AlphaStreet Newsdesk powered by AlphaStreet Intelligence

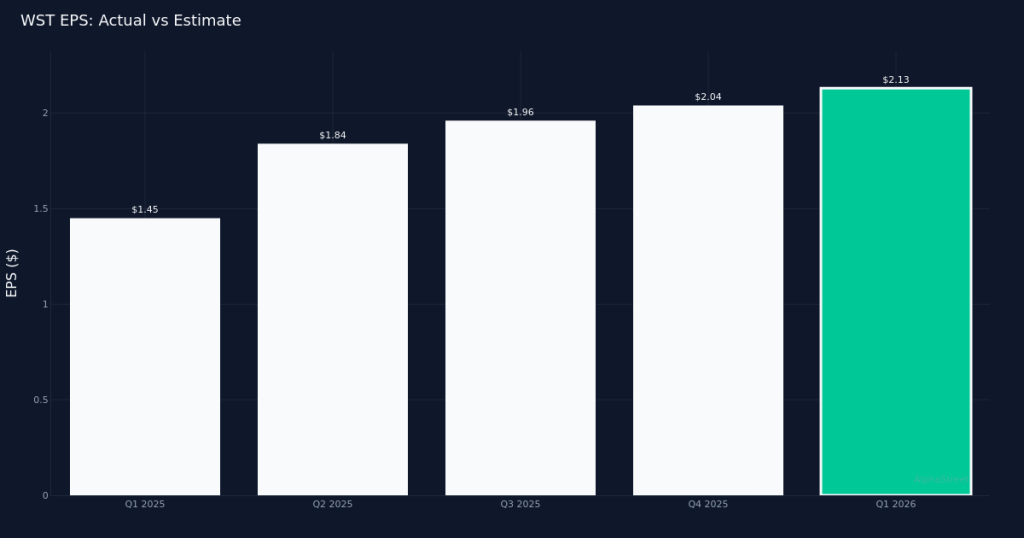

West Pharmaceutical Services delivered a commanding first-quarter performance that exceeded expectations by a substantial margin and forced a reset of full-year guidance higher. The company’s adjusted EPS of $2.13 beat the consensus estimate of $1.69 by 26.0%, while revenue of $844.9M represented 21.0% growth year-over-year. The magnitude of the beat—combined with organic revenue growth of 15.3%—signals underlying demand strength rather than acquisition-driven inflation, a critical distinction for assessing earnings quality. Management responded by raising full-year organic revenue growth expectations to 7% to 9% from a prior 5% to 7% range, stating “We now anticipate full-year organic revenue growth back to our long-term construct of 7% to 9%, up from our previous guide of 5% to 7%, and adjusted EPS increase to the range of $8.40 to $8.75.”

Earnings quality appears robust, driven by revenue expansion rather than margin engineering through cost reduction. Net margin expanded to 16.4% from 15.2% in the year-ago quarter, a 1.2 percentage point improvement that accompanied top-line growth of 21.0%. This simultaneous expansion of both revenue and profitability indicates operating leverage is working in the company’s favor. Operating margin reached 21.0%, while gross margin stood at 35.1%, reflecting pricing power and manufacturing efficiency gains. The $138.8M in net income represents a 46.9% increase from the prior year’s $106.2M, substantially outpacing revenue growth and demonstrating the scalability of the business model. This is the hallmark of quality earnings—not just hitting numbers through aggressive cost management, but delivering profit growth that exceeds revenue growth through operational execution.

The revenue trajectory shows clear acceleration across consecutive quarters, with Q1 2026 marking the fourth straight quarter of sequential growth. Revenue progressed from $766.5M in Q2 2025 to $804.6M in Q3, $805.0M in Q4, and now $844.9M in Q1 2026. Management noted “First-quarter revenues of $845 million were up 21% on a reported basis and 15% on an organic basis,” highlighting that even stripping out inorganic contributions, the growth trajectory remains firmly intact. The 21.0% reported growth rate represents a meaningful reacceleration from what had been more modest quarterly increases through 2025. This pattern suggests demand inflection rather than a temporary spike, particularly given the organic growth component exceeded 15.0%.

Segment performance reveals HVP Components as the standout growth driver, though all divisions contributed positively. HVP Components generated $409.3M in revenue with 29.6% growth, the strongest performance among disclosed segments. Management highlighted specific strength within this division, noting “This business continues to be a strong growth driver for our HVP Components business and delivered 26% organic growth.” The Proprietary Products segment delivered $694.3M with 23.3% growth, representing the largest absolute revenue contributor. West Vantage, at $150.6M with 11.6% growth, lagged the other segments but still posted double-digit expansion. The dispersion in growth rates suggests HVP Components is capturing share or benefiting from end-market tailwinds that aren’t equally distributed across the portfolio, warranting closer examination of the sustainability of that 29.6% growth trajectory.

The updated full-year guidance implies material upside to prior expectations and suggests management confidence extends beyond a single strong quarter. The adjusted EPS guidance range of $8.40 to $8.75 yields a midpoint of $8.57, which management elevated from prior targets alongside the organic revenue growth increase. Revenue guidance of $3.29B to $3.35B provides a relatively narrow band, suggesting visibility has improved rather than deteriorated. At the midpoint, the guidance implies Q2-Q4 average quarterly EPS of approximately $2.15, essentially flat to the Q1 performance, indicating management views this quarter as a sustainable baseline rather than a peak. The raised organic growth target to the company’s “long-term construct” suggests cyclical headwinds that may have suppressed growth are dissipating.

Cash generation metrics reveal a divergence between operating performance and free cash flow conversion that merits monitoring. Operating cash flow of $89.9M converted to free cash flow of just $47.2M, indicating capital expenditures consumed roughly 47% of operating cash flow in the quarter. While a single quarter doesn’t establish a trend, this conversion rate appears relatively low given the strong profitability metrics elsewhere in the report. Management commentary emphasized project activity, noting “We’ve seen a sequential improvement over the prior quarter, and it’s up 66% over the first quarter of last year of number of projects that we have taken on,” which may explain elevated capital deployment. The question is whether this capex intensity supports future margin expansion or represents ongoing investment requirements that will persist.

The stock’s 12.9% surge to $309.70 reflects investor enthusiasm for both the beat and the guidance raise, though the reaction appears measured given the magnitude of the earnings surprise. A 26.0% EPS beat paired with raised full-year guidance would typically justify a more aggressive revaluation, suggesting either skepticism about sustainability or prior positioning that limited short-covering potential. The move does reward shareholders who maintained conviction through what appears to have been a period of lowered expectations, given the prior 5% to 7% organic growth guide that has now been reset higher. Track record matters for credibility, and management delivered a beat in 1 of the last 1 reported quarters, representing a 100% beat rate over the limited disclosed period.

Geographic performance questions raised by analysts suggest international markets may be driving outsized results. One analyst inquiry referenced the strong 29.6% growth, asking “Pretty strong 29% growth in Q1, so just wondering if that’s being underpinned by anything notably different than your U.S.” This line of questioning implies potential geographic concentration of growth that could create sustainability questions if driven by region-specific factors rather than broad-based demand. The answer to this question—not disclosed in available data—will determine whether the current growth trajectory can persist across economic cycles and regional variations.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.