How is Repay different from other payment providers out there?

Tim: We are unique in the verticals we serve. We serve some very large underpenetrated verticals, like auto, finance, and business-to-business payments. Our payment technologies are proprietary and specific to serving the needs of the merchants in those verticals. And the integrations that we have are also pretty unique.

What were your observations and learnings from the pandemic year?

We saw a lot of shifts accelerate. We saw the shift happening — the move to digital payments — prior to Covid. But Covid really accelerated a lot of those trends, specifically in the business-to-business payment world, where AP clerks were no longer in the office and they weren’t able to write and send checks. They had to move to electronic.

We are serving businesses that have now accelerated all of that adoption of technology, for example, electronic payables. So I think those are trends that were starting to happen and were underway prior to Covid but they probably pushed them forward 18 to 24 months and I don’t see that going back.

I don’t see companies looking to become less efficient and less digital. Now I see everybody moving toward more digital. So we greatly benefited from that. At our own AP department, we’ve moved all to electronic payments and I don’t see us going back to manual. We were forced to do that because of Covid, but we are now really embracing it. There are thousands and thousands of businesses across the country doing the same thing.

What are the themes that you are witnessing specifically on the B2B space? And what are the areas that you feel are under-penetrated, where you see a possibility for further growth?

Yeah, so business-to-business payments have generally lagged consumer payments. The consumer payments market had adopted card payments much earlier. Consumers have been using cards to make payments in their daily lives for decades. B2B had just sort of really taken off in the last several years because of the technology and all the different pieces of businesses — payables or receivables departments are becoming digitized and using technology.

And so we’re in both sides of the transaction. We’re able to facilitate our business accepting a card payment from another business and we’re also able to help our customers send electronic payments to their vendors using virtual cards. So we can do both the acceptance, which is AR, and then the payables, which is AP.

And we see both of those very underpenetrated from our card perspective, and we think that’s a very large market. That’s why we’re spending a lot of resources there. It’s our fastest-growing vertical, and again, we’re on both sides, which is pretty unique.

We don’t think there’s a lot of companies that can do both the AR and AP. And we’re also integrated with the key accounting systems to be able to do both. And so that’s just the very large space that has taken a long time to get up the curve from a digital payments perspective, but I think it’s finally there.

