AlphaStreet Newsdesk powered by AlphaStreet Intelligence

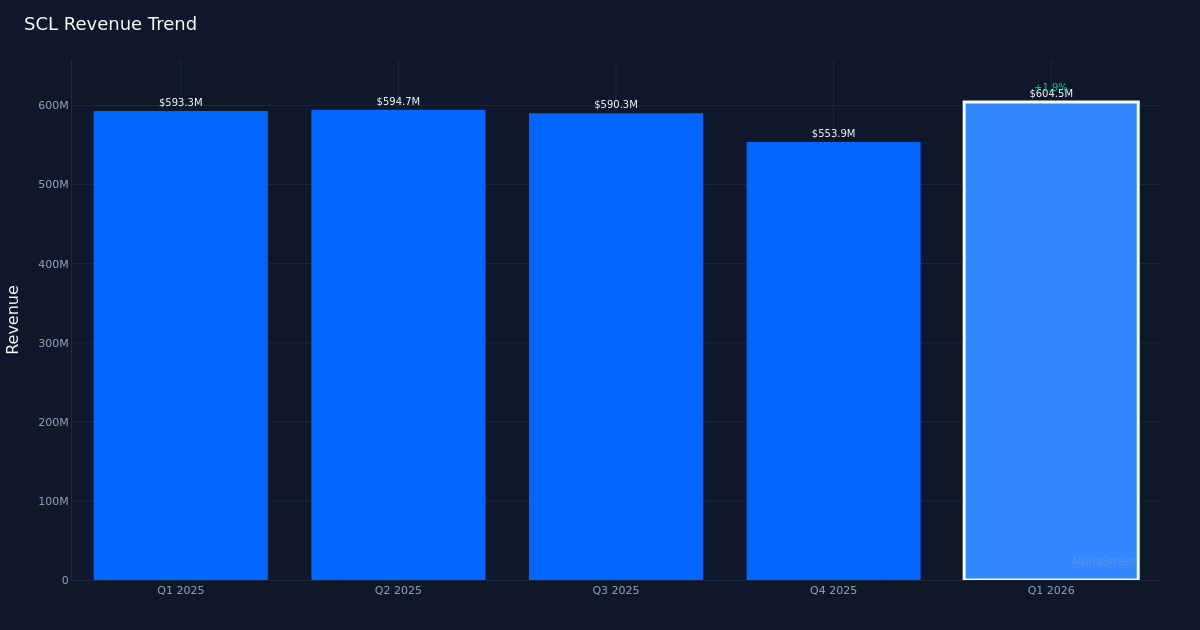

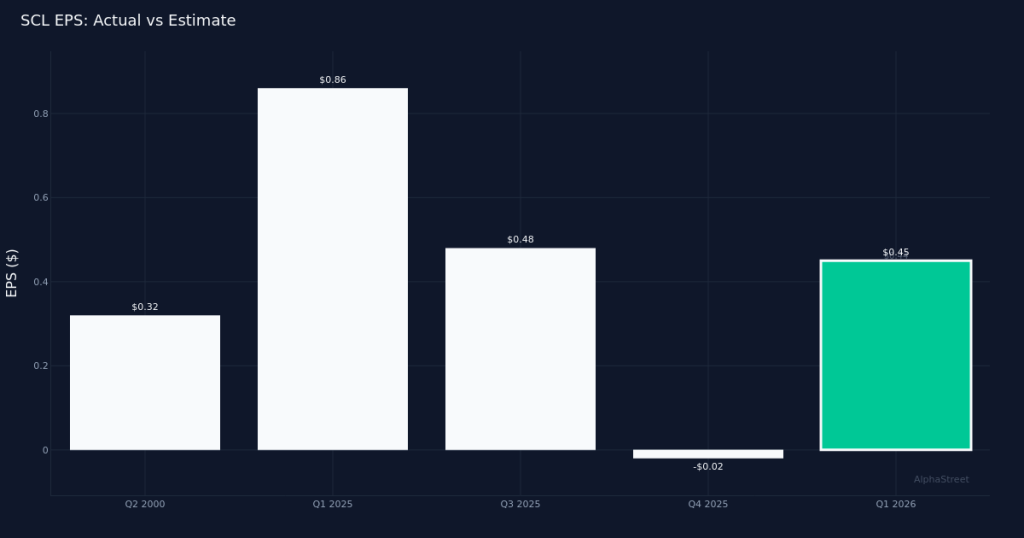

Modest beat delivered. Stepan Company (NYSE: SCL) reported Q1 2026 adjusted earnings of $0.45 per share, edging past the $0.44 consensus estimate by 2.3% in a quarter marked by flat volume growth and modest revenue expansion. The specialty chemicals manufacturer generated $604.5M in revenue for the quarter, representing a 2.0% increase from the $593.3M recorded in Q1 2025, while adjusted net income reached $10.3M. The stock traded up following the release, suggesting investors found comfort in the company’s ability to navigate a challenging demand environment while maintaining profitability.

