Shares of RBC Bearings Incorporated climbed in early trading on Thursday after the precision bearings maker reported third-quarter fiscal 2026 results that beat Street expectations. The stock was up modestly in the session, trading within its 52-week range of roughly $297.28 to $522.07, near multi-month highs amid a broader industrials sector rally.

RBC’s shares have outperformed over the past year, gaining sharply from their lows and recently testing 52-week highs, reflecting solid earnings momentum.

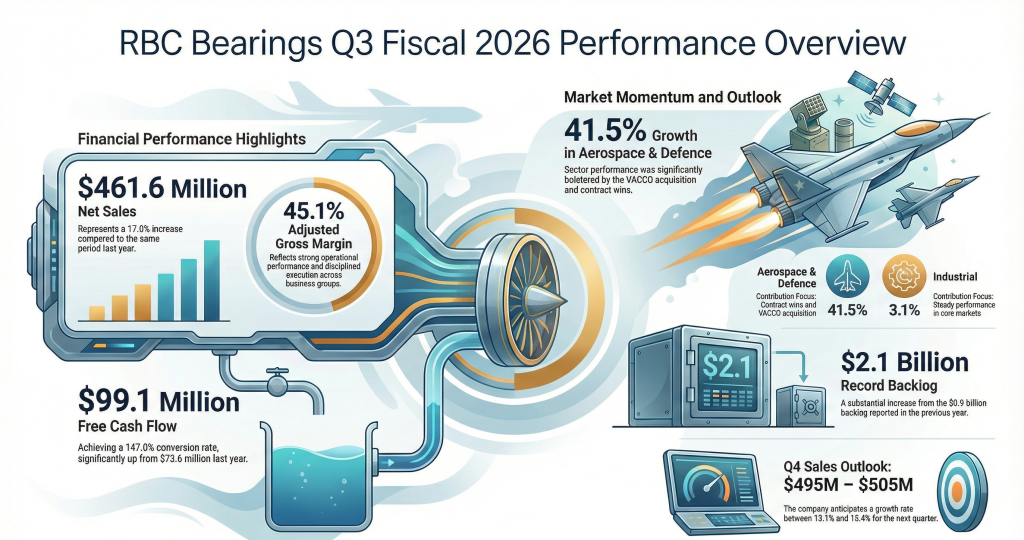

Third-quarter results beat expectations

RBC Bearings reported net sales of $461.6 million for the third quarter of fiscal 2026, an increase of 17.0% year-over-year. Aerospace/Defense unit sales rose about 41.5%, while Industrial segment sales grew roughly 3.1%.

Gross margin held at 44.3% of sales, in line with the year-ago period, while adjusted gross margin expanded to 45.1%. Net income attributable to common stockholders was 14.6% of net sales, up from 14.4% in the prior year, with adjusted EBITDA margin rising to 32.4% from 31.1%. Free cash flow increased substantially to $99.1 million from $73.6 million in the year-ago quarter.

On a per-share basis, diluted earnings per share came in at $2.13, with adjusted EPS of $3.04, reflecting year-over-year growth of about 17% and nearly 30% on an adjusted basis, respectively.

Nine-month results show consistent growth

For the first nine months of fiscal 2026, net sales rose nearly 12.9% to $1.35 billion versus prior year. Adjusted net income for the period was up more than 29%, with diluted EPS growth of about 22.5% compared with the same period in fiscal 2025.

The company also reported a growing backlog of $2.1 billion as of Dec. 27, 2025, compared with $0.9 billion a year earlier, citing strong defense and aerospace demand.

Outlook and guidance

RBC Bearings reiterated its fiscal fourth-quarter guidance, expecting net sales of approximately $495 million to $505 million, reflecting year-over-year growth of roughly 13.1% to 15.4%. Excluding contributions from its July 2025 VACCO acquisition, organic sales are expected to expand about 6.4% to 8.7%. Adjusted gross margin is projected to range between 45.0% and 45.25%, with SG&A as a percentage of sales targeted around 16.0% to 16.25%.

Sector context

Despite strong results, industrial and broader equity markets have faced macro-level pressures, including higher interest rates and moderating manufacturing activity. These factors have tempered gains in cyclical industrial and tech-linked stocks, particularly in lower-growth segments, while demand for defense-related components has remained resilient.