Shares of PepsiCo, Inc. (NASDAQ: PEP) gained over 6% on Thursday after the company beat expectations on both revenue and earnings for the second quarter of 2025. The beverage giant also maintained its revenue outlook for the full year but revised its guidance for core earnings per share. Here are the key takeaways from the earnings report:

Results beat estimates

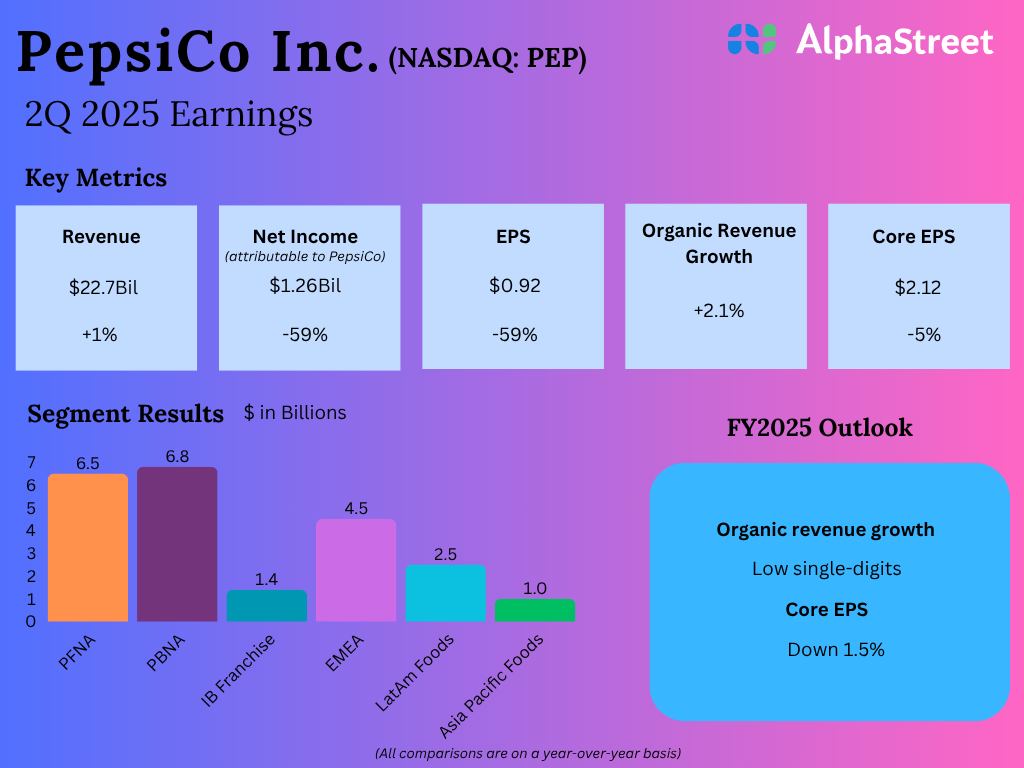

PepsiCo’s net revenue inched up 1% to $22.7 billion in Q2 2025 compared to the prior-year period, beating estimates of $22.3 billion. GAAP earnings per share decreased 59% year-over-year to $0.92. Core EPS declined 5% on a constant currency basis to $2.12, but surpassed projections of $2.03.

North America improvement and international strength

During the second quarter, PepsiCo witnessed continued momentum in its international business and improvement in its North America business even as it faced a challenging macroeconomic environment.

In North America, although category demand remained muted, the company saw improvement in organic volume trends in convenient foods and beverages. The strength in beverages was led by Pepsi, with continued gains from Pepsi Zero Sugar. PEP continues to work on driving growth through product innovation, partnerships and an increased focus on healthier options.

In Q2, PepsiCo completed the acquisition of poppi, a prebiotic, modern soda business with strong retail sales. This acquisition is expected to expand the company’s beverages portfolio and its reach with younger consumers.

The international business saw organic revenue growth of 6% in Q2. Organic revenues in the beverages business increased 9%, helped by strength in markets like Mexico, Germany, Poland and France. The convenient foods business recorded organic revenue growth of 4%, led by gains in markets like Mexico, Brazil, Colombia and India.

Outlook

PepsiCo expects its business to stay resilient through the remainder of fiscal year 2025, helped by strength in its international business and improvement in its North America business.

For FY2025, PEP continues to expect a low-single digit increase in organic revenue. Core constant currency EPS is expected to be approx. even with the prior year. However, the company now expects core EPS to decline 1.5% for the year versus its previous expectation of a 3% decline.