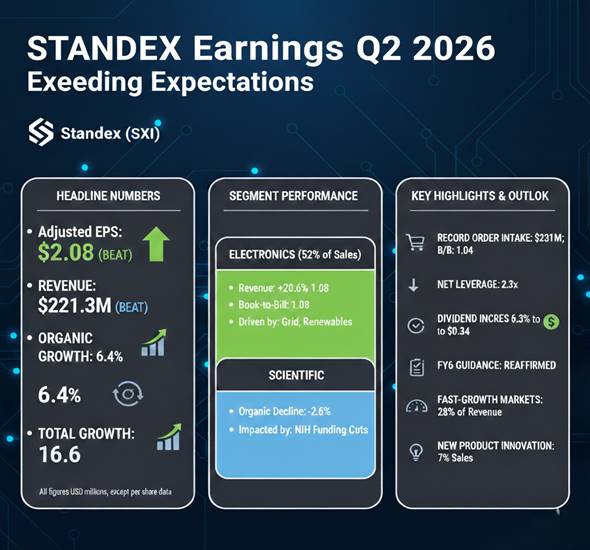

Standex International Corporation (NYSE: SXI) reported second-quarter fiscal 2026 financial results that exceeded analyst expectations for both earnings and revenue, bolstered by double-digit organic growth in its electronics division and the integration of recent acquisitions. The diversified industrial manufacturer posted adjusted diluted earnings per share of $2.08, outperforming the consensus estimate of $2.00. Revenue for the period ending December 31, 2025, rose 16.6% year-on-year to $221.3 million, marginally ahead of the $219.2 million anticipated by the market. Following the announcement, the company’s shares reached a new 52-week high, trading as high as $258.05 as investors responded to record order intake and a reaffirmed full-year outlook.

Core Performance and Segment Analysis

The quarterly performance was characterized by a combination of organic expansion and strategic inorganic growth. Organic revenue increased 6.4%, while acquisitions—notably McStarlite in the Engineering Technologies segment—contributed 9.4% to the top line. Favorable foreign currency movements added a further 0.8%.

The Electronics segment, which represents approximately 52% of total group sales, remained the primary engine of growth. Revenue in this division climbed 20.6% to $115.7 million, driven by demand in fast-growth markets such as the electrical grid and renewable energy. This segment reported a robust book-to-bill ratio of 1.08, signaling a continued backlog of demand.

Conversely, the Scientific segment faced headwinds, reporting an organic decline of 2.6%. Management attributed this softness to reduced demand from academic and research institutions, which have been impacted by recent cuts in National Institutes of Health (NIH) funding. However, the impact was partially mitigated by acquisition contributions within the sector.

Key Financial Metrics (Q2 FY2026)

| Metric | Q2 FY2026 | Q2 FY2025 | Year-over-Year Change |

| Net Sales | $221.3M | $189.8M | +16.6% |

| Adjusted Operating Income | $42.2M | $35.5M | +18.9% |

| Adjusted Operating Margin | 19.0% | 18.7% | +30 bps |

| Adjusted Diluted EPS | $2.08 | $1.91 | +8.9% |

| Free Cash Flow | $13.0M | $2.2M | +506.5% |

Strategic Growth Drivers and Executive Commentary

Standex’s “growth engine” strategy appears to be gaining traction, particularly through its focus on high-margin, high-growth end markets. Sales into these “fast-growth” markets accounted for approximately 28% of total revenue in the quarter, totaling $61 million. Additionally, new product innovation contributed roughly 7% to the quarterly sales total.

In a statement accompanying the results, President and Chief Executive Officer, David Dunbar, noted that the company’s long-term efforts to reposition itself are now manifesting in consistent top-line results. He highlighted the record quarterly order intake of $231 million and a consolidated book-to-bill ratio of 1.04 as indicators of sustained momentum heading into the second half of the fiscal year.

Chief Financial Officer, Ademir Sarcevic, emphasized the company’s disciplined capital allocation, noting that Standex reduced its net leverage ratio to 2.3x after repaying $10 million in debt during the quarter. The company also declared its 246th consecutive quarterly dividend, increasing the payout by 6.3% to $0.34 per share.

Business Outlook and Industry Context

Standex reiterated its full-year fiscal 2026 guidance, projecting revenue growth of more than $110 million over fiscal 2025 levels. This forecast is predicated on:

- Electronics: Expected mid-to-high single-digit organic growth.

- Engineering Technologies: Anticipated double-digit organic growth.

- Innovation: The release of more than 15 new products, expected to contribute 300 basis points of incremental growth.

The broader industrial sector continues to navigate a complex macro environment characterized by shifting trade policies and fluctuating demand in general industrial markets. While Standex has demonstrated resilience through its diversified portfolio, management cautioned that the outlook remains subject to potential global trade or tariff-related disruptions. For the upcoming third fiscal quarter, the company anticipates “significantly higher” year-on-year revenue, supported by a recovery in general industrial demand and continued strength in the defense and aviation sectors.