Video conferencing platforms and other workplace collaboration tools have become more popular nowadays. With most people confined to their homes, apps that allow us to stay in touch have become essential to our day-to-day lives as a result of the COVID-19 pandemic. In this article, let’s analyze video chat app provider Zoom Video Communications’ (NASDAQ: ZM) first quarter 2021 performance and its future.

Q1 results

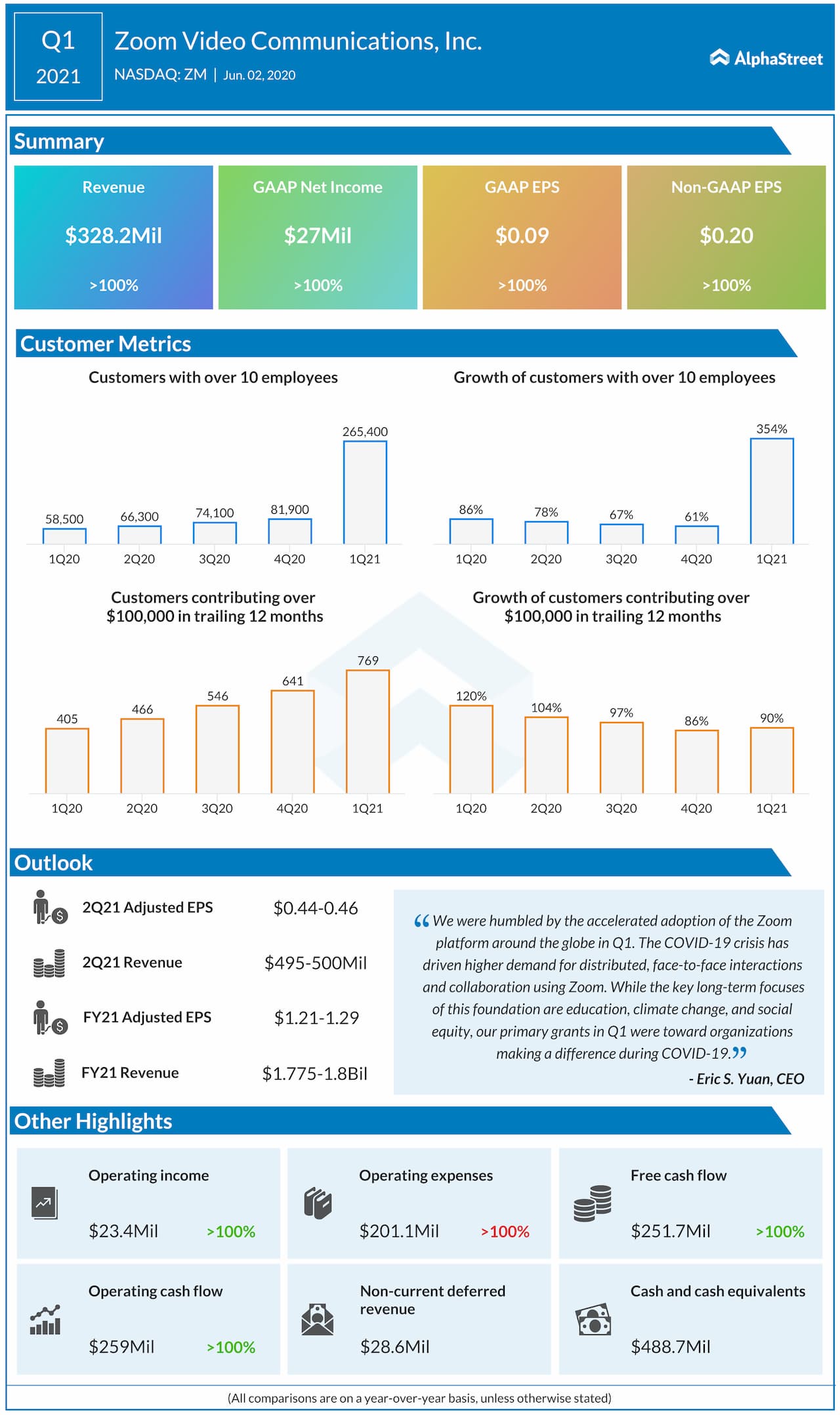

While Zoom’s first quarter

of 2021 results surpassed the market’s view, the company’s outlook for Q2 was

better-than-expected. The company also doubled

its previously announced outlook for fiscal 2021. Revenue jumped 169% due

to subscriptions provided to new customers, which accounted for 71% of the

increase. Subscriptions provided to existing customers accounted for 29% of the

revenue increase. Demand was broad-based across industry verticals, geographies

and customer cohorts.

