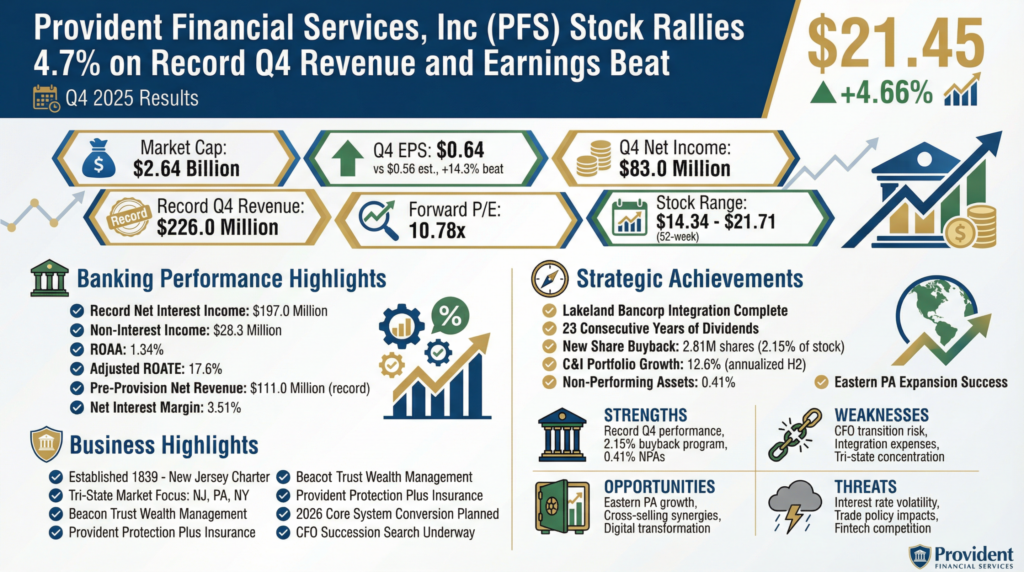

Strengths

- Record Financial Performance: Q4 revenue and pre-provision net revenue reached all-time highs.

- Capital Management: Initiation of a 2.15% share buyback program and 23 consecutive years of dividend payments.

- Asset Quality: Strong credit metrics with non-performing assets at just 0.41%.

Weaknesses

- Leadership Transition: Retirement of long-serving CFO introduces short-term execution risk during a core system conversion.

- Operating Expenses: Merger integration and technology investments continue to weigh on the total expense base.

- Geographic Concentration: Business is heavily concentrated in the tri-state area, making it sensitive to regional economic shifts.

Opportunities

- Commercial Growth: Specialized lending teams in Eastern Pennsylvania are driving high-teens annualized loan growth.

- Cross-Selling Synergies: Leveraging Beacon Trust and Provident Protection Plus for non-interest income growth.

- Digital Evolution: The 2026 core system conversion provides a platform for enhanced digital banking services.

Threats

- Macroeconomic Volatility: Shifting interest rate paths could compress net interest margins (NIM).

- Trade Policy: Tariffs on industrial clients could weaken the credit profiles of commercial borrowers.

- Competition: Intense rivalry from both national banks and digital-first fintech challengers for core deposits.