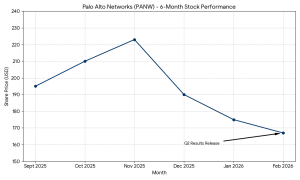

Shares of Palo Alto Networks (NASDAQ: PANW) fell 5.2% to $167.00 in early Wednesday trading after the cybersecurity leader issued a mixed financial outlook that overshadowed a second-quarter earnings beat. The stock currently trades approximately 25% below its 52-week high of $223.61, reflecting a broader 11% decline year-to-date as investors recalibrate expectations for software-as-a-service (SaaS) growth.

For the fiscal second quarter ended Jan. 31, 2026, Palo Alto Networks reported total revenue of $2.59 billion, a 15% increase from $2.26 billion in the same period last year. This figure narrowly exceeded the Zacks Consensus Estimate of $2.58 billion. Non-GAAP net income reached $1.03 per diluted share, surpassing analyst expectations of $0.94 and up from $0.81 a year ago.

Quarterly metrics and margins

The company’s shift toward “platformization”—integrating various security tools into a single interface—remained a primary driver. Next-Generation Security (NGS) Annual Recurring Revenue (ARR) grew 33% year-over-year to $6.33 billion. Remaining performance obligation (RPO), a key indicator of future revenue, rose 23% to $16.0 billion.

Profitability remained a highlight, with the company reporting its third consecutive quarter of non-GAAP operating margins above 30%. The non-GAAP operating margin for the quarter was 30.3%, up 190 basis points from the prior year. GAAP net income rose to $432 million, or $0.61 per diluted share, compared to $267 million, or $0.38 per diluted share, in the year-ago quarter.

Future Guidance

The market reaction was primarily fueled by the company’s third-quarter guidance. While Palo Alto raised its full-year revenue forecast to a range of $11.28 billion to $11.31 billion—up from a previous $10.52 billion estimate—it projected Q3 non-GAAP earnings per share between $0.78 and $0.80. This outlook fell short of the $0.92 consensus estimate, signaling potential margin pressure or increased investment costs in the near term.

For the full fiscal year 2026, the company expects:

- Total Revenue: $11.28 billion to $11.31 billion (22%–23% growth).

- NGS ARR: $8.52 billion to $8.62 billion (53%–54% growth).

- Non-GAAP Operating Margin: 28.5% to 29.0%.

- Adjusted Free Cash Flow Margin: 37%.

Sector Context

The results come amid a cautious environment for enterprise software. While cybersecurity is often viewed as a “must-have” expense, high interest rates and macroeconomic uncertainty have led some enterprises to consolidate vendors or delay large-scale IT transformations.

Analysts noted that while the “platformization” strategy is winning larger deals—including a new $40 million agreement with a leading IT services firm—it can lead to longer sales cycles. There were no immediate rating downgrades following the release, though several firms adjusted price targets to reflect the lower EPS guidance. Zacks Investment Research currently maintains a “Sell” rating on the stock, citing valuation concerns relative to the lowered earnings outlook.

CEO Nikesh Arora attributed the growth to AI-driven demand, stating that customers are modernizing their stacks to align with AI security needs. The company also confirmed the completion of its acquisitions of CyberArk and Chronosphere during the period to bolster its identity security and observability capabilities.