AlphaStreet Newsdesk powered by AlphaStreet Intelligence

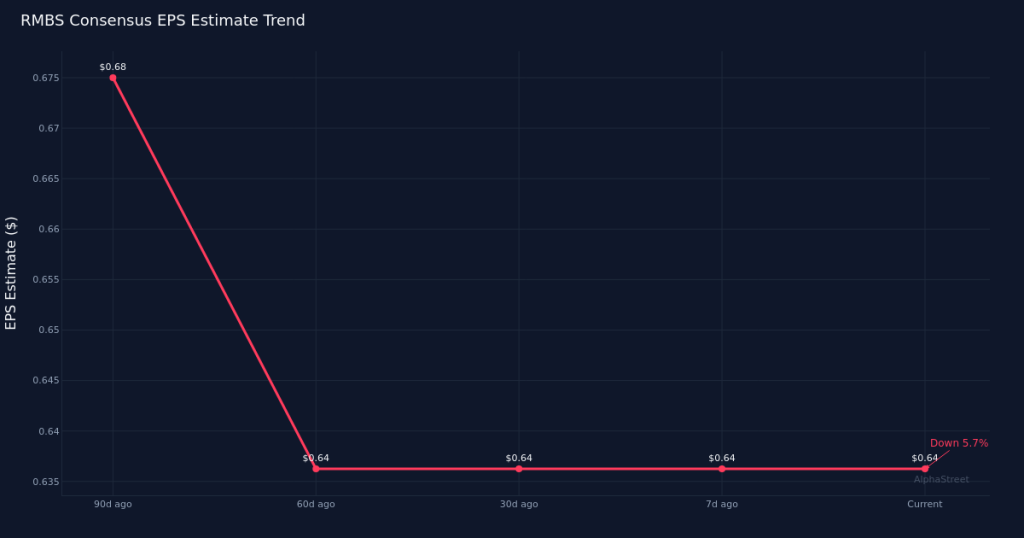

Wall Street is targeting earnings of $0.64 per share on revenue of $179.9M when Rambus Inc. reports first-quarter results on April 27. Eight analysts covering the semiconductor company have set estimates ranging from $0.60 to $0.68 per share on the bottom line, while revenue projections span $175.0M to $184.0M. The consensus marks another quarter of expected growth for the memory interface and security IP provider as it navigates the evolving semiconductor landscape.

Analysts have trimmed their outlook over the past three months, signaling some caution heading into the print. The EPS consensus has drifted down 5.9% on a 90-day basis, falling from $0.68 to the current $0.64 estimate. Over the past 30 days, however, estimates have stabilized at $0.64 with no further downward revision. This pattern suggests that while analysts recalibrated expectations earlier in the quarter, the outlook has found a floor more recently. The revision trajectory bears watching as it reflects shifting sentiment around Rambus’s near-term execution and end-market demand dynamics.

The consensus implies solid year-over-year expansion across both the top and bottom lines. Compared to Q1 2025 results, the revenue estimate of $179.9M represents growth of 7.9% from the year-ago figure of $166.7M. On the earnings side, the $0.64 consensus translates to an 8.5% increase from the $0.59 per share Rambus delivered in the prior-year period. Last year’s first quarter produced net income of $64.1M on revenue of $166.7M, yielding a net margin of 38.5%. The profitability profile from a year ago underscores Rambus’s ability to convert revenue into bottom-line results, and investors will be keen to assess whether margin performance has held up, expanded, or contracted as the business has scaled.

The company’s track record and recent momentum will shape investor expectations for how this quarter unfolds. While prior quarter results are not detailed in the available data, Rambus’s historical performance in Q1 2025 provides a benchmark for evaluating current operational trends. The semiconductor sector has experienced mixed demand signals across different end markets, from data center and AI applications to consumer electronics, and Rambus’s exposure to memory interface technologies positions it at the intersection of these dynamics. How the company has navigated inventory cycles, design win momentum, and royalty streams will be critical context for interpreting the upcoming results.

Rambus’s beat-or-miss pattern heading into this report will influence how the market interprets any variance from consensus. Companies with consistent track records of exceeding estimates often receive the benefit of the doubt when guidance appears conservative, while those with more volatile results face heightened scrutiny. The stability of estimates over the past month, following the earlier downward drift, suggests analysts have incorporated recent business trends into their models. Whether management’s commentary on design activity, customer engagements, and royalty visibility supports or challenges the current outlook will be a key element of the earnings call.

The stock’s positioning within its 52-week range adds another layer to the earnings setup, though specific price levels are not available in the verified data. Investor sentiment heading into a quarterly report often reflects accumulated expectations about both the quarter being reported and forward guidance. For a semiconductor IP company like Rambus, forward-looking commentary around licensing activity, product roadmaps, and customer adoption timelines can matter as much as the backward-looking quarterly results themselves.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.