Volume stagnation persists. The headline revenue growth masks underlying weakness in demand, with organic sales volume registering at 0.0% for the quarter. This flat volume performance indicates that the year-over-year revenue gain was driven entirely by pricing actions rather than end-market expansion—a less durable foundation for growth that raises questions about the sustainability of the company’s top-line momentum. For a specialty chemicals supplier, stagnant volumes typically signal either market share challenges or broader destocking trends among customers across industrial and consumer end markets.

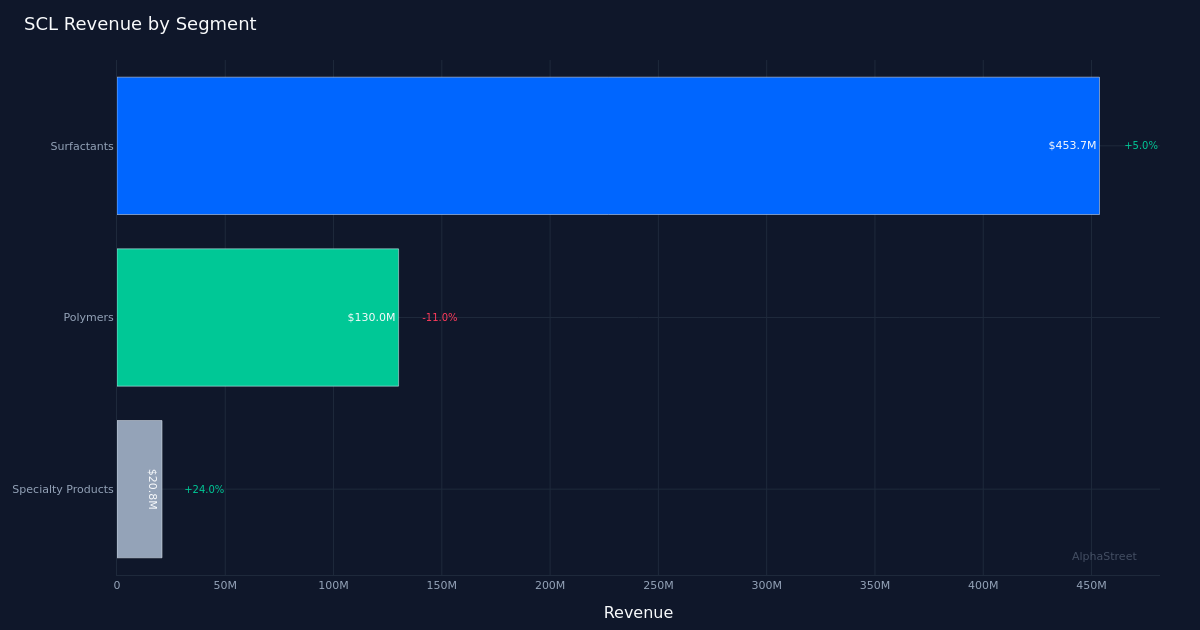

Surfactants carry the load. The Surfactants segment led performance with $453.7M in revenue, up 5.0% year-over-year, demonstrating resilience in Stepan’s core business serving detergent, personal care, and industrial cleaning applications. This segment’s outperformance relative to the company’s overall 2.0% revenue growth suggests other divisions faced headwinds, though specific segment-level profitability metrics were not disclosed. The surfactants strength likely reflects sticky customer relationships and the mission-critical nature of these ingredients in formulated products, where switching costs provide some insulation from demand volatility.

Quality of beat questioned. The narrow earnings beat of just one cent per share, combined with flat organic volumes, suggests margin management rather than robust operational performance drove the result. Adjusted net income of $10.3M on revenue of $604.5M points to margin pressures that required careful cost control to deliver the modest upside. Institutional investors should scrutinize whether the earnings delivery relied on temporary cost actions or sustainable operational improvements—a distinction that will determine whether the company can sustain profitability as pricing power potentially moderates.

Analyst sentiment measured. Wall Street maintains a cautiously optimistic stance with consensus standing at 3 buy ratings, 1 hold, and 0 sell recommendations. This positioning reflects recognition of Stepan’s market position in specialty surfactants while acknowledging the challenges posed by industrial demand uncertainty and the company’s need to reignite volume growth to justify further multiple expansion.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.