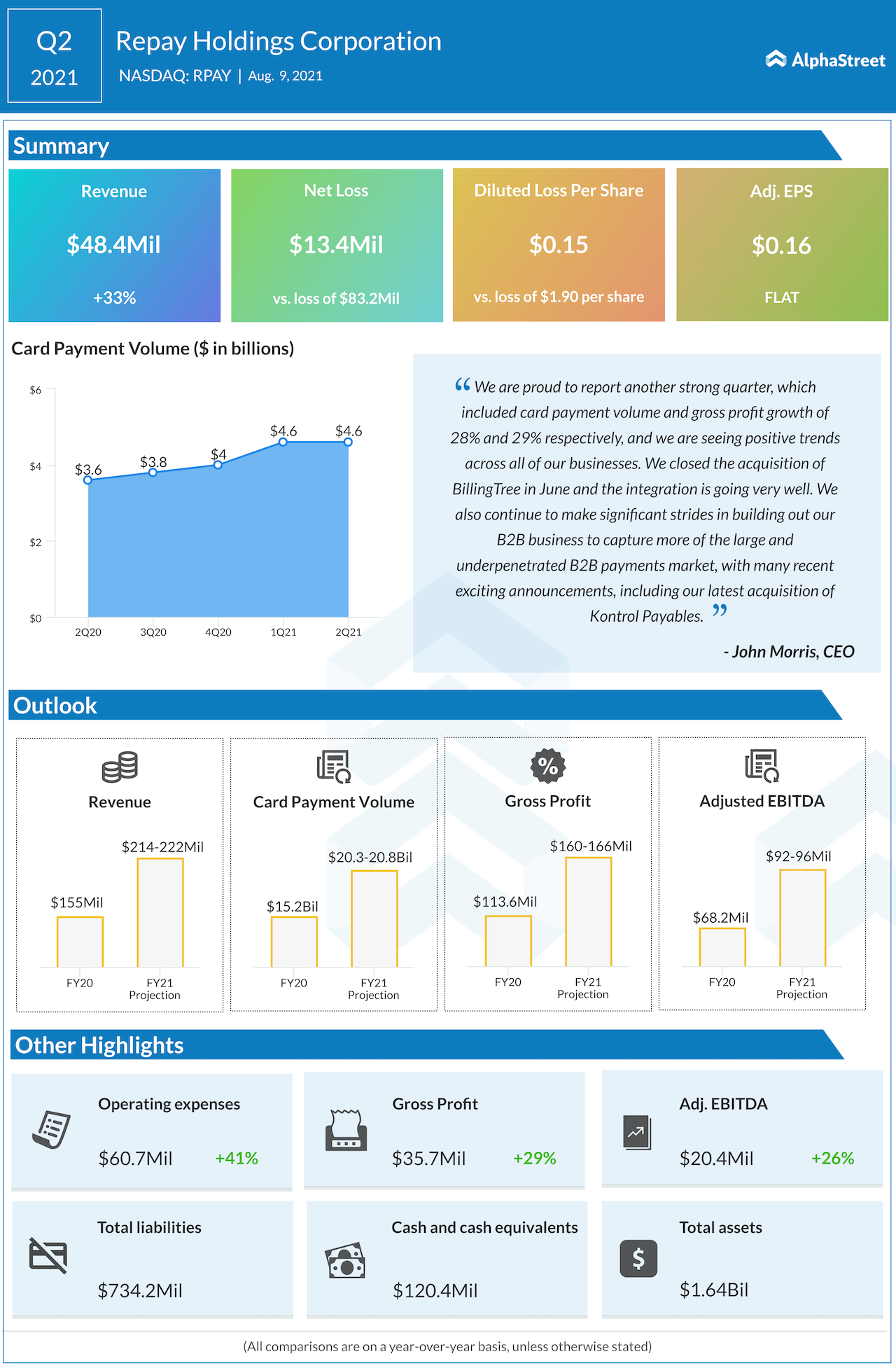

You had raised your full-year guidance while reporting earnings last month. Do you see those tailwinds continuing to act on your financials going into this quarter?

Yes, we feel good about the trends we see. What we feel really good about is what we see for next year. We’re still kind of in this Delta variant phase, which hopefully will normalize in 2022. So we feel good about what we’re seeing in Q3 and Q4, but really even more excited about what we see for the full year of 2022.

Healthcare is an area where we’re both in the acceptance part and the payables part. And as you know, hospitals have been, unfortunately, logged down again with Delta variant and we hope that there’s some pent-up demand within hospitals, that will benefit us going into next year as well.

ALSO READ AdTheorent CEO Jim Lawson: We are a privacy-forward digital ad platform

You are very active on the M&A side, and obviously, that requires a lot of funding. What’s your funding strategy?

Earlier this year in January, we completed a concurrent common stock and convertible debt offering. And so we have $440 million of debt today and about $120 million of cash. So about $320 million of net debt puts us at about 2.8 times net leverage. It’s a very comfortable level for us, we have a $125 million undrawn revolver. So we have the capacity to do additional M&A just with our existing balance sheet.

We think we could comfortably stretch up to maybe four times net leverage, maybe a little bit of above four times in that leverage, knowing that our target would be to bring that back down to around three to three and a half times within 12 to 18 months. And we have the capacity to do that.

I think for the near term we are more focused on using our balance sheet and the debt and cash we have. If there is a much larger deal in the future, we have to consider equity again.

ALSO READ Kontrol Technologies CEO Paul Ghezzi: Our focus is on reinvesting for growth

What is going to be the management’s focus for the next 12-24 months?

Yes. So like I mentioned earlier, the fastest-growing part of our business is B2B. So we’re focused on investing there. We’re focused on continuing to increase organic growth. We want to see organic growth in the high teens, the 20%, and for that I think we could tack on some M&A to facilitate even faster growth.

That’s something we’ve been successful at during the past years when we’ve made several acquisitions. All of these are intended to be very strategic and intentional and put us in verticals where there’s a very large addressable market.

____

For more insights into Repay Holdings, read the latest earnings call transcript