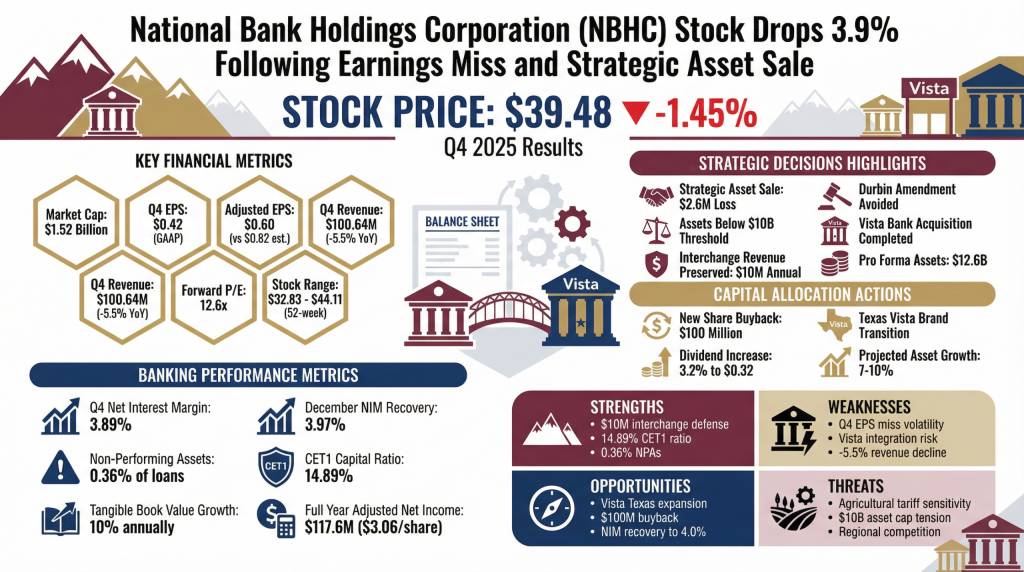

Strengths

- Interchange Revenue Defense: Strategic asset management preserved $10 million in annual fee income by staying below the $10 billion threshold.

- Capital Ratios: Strong CET1 capital ratio of 14.89% and 10% annual growth in tangible book value.

- Asset Quality: Non-performing assets (NPA) improved to a low 0.36% despite recent credit actions.

Weaknesses

- Earnings Volatility: “Noisy” Q4 with multiple one-time charges leading to a significant EPS miss.

- Integration Risk: Q3 2026 systems conversion for Vista Bank remains a critical execution hurdle.

- Revenue Growth: Sluggish 5.5% year-over-year revenue decline in the most recent quarter.

Opportunities

- Vista Brand Expansion: Scaling the relationship-banking model into high-growth markets like Austin and Dallas.

- Shareholder Returns: New $100M buyback authorization and dividend increase provide a floor for shareholder value.

- NIM Recovery: Projected 2026 NIM of ~4.0% as deposit costs stabilize.

Threats

- Tariff Sensitivity: Indirect exposure to agricultural and manufacturing borrowers sensitive to trade policy inflation.

- Asset Thresholds: Operating near the $10B asset cap creates ongoing tension between growth and fee-income retention.

- Regional Competition: Intense rivalry for low-cost deposits in the Mountain West and Texas markets.