Shares of Philip Morris International Inc. (NYSE: PM) were down 3.3% on Tuesday after the company delivered mixed results for the second quarter of 2021. While the tobacco giant managed to beat earnings estimates, its revenue fell short of expectations. The company also cut its reported earnings forecast for the full year. The company is increasing its focus on smoke-free products and has made some prudent acquisitions as part of these efforts.

Q2 numbers

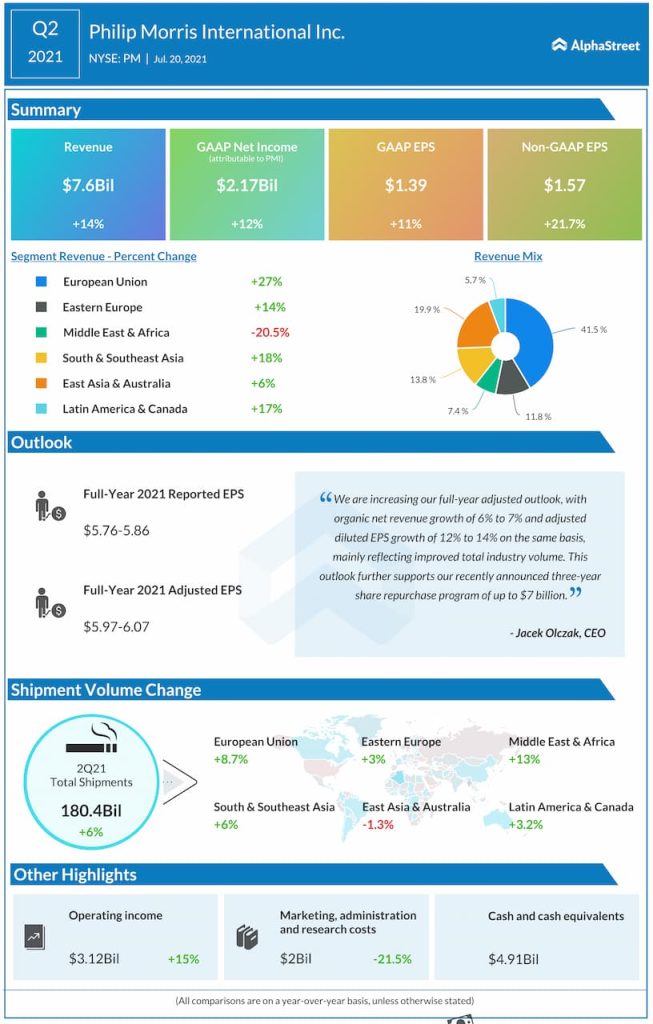

Revenues increased 14.2% year-over-year on a reported basis and 7.9%, excluding currency, helped by favorable volume/mix and pricing. The company benefited from higher heated tobacco unit volume, mainly in the European Union, and higher cigarette volume in Indonesia, Italy and Spain. GAAP EPS rose 11% to $1.39 while adjusted EPS increased nearly 22% to $1.57.

Outlook

Philip Morris cut its full-year 2021 GAAP EPS guidance to a range of $5.76-5.86 from the previous range of $5.93-6.03 mainly reflecting adverse impacts from the Saudi Arabia customs assessments as well as other asset impairment costs. Adjusted diluted EPS is estimated to increase 12-14% to a range of $5.97-6.07 and organic revenue is projected to grow 6-7% reflecting an improvement in total industry volume.

The company anticipates that many of its key markets will emerge from the pandemic-related restrictions for the most part during the second half of the year. In markets such as the Philippines and Indonesia where challenges remain, the company does not expect the situation to deteriorate significantly from the current level. The uncertainty surrounding global travel is likely to take a toll on PMI’s duty-free business.

PMI assumes total cigarette and heated tobacco unit shipment volume progression to be in the range of approx. flat to up 2%. Heated tobacco unit shipment volume is expected to be 95 to 100 billion units. For the third quarter of 2021, Philip Morris expects reported EPS to range between $1.50-1.55.

Beyond Nicotine

Philip Morris is focusing more on smoke-free products and the company aims to generate at least $1 billion in annual net revenue from Beyond Nicotine products by 2025. The Beyond Nicotine strategy focuses mainly on botanicals and inhaled therapeutics, which are expected to have an addressable market of around $65 billion by 2025.

As part of these efforts, Philip Morris announced the acquisitions of Fertin Pharma and Vectura Group. These deals are expected to help PMI expand its capabilities in inhaled and oral product formulations.

Fertin produces lozenges, gum and pouches that can be applied in oral nicotine and beyond nicotine areas for selfcare wellness products while Vectura is a provider of inhaled drug delivery solutions. These acquisitions will help PMI broaden the reach of its smoke-free alternatives to smokers around the world.

Click here to read the full transcript of Philip Morris Q2 2021 earnings conference call