Shares of Starbucks Corporation (NASDAQ: SBUX) stayed red on Friday. The stock has dropped 8% in the past three months. The coffeehouse chain is in the midst of a turnaround effort against a backdrop of continued sales declines in its largest market, North America. Even as it appears to make progress on many fronts, it recently announced a number of store closures and job cuts in this region.

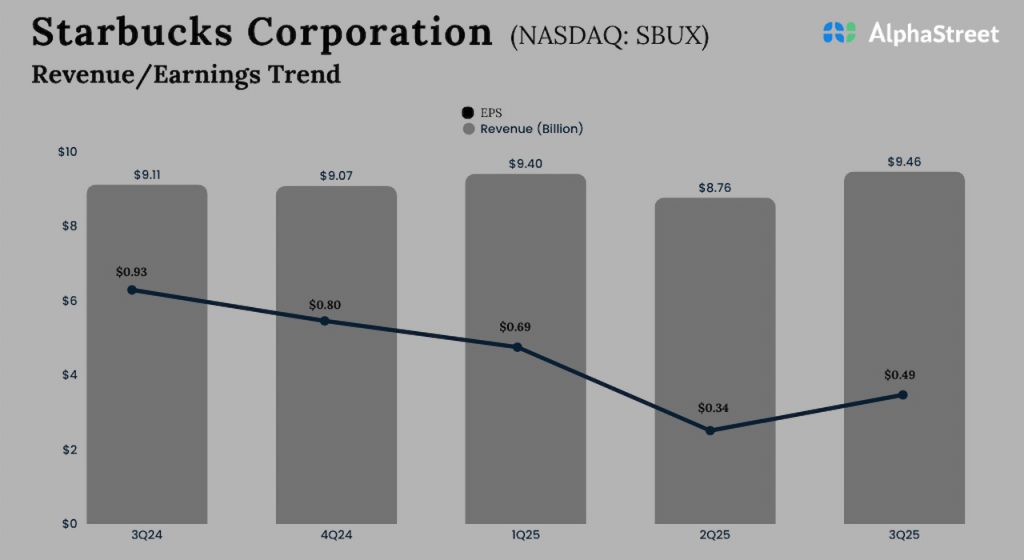

Recent quarterly performance

In Q3 2025, Starbucks’ revenue in North America increased 2% to $6.9 billion. However, its comparable store sales in the region declined 2%, marking the sixth quarterly decline in a row. The decrease in comparable store sales was driven by a 3% drop in comparable transactions, partly offset by a 1% increase in average ticket.

Comparable store sales in the US decreased 2%, driven by a 4% decline in transactions, partly offset by a 2% rise in average ticket. Transactions were impacted by the lapping of highly-discounted promotions in the previous year. However, the company is seeing improvement in its transaction comps. It is also seeing improvements in transactions from both members and non-members of its Starbucks Rewards loyalty program.

SBUX saw a decline in US licensed store portfolio revenue in the third quarter, driven by grocery and retail channels. Meanwhile, Canada’s sales comp grew in the low single-digits, driven by product innovation, mainly in food.

Initiatives

SBUX has been investing in stores, menu innovation and marketing as part of its Back to Starbucks strategy, and it has been seeing progress across many areas. The company is seeing gains from Gen Z and millennial customers, who make up half of the customer base. It is seeing improvements in full-day transaction comps and morning transactions.

Starbucks’ in-café, drive-thru, and digital businesses are performing well and it is seeing growth in its delivery business that saw transactions grow over 25% year-over-year. The company is working on uplifting its coffeehouses for which it is targeting an investment of around $150,000 per store. It aims to complete at least 1,000 uplifts across North America by the end of calendar year 2026. SBUX is also focusing on product innovation and is rolling out new items on its menu.

Store closures and job cuts

Last month, Starbucks announced plans to close several of its coffeehouses in North America where it is unable to create a physical environment or generate financial performance as per expectations. The company estimates its overall company-operated count in North America to decline by about 1% in FY2025 after taking into account openings and closures.

SBUX plans to end FY2025 with nearly 18,300 Starbucks locations across the US and Canada. It is also eliminating around 900 non-retail partner roles and closing many open positions as part of its efforts to reduce non-retail headcount and expenses.

Given the uncertain consumer environment, Starbucks remains cautious on the trends in its US company-operated business in the fourth quarter of 2025. It remains to be seen when the company’s turnaround plan will generate solid returns.