PIPR Stock Surges Following Record Quarterly Performance

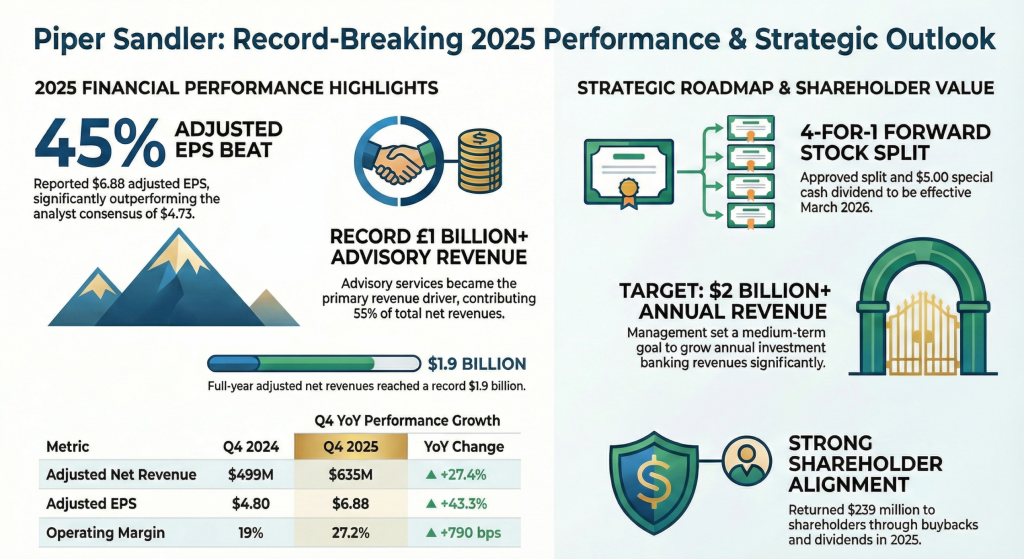

Shares of Piper Sandler Companies (PIPR) rose approximately 10% (up ~$33 to around $365 range in trading on Friday) after the investment bank reported fourth-quarter and full-year 2025 results that significantly exceeded market expectations. The stock traded within its 52-week range of $202.91 to $380.26, having trended upward strongly in recent sessions. The gain followed a reported $6.88 adjusted EPS, surpassing the analyst consensus of approximately $4.73 (a beat of over 45%).

Company Description: Piper Sandler Companies is a middle-market investment bank and institutional securities firm. It provides financial advisory services, M&A advisory, equity and debt capital markets products, public finance services, and institutional brokerage. The firm focuses on seven core sectors: healthcare, financial services, energy and power, consumer, services and industrials, technology, and chemicals. Its primary end markets include corporations, private equity groups, public entities, and institutional investors in the United States and internationally.

Current Stock Price: ~$365 (as of midday February 6, 2026, post-earnings reaction)

Market Capitalization: Approximately $6.46 billion

Valuation: Piper Sandler trades at a trailing P/E ratio in the mid-to-high 20s post-beat (adjusted for recent earnings strength). This reflects a premium for record advisory performance, though tempered by the cyclical nature of investment banking and capital markets activity.

Record Advisory Revenue Drives 22% Annual Growth

Piper Sandler reported record fourth-quarter adjusted net revenue of $635 million, up 27.4% from the prior-year period. For the full year 2025, adjusted net revenues reached $1.9 billion, a 22% increase year-over-year (GAAP net revenues ~$1.90 billion, up ~24%). Advisory services became the largest revenue driver, generating a record over $1 billion for the year, representing approximately 55% of total net revenues.

| Metric | Q4 2024 | Q4 2025 | YoY Change |

| Adjusted Net Revenue | ~$499M | $635M | +27.4% |

| Adjusted EPS | $4.80 | $6.88 | +43.3% |

| Operating Margin | ~19% | 27.2% | +790 bps |

| Full Year Adjusted Revenue | ~$1.54B | $1.9B | +22% |

Calculated/derived from reported figures and YoY changes.

Investment banking revenues contributed strongly in the quarter, with full-year corporate financing up significantly (e.g., 122 completed financings). Equity brokerage reached an all-time high. The firm ended 2025 with an operating margin of 21.9%, up notably as compensation ratios improved to 61.4% for the year (with Q4 at ~60.1%).

Analyst Forecasts and Capital Returns

Following the earnings beat, the board approved a special cash dividend of $5.00 per share (plus regular quarterly $0.70) and a 4-for-1 forward stock split, effective March 24, 2026 (trading split-adjusted starting that date). Analysts had a prior consensus EPS estimate around $4.73 (some sources note $4.72–$4.76), which the company outperformed substantially.

Management established a medium-term goal to grow annual investment banking revenues to $2 billion plus. In 2025, the firm returned an aggregate of $239 million to shareholders through buybacks and dividends. Analyst sentiment remains positive post-release, with many maintaining “Buy” or “Strong Buy” ratings as of February 2026.

Geopolitical Risks and Sector Pressures

Piper Sandler faces specific challenges related to equity capital markets volatility. Recent sell-offs in technology and software sectors could pressure near-term equity underwriting activity. Additionally, Q1 seasonality typically makes early-year performance cadence uncertain.

The firm’s international operations in the U.K., EU, and Hong Kong expose it to varied regulatory and geopolitical environments. While specific tariff impacts on the service-based investment banking model are indirect, broader macro pressures such as interest rate volatility and shifting U.S. trade policies could impact the M&A and capital-raising activities of its corporate clients, particularly in the healthcare and industrial sectors.

Piper Sandler (PIPR) SWOT Analysis

Strengths

- Advisory Leadership: Record >$1 billion in annual advisory revenue, outpacing middle-market growth.

- Diversified Model: Strong performance across equity brokerage and municipal financing provides a hedge against M&A cycles.

- Shareholder Alignment: High capital return (including special dividends) and focus on returns.

Weaknesses

- Compensation Sensitivity: High compensation ratio (~61.4%) makes margins vulnerable to talent competition.

- Middle-Market Concentration: Heavy focus on middle-market clients can lead to higher volatility during economic contractions.

- Non-Comp Expense Growth: Increases due to office moves and business activity.

Opportunities

- M&A Resurgence: Expected recovery in bank M&A due to a more accommodating regulatory environment.

- Market Share Gains: MD headcount growth increasing capacity for larger, higher-fee transactions.

- $2B Revenue Target: Strategic pursuit of $2 billion+ in annual investment banking revenue.

Threats

- Macro Headwinds: Interest rate volatility and potential economic slowdown could impair deal-making.

- Geopolitical Instability: Risks in international markets (EU, Hong Kong) may disrupt global capital flows.

- Market Competition: Intense competition from “Bulge Bracket” banks and boutique firms for deal flow and talent.