Stanley Black & Decker Inc. (NYSE: SWK) reported fourth-quarter 2025 earnings that exceeded analyst expectations on Wednesday, as aggressive cost-reduction measures and pricing actions successfully offset a decline in sales volumes. While revenue fell short of consensus estimates due to persistent retail softness in North America, the industrial toolmaker underscored its commitment to balance sheet optimization by announcing a $1.8 billion divestiture of its aerospace manufacturing business.

The company’s quarterly performance reflected a continued divergence between its primary business segments. The Tools & Outdoor division faced a difficult retail environment, while the Engineered Fastening segment benefited from sustained demand in the aerospace and automotive sectors.

Financial Performance and Segment Results

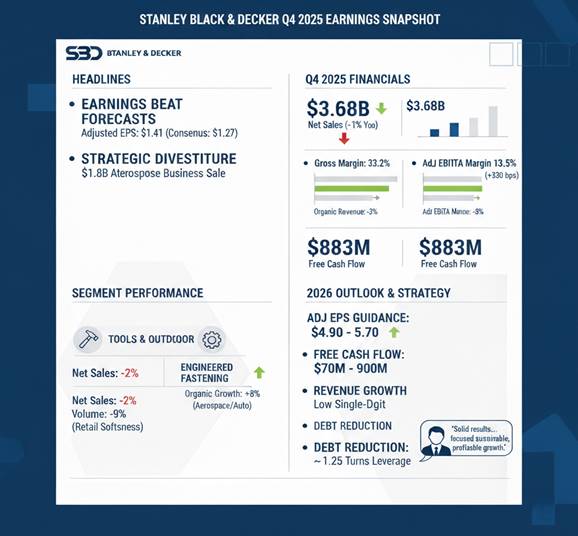

For the quarter ended December 2025, Stanley Black & Decker reported adjusted earnings per share (EPS) of $1.41, surpassing the Zacks Consensus Estimate of $1.27. However, this figure represented a decrease from the $1.49 per share earned in the same period a year prior. Net sales for the quarter reached $3.68 billion, a 1% year-over-year decline that missed the $3.78 billion targeted by analysts.

The top-line contraction was primarily driven by a 7% decline in overall volume, which outweighed a 4% benefit from higher pricing and a 2% favorable impact from currency fluctuations. On an organic basis, revenues fell by 3%.

Key Fourth-Quarter Financial Metrics:

- Adjusted EPS: $1.41 (Consensus: $1.27)

- Net Sales: $3.68 billion (Consensus: $3.78 billion)

- Gross Margin: 33.2% (Up 240 basis points year-over-year)

- Adjusted EBITDA Margin: 13.5% (Up 330 basis points year-over-year)

- Free Cash Flow: $883 million

The Tools & Outdoor segment saw net sales decline 2% to approximately $3.1 billion. Management attributed the 9% volume decline in this segment to “opening price point” products and reduced demand in North American retail channels. Conversely, the Engineered Fastening segment reported a 6% increase in net sales, bolstered by an 8% rise in organic revenue and strong volume growth in the aerospace sector.

Strategic Divestiture and Debt Reduction

A central pillar of the fourth-quarter announcement was the definitive agreement to divest the Consolidated Aerospace Manufacturing (CAM) business for $1.8 billion in cash. The company expects net proceeds of approximately $1.525 billion to $1.6 billion after taxes and fees.

Proceeds from the sale are earmarked for debt reduction, a move intended to lower the company’s leverage by approximately 1 to 1.25 turns. This strategic exit follows the company’s stated objective to simplify its portfolio and focus on its core leadership in the tools and outdoor markets.

“Stanley Black & Decker delivered solid results across our key focus areas in 2025, with continued gross margin and net income growth, strong free cash flow, and a strengthened balance sheet,” said Chris Nelson, President and CEO. He noted that strategic investments remain focused on driving sustainable, profitable growth.

Operational Efficiency and Cost Management

The company reached a significant milestone in its Global Cost Reduction Program, which has now generated $2.1 billion in pre-tax run-rate savings since its inception in mid-2022. During the fourth quarter alone, the program contributed approximately $120 million in incremental savings. These efficiencies were instrumental in expanding the adjusted gross margin to 33.3%, a 210 basis point improvement over the prior year.

2026 Outlook and Industry Context

Looking ahead to 2026, Stanley Black & Decker issued guidance that reflects a cautious but improving outlook. The company expects full-year adjusted EPS to range between $4.90 and $5.70, with the midpoint suggesting 13% growth over 2025 levels. However, the forecast was slightly below some analyst expectations of $5.66.

2026 Guidance Summary:

- Adjusted EPS: $4.90 – $5.70

- Free Cash Flow: $700 million – $900 million

- Revenue Growth: Low single-digit total and organic growth

- Brand Investment: Incremental $75 million – $100 million in SG&A spending

The company faces a complex macroeconomic backdrop, including the lingering impact of tariffs and a transition of its gas-powered walk-behind outdoor products to a licensing model. Management noted that first-quarter 2026 results are expected to be pressured by peak tariff expenses, with gross margins likely to remain flat before resuming expansion in the second half of the year.

As of Wednesday’s market close, shares of Stanley Black & Decker (SWK) remained relatively flat, as investors weighed the earnings beat and debt-reduction strategy against the softer-than-expected revenue and 2026 profit outlook.