Shares of Philip Morris International Inc. (NYSE: PM) were down 1% on Thursday despite the company beating expectations on its third quarter 2022 earnings results and making two huge announcements. PMI struck an agreement with Altria (NYSE: MO) to acquire the US commercialization rights for IQOS and it increased its offer to buy Swedish Match. These deals will provide an advantage as the company furthers its goals in the smoke-free market.

Quarterly performance

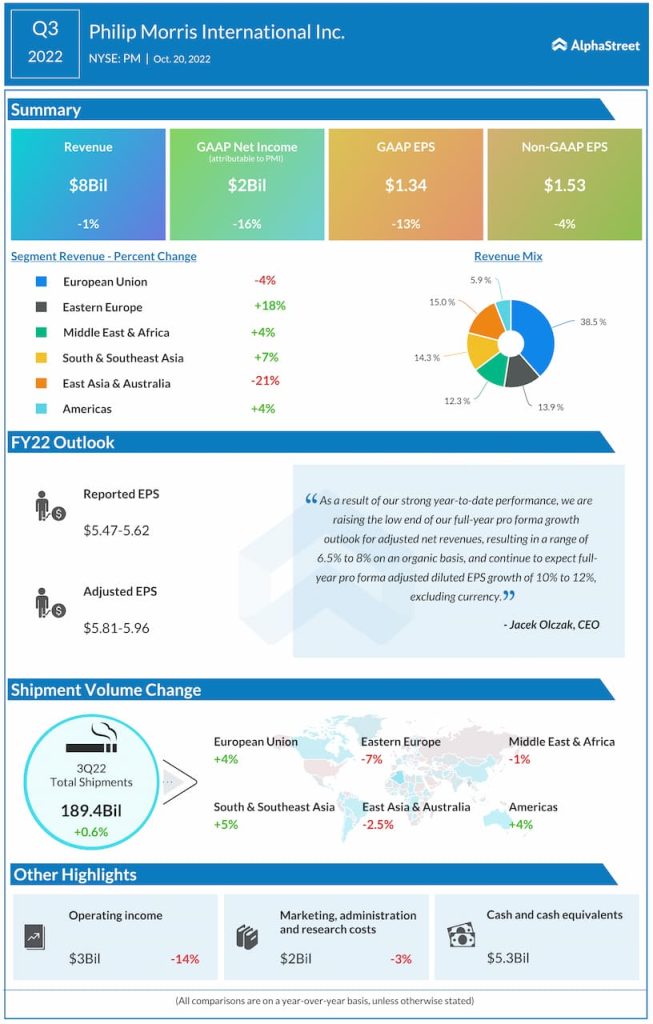

In Q3 2022, revenues declined 1.1% to $8 billion while adjusted EPS dropped 4% to $1.53. Despite the year-over-year decreases, both the top and bottom line numbers beat expectations. Total shipment volume increased 0.6%, driven mainly by a 17.1% increase in HTU shipments. Operating income decreased by 14.1% during the quarter. On an organic basis, revenues increased 6.7%.

Altria and the IQOS deal

Philip Morris has entered into an agreement with Altria to acquire the full rights to commercialize IQOS in the US. Under the terms, PMI will pay a total cash consideration of $2.7 billion. Of this, $1 billion was paid at the inception of the agreement and the remaining $1.7 billion will be paid by July 2023. The companies’ partnership on IQOS will end on April 30, 2024.

PMI is way ahead with its commercialization plans for IQOS in the US, which include full-scale launches in key cities and regions and then building a national presence. The company believes that IQOS heat-not-burn products could account for around 10% of total US cigarettes and heated tobacco unit volume by 2030.

Revised offer for Swedish Match

Philip Morris raised its offer price to buy Stockholm-based oral nicotine pouches maker Swedish Match. The company is now offering SEK 116 in cash per share versus its previous offer of SEK 106 per share. The deal is now estimated to be valued at around $15.8 billion. The revised offer takes into account the impacts from the strengthening US dollar. This will be PMI’s final offer and the company expects the transaction to close in the fourth quarter of this year.

IQOS and smoke-free opportunity

PMI saw strong performance from IQOS in Q3, with 22% growth in pro forma HTU shipment volumes. The company estimates there were approx. 19.5 million IQOS users as of September 30, excluding Russia and Ukraine, which reflects growth of around 0.5 million users in Q3.

In its conference call, PMI stated that the US is the world’s biggest accessible nicotine market by retail value. The company sees substantial opportunity in the US for IQOS due to demand for smoke-free alternatives to cigarettes. PMI believes a volume share of 10% of cigarettes and HTUs by 2030 is achievable with further expansion potential.

Outlook

For the full year of 2022, on a pro forma basis, Philip Morris expects total shipment volumes to grow 2-3% and organic net revenues to grow 6.5-8.0%. Pro forma adjusted EPS is expected to range between $5.22-5.33.