Provident Financial Holdings, Inc. (NASDAQ: PROV), the parent company of Provident Savings Bank, F.S.B., has announced financial results for its second fiscal quarter ended December 31, 2025. The report detailed a period of significant year-over-year profit growth contrasted by a sequential decline in earnings, as the institution navigates a shifting interest rate environment and competitive regional banking landscape.

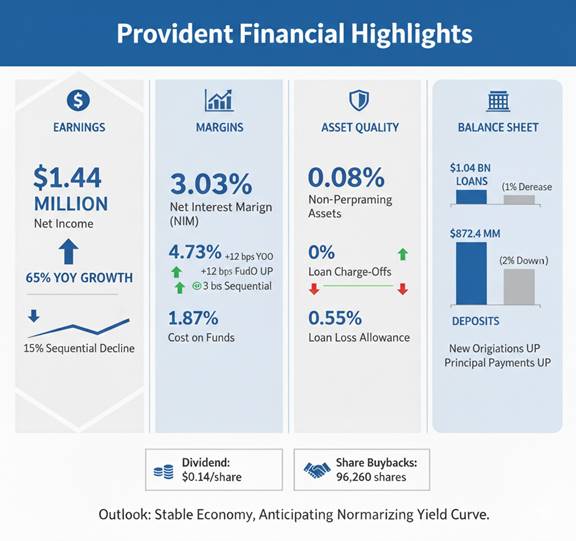

For the quarter, the company reported net income of $1.44 million, or $0.22 per diluted share. This performance represents a 65% increase from the $875,000, or $0.13 per diluted share, recorded in the same quarter of the previous fiscal year. However, when compared to the $1.69 million earned in the first quarter of fiscal 2026, net income fell by approximately 15%.

Shifting Credit Dynamics and Operating Expenses

The primary driver of the year-over-year earnings improvement was a substantial swing in credit loss accounting. During the second quarter, Provident recorded a $158,000 recovery of credit losses. This is a notable reversal from the $586,000 provision for credit losses—an expense—recorded in the second quarter of fiscal 2025.

The sequential dip in profitability was attributed to two primary factors. First, while the bank reported a recovery of credit losses, the amount was significantly lower than the $626,000 recovery recognized in the first quarter. Second, non-interest expenses rose to $7.78 million, an increase of $315,000 over the preceding quarter. A significant portion of this increase was tied to a non-recurring $214,000 expense for a pre-litigation mediation settlement involving an employment-related matter. These costs were partially offset by a lower income tax provision.

Interest Margin and Revenue Performance

A central feature of the report was the continued expansion of the bank’s net interest margin (NIM). The NIM reached 3.03% for the quarter, reflecting a 12-basis-point increase from the prior year and a 3-basis-point improvement from the previous quarter.

The expansion of the NIM was supported by a 7-basis-point rise in the average yield on interest-earning assets to 4.73%, while the average cost of funds fell by 5 basis points to 1.87%. Consequently, net interest income grew by 2% to $8.92 million, even as the average balance of interest-earning assets declined by 2%.

Management noted that the lower cost of funds was primarily achieved through a reduction in the average balance of higher-cost time deposits, which helped mitigate the competitive pressure on deposit pricing.

Balance Sheet Trends and Asset Quality

Provident’s balance sheet showed signs of modest contraction during the first half of the fiscal year. Total assets stood at $1.17 billion on December 31, 2025, a 2% decrease from June 30, 2025.

In the lending sector, loans held for investment totaled $1.04 billion. While loan originations for investment increased by 16% year-over-year to $42.1 million, this volume was surpassed by $46.7 million in loan principal payments—a 36% increase in repayment activity compared to the prior year. Total deposits also trended lower, falling 2% to $872.4 million since the end of the previous fiscal year.

Despite the reduction in asset volume, credit quality remained a metric of strength for the institution. Non-performing assets fell by 30% from the June 30, 2025 level to $990,000, representing 0.08% of total assets. The bank reported zero loan charge-offs during the quarter. Furthermore, the allowance for credit losses on loans decreased to 0.55% of gross loans. The company attributed this adjustment to a shorter estimated average life of the loan portfolio, a byproduct of declining mortgage rates which typically accelerate prepayment speeds.

Strategy and Forward Outlook

Provident Financial continues to execute a capital return strategy, repurchasing 96,260 shares of common stock during the quarter at an average price of $13.78 per share. The board also maintained its quarterly cash dividend of $0.14 per share.

Looking ahead, management described the current banking environment as highly competitive for both deposits and quality loan opportunities. However, leadership expressed optimism regarding the macroeconomic backdrop, specifically the potential for a “normalizing” yield curve.

A normalizing, or steepening, yield curve—where long-term interest rates are higher than short-term rates—is generally viewed as beneficial for traditional banking models. It allows institutions to price long-term loans more profitably while keeping short-term funding costs relatively lower. The bank indicated that its current strategy remains focused on maintaining strict underwriting standards and disciplined pricing to preserve margins in the coming fiscal periods.