AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street expects modest growth when Simpson Manufacturing Co., Inc. (NYSE:SSD) reports first-quarter 2026 results on April 27. The consensus among 3 analysts calls for earnings of $1.84 per share on revenue of $552.4M. The revenue estimate implies year-over-year growth of 2.5% from the $538.9M reported in the first quarter of 2025. Analyst EPS estimates range from $1.80 to $1.90, while revenue projections span $541.7M to $561.5M, reflecting modest dispersion in views on the engineered building products manufacturer’s performance.

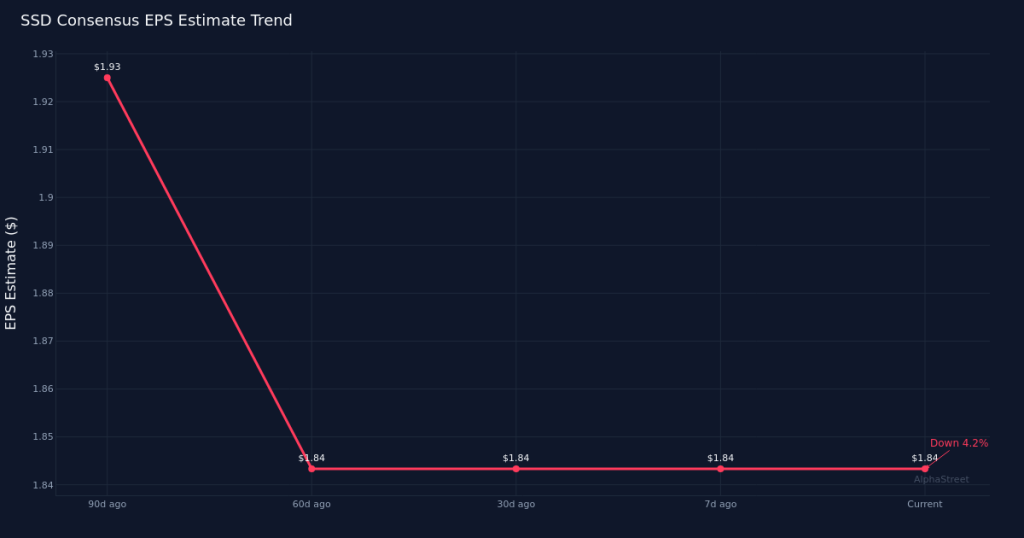

Analysts have tempered their profit outlook over the past three months. The current consensus of $1.84 per share is unchanged from 30 days ago but represents a decline of 4.7% from the $1.93 estimate that prevailed 90 days earlier. This downward revision suggests growing caution about Simpson’s ability to maintain profitability levels as the company navigates the first quarter, traditionally a softer period for construction activity. The compression in earnings expectations without corresponding revenue downgrades points to potential margin pressures or cost headwinds entering analyst models.

The year-over-year comparison reveals a company facing a fundamentally different profit dynamic than a year ago. In the first quarter of 2025, Simpson generated net income of $78.0M on revenue of $538.9M, translating to a net margin of 14.5%. With revenue expected to advance 2.5% to $552.4M, investors will scrutinize whether the company can preserve or expand that double-digit margin profile. The modest top-line growth reflects the ongoing normalization in residential construction activity and repair-and-remodel demand following the post-pandemic boom in housing activity.

Simpson’s first-quarter performance will set the tone for the full-year 2026 outlook. As a manufacturer of engineered structural connectors, fasteners, and related building products, the company’s fortunes track closely with housing starts, commercial construction activity, and do-it-yourself trends. The quarter typically sees seasonal softness in construction markets, particularly in regions affected by winter weather, making execution on cost control and operational efficiency especially critical. Investors will look for management commentary on order trends, channel inventory levels, and the pricing environment across both wood construction products and concrete construction products segments.

The company’s historical reporting pattern provides context for investors calibrating expectations. Simpson has established a track record in the engineered building products sector, though the limited analyst coverage of 3 estimates suggests the stock trades with less Wall Street attention than large-cap building materials peers. This creates potential for meaningful stock reactions to earnings surprises in either direction, as fewer analysts covering the name can lead to wider gaps between Street expectations and actual results.

Shares enter the report within the context of broader construction market dynamics. The stock’s positioning heading into the print will influence post-earnings volatility, as will any guidance adjustments for the remainder of fiscal 2026. With residential construction facing elevated mortgage rates and commercial development navigating uncertain demand conditions, Simpson’s ability to maintain pricing discipline while managing input costs will be paramount to margin preservation.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.