Since the start of the pandemic, work collaboration tools have gained more popularity. While more collaborative communication companies are coming up now, the existing companies are trying to capture the major share of the pie. In this scenario, the San Francisco-based workplace collaboration platform Slack Technologies (NYSE: WORK) reported its first quarter of 2021 results yesterday.

Q1 results

Even though Slack surpassed top and bottom line estimates for Q1, its shares cratered 14% today as investors and market watchers compared Slack’s quarterly results with video chat provider Zoom’s (NASDAQ: ZM) stellar Q1 results.

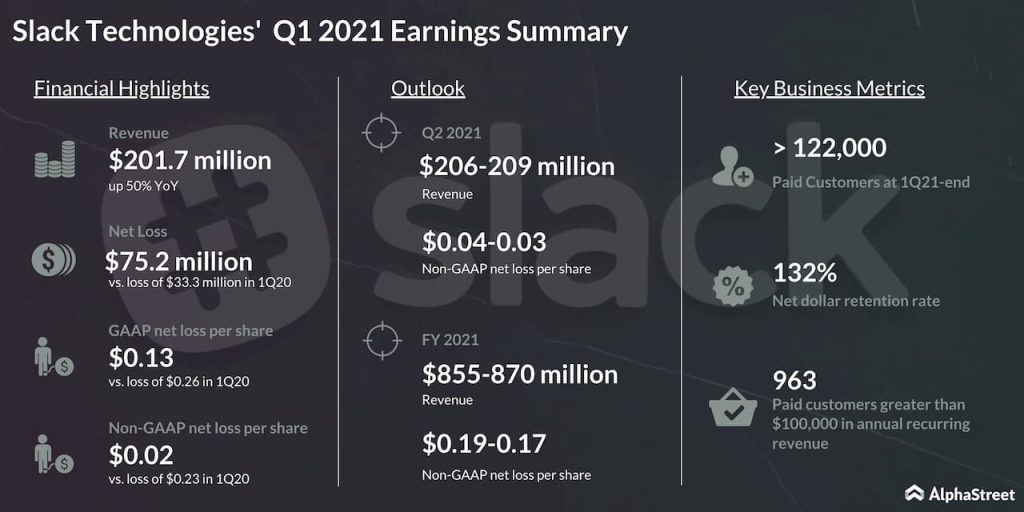

In the first quarter of 2021, which was described by CEO Stewart Butterfield as intense, productive, overwhelming and exciting, Slack’s revenue rose 50% year-over-year. Calculated billings (revenue plus the change in deferred revenue in a given period) grew 38% and the growth was impacted by $17 million of headwinds. The $10 million of billings occurred in the first quarter of 2020 and $7 million was COVID-19 related billings headwinds.

Expected impact from COVID-19

In Q1, there were a number of COVID-19-related headwinds for Slack. To support distressed customers, the company offered credits, installment billings and billings duration of less than one year. Slack also built-up reserve to account for potential credit issues, which is a negative impact of deferred revenue. These COVID-19-related billings headwinds totaled $7 million in the first quarter. The company expects calculated billings to be less useful as a measure of underlying growth during the COVID-19 crisis.

Slack expects net new customer additions to moderate through the remainder of the year to quarterly levels closer to those observed in fiscal 2020.

[irp posts=”63480″]

The company estimates about a quarter of its business is

derived from companies with less than 100 employees. Within this small medium

business base, churn trend was a bit higher than historical norms in March and

April, albeit off a low base.

Despite having a diversified customer base, Slack said that some of its customers have been impacted by COVID-19. The company estimates that less than 20% of its business is derived from the most directly impacted industries such as travel, hospitality, commercial real estate, ridesharing and retail.

In the enterprise segment, some sales cycles have

accelerated due to work from home, but others have slowed, particularly in impacted

industries. There is less visibility into how IT spending will trend for the

remainder of the year, particularly if the economic effects of the COVID-19

pandemic persist or worsen.

Guidance

Due to the uncertain environment, Slack withdrew its calculated billings outlook. For the second quarter, Slack expects revenue to be between $206 million and $209 million, representing growth of 43% at the midpoint. Non-GAAP loss per share is expected in the range of $0.04 to $0.03.

For the full year 2021, Slack lifted its revenue guidance to

a range of $855 million to $870 million, representing growth of 37% at the

midpoint. Non-GAAP loss per share is expected to be in the range of $0.19 to $0.17.

Slack vs. Zoom

Slack is not specifically a tool for remote work. It’s a channel-based messaging platform to improve communication with the employees. During the prepared remarks, CEO Stewart said,

“Unlike the many video conferencing solutions in the market such as Zoom, RingCentral, Google Meet, Microsoft Teams, Amazon Chime, and BlueJeans, we aren’t a digital substitute for physical, in-person meetings. Instead, Slack acts more like a digital office, a persistent place for users to connect and find information”.

Zoom’s revenue grew 169% and it doubled the revenue outlook for fiscal 2021, which propelled ZM shares to reach an all-time high on Wednesday. Slack investors and market watchers weren’t impressed comparing Zoom’s revenue growth and its upbeat FY21 outlook. Maybe, if Slack had reported its quarterly results before Zoom, WORK stock wouldn’t have experienced this steep fall.

[irp posts=”63295″]

But it’s worth noting that Zoom ended Q1 at 769 paid users

with 769 customers with more than $100,000 in trailing

12 months revenue, while Slack finished Q1 with 963 customers spending

more than $100,000 annually.

When questioned on the competitive landscape, CEO Stewart answered,

“I think it’s really what you saw with Zoom, what you saw with Teams is a great indication that this is not apples-to-apples and that the products are not really competitive with one another. You just can’t adopt Slack that quickly. You can’t move from email to channel-based messaging in that short amount of time, which is — I wish that call cultures could change overnight. But I think what you really saw from Microsoft and from Teams was the emphasis on voice, the emphasis on video calling product, moving people over from Skype for business.”

Read the entire Slack Technologies (WORK) Q1 2021 transcript