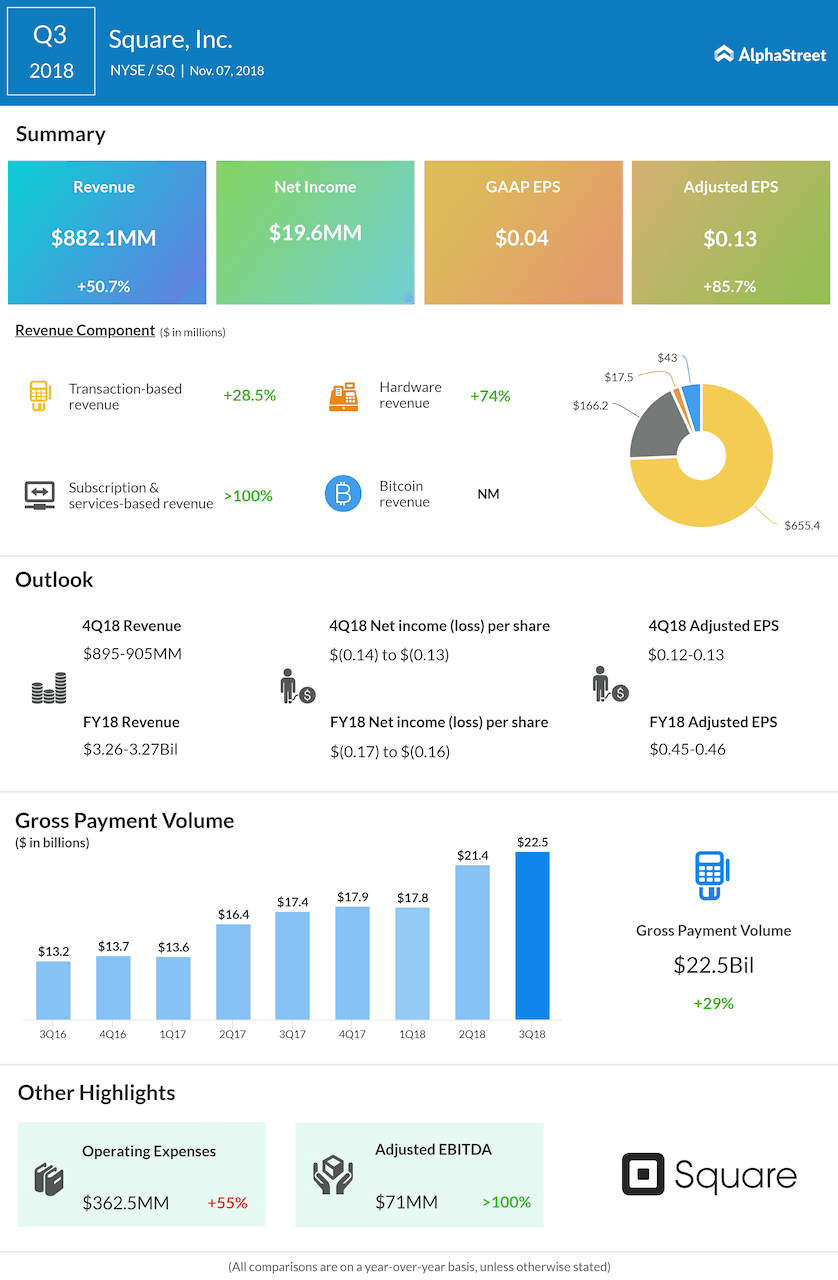

Square (SQ) stock inched down over 4% in the after-market session following weak guidance for the fourth quarter. The third quarter bottom line results benefited from the strong revenue growth as well as the gain from the initial public offering of Eventbrite. The results came in ahead of analysts’ expectations.

Net income was $19.6 million or $0.04 per share compared to a loss of $16.1 million or $0.04 per share in the previous year quarter. The latest quarter results included gain as a result of the IPO and subsequent mark-to-market valuation of its Eventbrite investment. Non-GAAP EPS soared 86% to $0.13.

Revenue surged 51% to $882 million and adjusted revenue soared 68% to $431 million. Gross Payment Volume (GPV), which is a key metric tracked by the investors, rose 29% to $22.5 billion on the continued contribution from large sellers.

The payment processor expects its fourth-quarter adjusted earnings to be in the range of $0.12 to $0.13 per share trailing analyst consensus of $0.15 per share. Adjusted EBITDA is forecasted to be between $75 million to $80 million. Adjusted revenues outlook came in better than street estimates in the range of $446 million and $451 million.

For 2018, Square has lifted the adjusted revenue guidance to the range of $1.569 billion to $1.574 billion from the prior range of $1.52 billion to $1.54 billion. Adjusted EPS outlook was lifted to the range of $0.45 to $0.46 from the previous range of $0.42 to $0.46. Adjusted EBITDA estimates were raised to the range of $250 million to $255 million from the prior forecast of $240 million to $250 million.

Square’s loss narrowed, weak Q3 profit outlook remains a concern

For the third quarter, transaction-based revenue climbed 29% year-over-year helped by the improvements in its transaction cost profile. Subscription and services-based revenue soared 155% driven primarily by Instant Deposit, Cash Card, Caviar, and Square Capital. Hardware revenue jumped 74% with continued growth from Square Register, Square Reader for contactless and chip, Square Stand, and third-party peripherals.

Square garnered $43 million from Bitcoin trading, which is an increase of about 26% compared to $34 million raked in the first quarter of 2018. In January, bitcoin trading was launched in its Cash app, available throughout the US excluding few states. The company expects to garner more revenues from bitcoin trading in the future.

Shares of Square ended Wednesday’s regular session up 6.96% at $82.69 on the NYSE. The stock has risen over 138% in the year so far and over 124% in the past year.