Both domestic and international markets had strong growth during the quarter. Americas grew at a rate of 150% year-over-year. Combined APAC and EMEA revenue grew even higher at 246% and represented approximately 25% of revenue.

[irp posts=”62102″]

Customer metrics

Zoom ended Q1 at 769 customers with greater than $100,000 in trailing 12 months revenue, up 90% annually. The increase of 128 customers over Q4, a record number of adds in a quarter. The addition of over 183,000 customers with more than 10 employees in the quarter, brought the total to 265,000.

The customer segment with 10 or fewer employees also expanded during the quarter as individuals adopted Zoom for many personal and social uses. As a result, customers with 10 or fewer employees represented 30% of revenue in Q1, up significantly from 20% in Q4.

As already stated by the

company in April, daily participants (free and paid meeting participants, not

unique) peaked to 300 million in April and Zoom stated that this number came

down a little bit in May on average.

Security issues

The adoption and traffic on the Zoom rapidly increased after the work-from-home and social distancing initiatives. As part of their business continuity plans, more enterprises started using the Zoom platform. When physical gathering was not possible, the first-time consumers used Zoom for personal and social purpose to connect with their friends and families.

Zoom stated that it opened

the platform to unprecedented numbers of first-time users during the crisis.

Zoom didn’t fully consider the challenges of letting those users who did not

have full IT support or established protocols for security and privacy like enterprise

customers.

During the first quarter earnings call, CEO Eric Yuan said,

“We have experienced negative press related to meeting disruption, security and privacy issues. Since these issues emerged, we have transparently and quickly addressed specific security and privacy issues, including, enacted a 90-day plan initiative on security and privacy with a weekly webinar for customers to ask me anything.”

He also added that Zoom acquired Keybase team to add engineering expertise to build an end-to-end encrypted meeting mode. The company also released Zoom 5.0 plan with new security features and enhancements.

[irp posts=”52189″]

When answering a question on the deployment of end-to-end encryption, Eric stated that this feature will be available with limited functionality for free users. For enterprise customers, those security features are built in and the challenge is how easily letting consumers enable that, he said.

Intensifying competition

Zoom faces competition from Cisco Webex, LogMeIn’s GoToMeeting, Microsoft Teams, Google G Suite, and PBX providers including Avaya and RingCentral, There are also large players like Facebook and Amazon who are trying to enter in the video communications arena.

Also, it’s worth noting that

Verizon has recently acquired video conferencing platform BlueJeans and

RingCentral’s enhanced offering with video capabilities.

Speaking on the competitive landscape, CEO Eric said that the pandemic crisis will not change anything, and the company is still laser focused on the video and also to have phone service,

When asked whether market

consolidation will limit to the competitors for enterprise communications, CEO

Eric said,

“It’s too early to tell. But overall, I truly believe the best-of-breed service provider will survive and thrive because customer — when it comes to video and voice, you’ve got to make it work anytime, everywhere, any device. It’s not that easy.”

Future ahead

As governments start to ease shelter-in-place restrictions, Zoom expects moderated demand for its services. Based on the assumptions on higher churn rate as well as economic uncertainty, Q3 and Q4 revenue is projected to be relatively consistent with Q2.

There are large opportunities ahead for Zoom. However, the company wants to focus mainly on keeping its service up, keep it down on the privacy, security issues and also down the road it wants to double down on the new growth areas.

When asked what would be

Zoom’s focus in the next 12 months, CEO Eric said.

“Even before this pandemic crisis, we — not only did we offer the video conferencing service, but also we have Zoom Phone system, and don’t forget about that. It’s also a huge opportunity. In particular, we believe, video and voice, those two are going to be converged into one service.”

Zoom Phone creates a huge

opportunity for more sales in Q2 and the rest of this year, he added.

Even in the areas where they’re starting to ease shelter-in-place, people are taking their time to go back to work and this is expected to help Zoom in the rest of FY21.

Stock performance

Yesterday, Zoom stock surged to all-time high ($224.46) and it had gained more than 200% since the beginning of this year. Given its recently ended quarter’s stellar results and the spectacular outlook for FY21, one can consider buying ZM stock when it falls below the $200 mark.

Read the entire Zoom Video Communications (ZM) Q1 2021 earnings transcript