AlphaStreet Newsdesk powered by AlphaStreet Intelligence

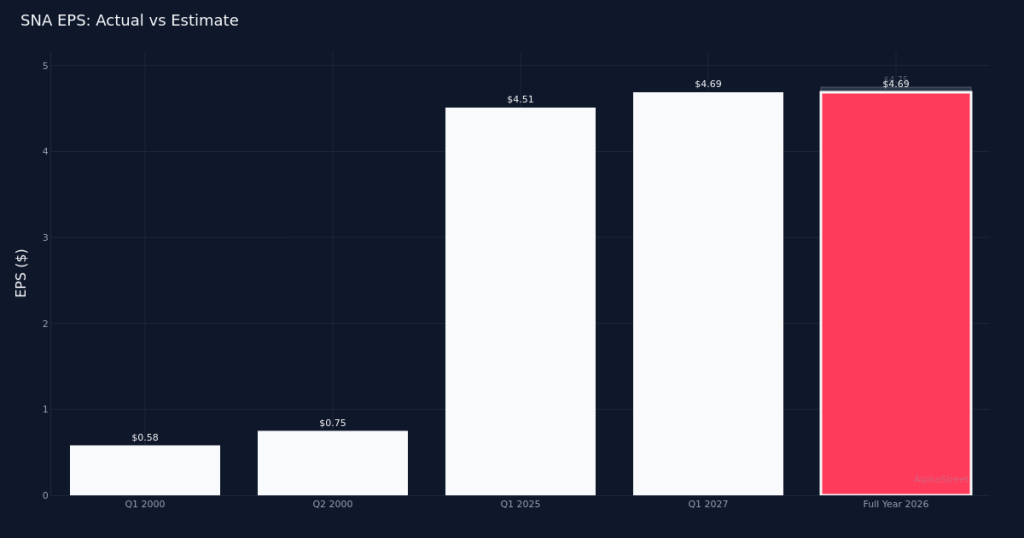

Mixed signals define Snap-on’s Q1 2026 result. The industrial tools manufacturer missed consensus EPS estimates by 1.3% with $4.69 per share against expectations of $4.75, even as revenue beat by 2.5% at $1.21B versus the $1.18B estimate. The disconnect between top-line strength and bottom-line disappointment points to margin pressure that warrants closer examination, particularly given the company’s premium market positioning. Net income of $247.0M translates to a 20.4% net margin, down from 21.1% in the year-ago period—a 0.7 percentage point compression that explains why revenue growth of 5.8% yielded only 4.0% EPS growth.

Earnings quality deteriorated despite revenue gains. The margin compression story becomes clearer when dissecting the P&L structure. While gross margin held relatively firm at 50.3% on gross profit of $608.3M, the operating margin of 26.3% on operating income of $318.8M reflects the company’s ongoing investment cycle. Management acknowledged the consolidated margin pressure, noting that “the consolidated margin, including both OpCo and financial services, of 24.4%, that compared to 25.3% last year.” The 90 basis point decline in consolidated margin suggests that incremental revenue is being earned at lower profitability than the existing base—a concerning dynamic for a company trading at premium multiples. The financial services segment experienced particular weakness, with management noting earnings “were lower by $2.3 million, or 3.3%” to $68M, creating a drag on overall profitability despite operational improvements elsewhere.

Revenue trajectory shows deceleration from exceptional comparisons. The 5.8% reported revenue growth and 3.4% organic growth represent solid absolute performance but must be contextualized against the four-quarter trend. Q4 2025 revenue of $1.23B exceeded the current quarter’s $1.21B, indicating sequential softness despite typical seasonal patterns. Management celebrated the result as “a new first quarter record, and our second highest quarterly sales ever,” but this framing obscures the sequential decline. The organic growth rate of 3.4% provides the cleaner read-through, stripping out acquisition and currency effects, and management acknowledged that operating income growth was “in the same zip code as the growth of the 3.4%,” suggesting limited operating leverage.

Segment dynamics reveal uneven growth drivers. The Commercial & Industrial Group emerged as the standout performer with $381.0M in revenue and 10.8% growth, nearly double the corporate average and indicating strong end-market demand in manufacturing and heavy industry applications. The Snap-on Tools Group generated $486.0M with 5.0% growth, slightly below the consolidated rate, suggesting that the core franchise network—while stable—isn’t driving outperformance. The Repair Systems & Information Group posted $485.3M in revenue but lacked disclosed growth metrics, making it difficult to assess whether this critical diagnostic and software business is maintaining momentum. The dispersion in segment performance creates portfolio risk; the company’s growth is increasingly dependent on the cyclically sensitive Commercial & Industrial business rather than the historically more stable Tools Group franchise model.

Cash generation remains a bright spot. Operating cash flow of $368.7M in the quarter demonstrates the business model’s inherent cash conversion strength, though without year-ago comparables it’s impossible to assess trend direction. The absolute dollar figure is substantial relative to the $247.0M in net income, implying healthy working capital dynamics and limited cash-based restructuring charges. Management’s comment that cash flow is “well over $100 million in a quarter” understates the actual performance, suggesting conservative financial communication—or perhaps indicating that some quarters fall below that threshold. For a capital-light business model with minimal maintenance capex requirements, the strong cash generation provides flexibility for shareholder returns and strategic investments, even as reported earnings disappoint.

Market reaction implies relief rather than celebration. The stock’s 2.2% gain to $390.75 following an earnings miss indicates investors entered the print with lowered expectations or found comfort in the revenue beat and segment mix. The positive reaction despite the EPS miss suggests the market is focused on top-line sustainability rather than near-term margin optimization. However, the modest magnitude of the gain—coupled with the earnings quality issues—suggests limited conviction that the current growth trajectory is sustainable at premium valuation levels. With a 0% beat rate over the last quarter, the company has established no recent track record of conservative guidance or consistent positive surprises that might support multiple expansion.

Guidance absence leaves investors without a roadmap. The lack of updated forward guidance in the verified data leaves a critical gap in assessing management confidence and the sustainability of current trends. Investors must extrapolate from the 3.4% organic growth rate and current margin structure, which implies modest mid-single-digit earnings growth if margins stabilize—hardly a compelling setup for a premium-valued industrial. The margin compression dynamic becomes the key variable: if the 0.7 percentage point net margin decline represents investment for future growth, the current valuation might be justified; if it reflects structural cost inflation or competitive pricing pressure, further multiple compression looms.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.