Smartsheet’s (NYSE: SMAR) stock was down 2% in the after-market trading hours as the second quarter earnings outlook failed to impress the street. However, full-year guidance came in line with the estimates. The company’s share price has increased about 61% this year and touching a new 52-week high level of $49.04 in March after the Q4 earnings beat and has surged 166% since IPO last April.

Q2 Outlook

Revenue is expected between $63-64 million, higher than $61.09 million expected by the street. However, adjusted loss per share is projected in the range of $0.16-0.15, which is higher than the 13 cent loss anticipated by the analysts.

Full-Year Outlook

For the full year, the company is expecting sales of $262-265 million and a non-GAAP loss of $0.59-0.54 per share. The revised headline numbers are better than the prior outlook provided by the firm last quarter. Analysts are forecasting a loss of $0.57 per share on revenue of $255.46 million, which is at the midpoint of the guidance provided by Smartsheet.

Q1 Performance

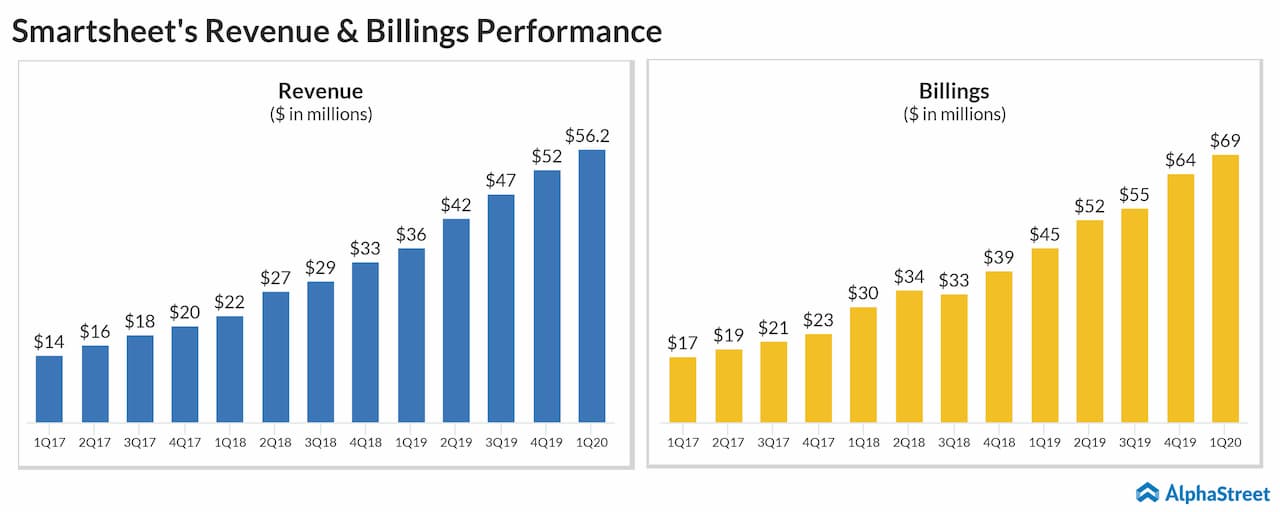

The workflow management platform continued its momentum from the last quarter with both the top and bottom line numbers surpassing estimates. Revenue soared 55% to $56.2 million while adjusted loss per share was flat at $0.12. Analysts were anticipating sales of $54.5 million and loss per share of 18 cents.

Smartsheet continues to see strong demand for its cloud-based collaboration platform from new and existing clients. Subscription revenues jumped 57% while professional services grew 38% over the prior year. Net loss widened 38.4% to $19.8 million due to an increase in expenses.

As expected, operating expenses jumped nearly 60% over the prior year period as the cloud-based platform continues to invest in augmenting the service offerings, expanding the presence, and increase the sales team to grow its client base and top line. However, this is going to impact earnings in the near future.

Key Business Metrics

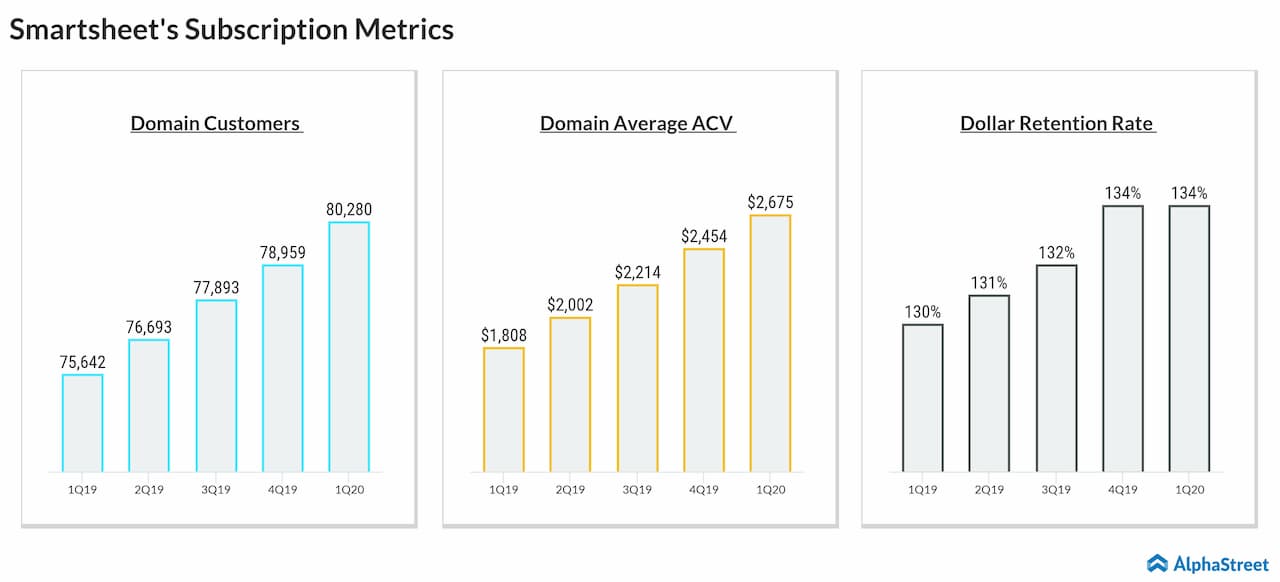

On the key metrics front, the company added 4.638 new clients in the first quarter over last year. Annualized contract values (ACV) surged 48% per domain-based client which is a good sign for investors as the investments made by the firm is paying off. Most importantly, ACV for $50,000 or more and $100,000 or more clients skyrocketed 117% and 139% over the prior year period.

Dollar retention rate helps investors to know whether Smartsheet is able to retain and sell more services to existing clients who are with the firm for more than a year. For the first quarter, retention rate came in at 134%, an increase of 4% from last year.