After the upbeat June-quarter performance, PepsiCo (NASDAQ: PEP) had predicted mixed prospects for the second half of the year, citing the continuing slump in the soda segment and stable demand for snacks. The soft-drink behemoth will be publishing its third-quarter report Thursday before the opening bell.

The market’s consensus revenue estimate of $16.93 billion represents a 2.7% year-over-year increase. It is estimated that earnings declined to $1.50 per share in the September-quarter from last year’s $1.59 per share.

Investors will be closely following the event as a gauge to evaluate the performance of Ramon Laguarta, who became the CEO almost a year ago. The earnings report will likely give yet another boost to the company’s stock, like in the past when the results regularly topped expectations, all along adding to shareholder value.

Product Portfolio

The management’s ongoing efforts to diversify the product portfolio, amid the slowdown in the sales of soda-based drinks, might influence the upcoming results. Recent innovations and partnerships, such as the tie-up with Lavazza in the UK market for iced coffee, might strengthen organic revenue growth this time.

The stable growth of the snack business, combined with the management’s cost-saving measures, will add to profitability. It is anticipated that the soda business would bounce back in the coming months helped by cost-cutting initiatives and favorable pricing.

Long-term Plans

Going ahead, the steps being taken by the management to revamp the business, such as enhancing productivity and incorporating new technology, will streamline the operations. International expansion, especially in Asia where the company is focusing on local flavors, brightens the long-term prospects.

The move assumes significance considering the concerns that PepsiCo is depending too much on the North American market. Meanwhile, the positive factors might be partially offset by the high costs associated with the business reorganization and unfavorable currency exchange rates.

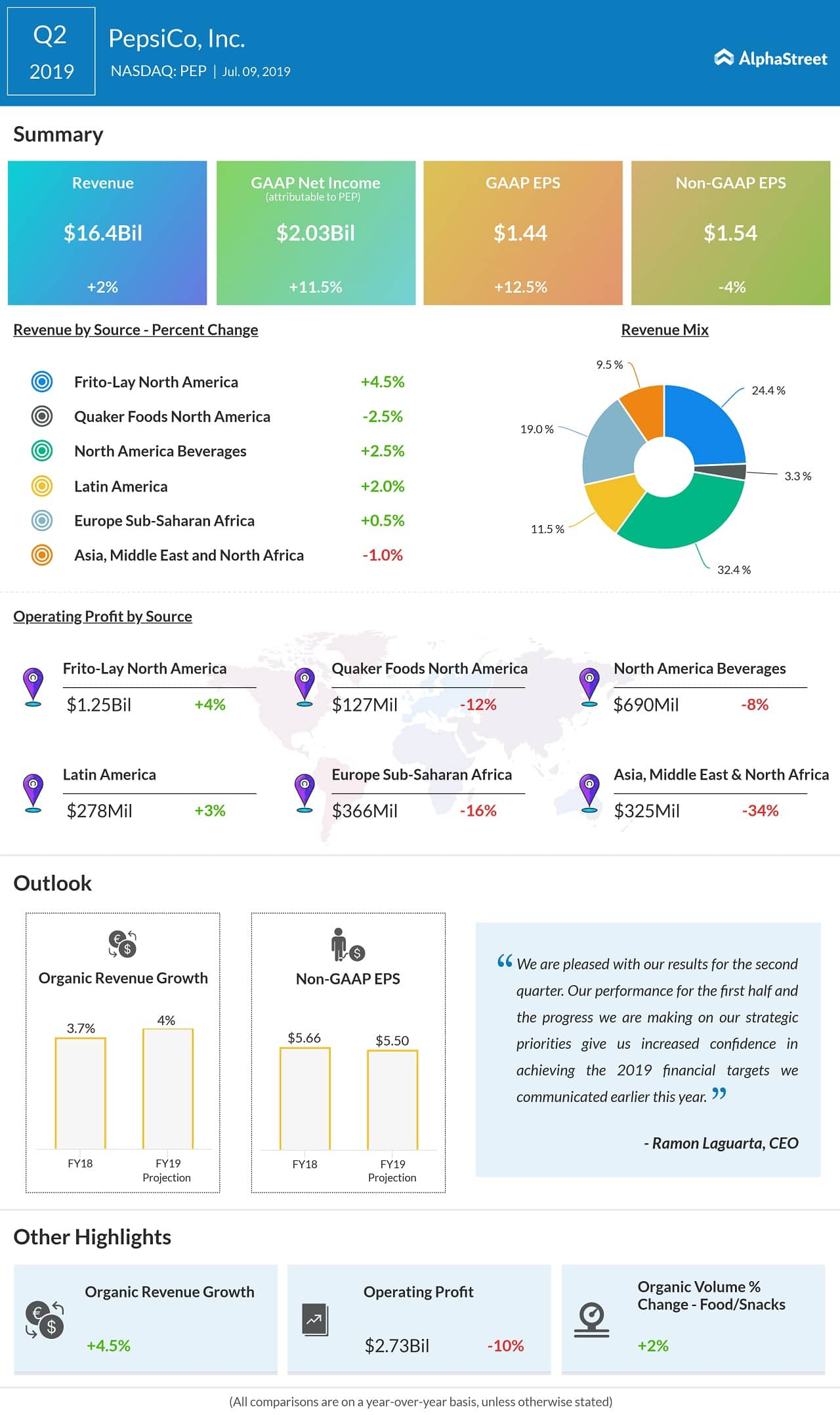

In the second quarter, all the major product categories and geographical regions registered growth, led by the snack business, lifting total revenues by 2% to $16.4 billion. In contrast, earnings dropped 4% to $1.54 per share but topped the estimates.

Competition

Rival beverage company Coca-Cola (KO) is scheduled to unveil its third-quarter numbers on October 18 before the opening bell. Market watchers predict a 2% dip in earnings to $0.56 per share.

Also see: Pepsico Q1 2019 Earnings Conference Call Transcript

Earlier this month,

PepsiCo shares climbed to an all-time high, after staying on the

growth path consistently. Having gained 25% since the beginning of

the year, the stock continues to outperform the market.