International Business Machines Corporation (NYSE: IBM) is in the final phase of its transformation from a conventional IT service provider to a diversified tech firm focused on cloud computing and artificial intelligence. The new model would enable the company to achieve solid revenue growth in the long term while enhancing shareholder returns.

The tech titan’s stock made a surprise recovery after being hit by the market selloff initially. The question is whether it can sustain its strength in the current market situation that is highly volatile. After regular hikes, IBM’s current dividend yield is an impressive 4.9%, which is above the industry average. The prospects of handsome shareholder returns should encourage those planning to invest in the technology behemoth, which has solid fundamentals and a healthy balance sheet. In short, it is a safe bet from the long-term perspective.

International Business Machines Corporation Q1 2022 Earnings Call Transcript

The new IBM is all set to enjoy the fruits of the many transformational initiatives it took in recent years, including strategic M&A deals like the Red Hat acquisition and the Kyndryl spin-off. It is expected that the leadership of Arvind Krishna, the cloud veteran whole assumed the role of CEO in 2020, would catalyze the company’s transition to a bigger and smarter business.

Cloud Power

It is estimated that the hybrid cloud industry’s value would more than double in the next five years, a trend that bodes well for IBM because its main offering is the hybrid cloud platform now. For the company, a key priority has been the development of AI capabilities that helped it broaden the addressable market significantly.

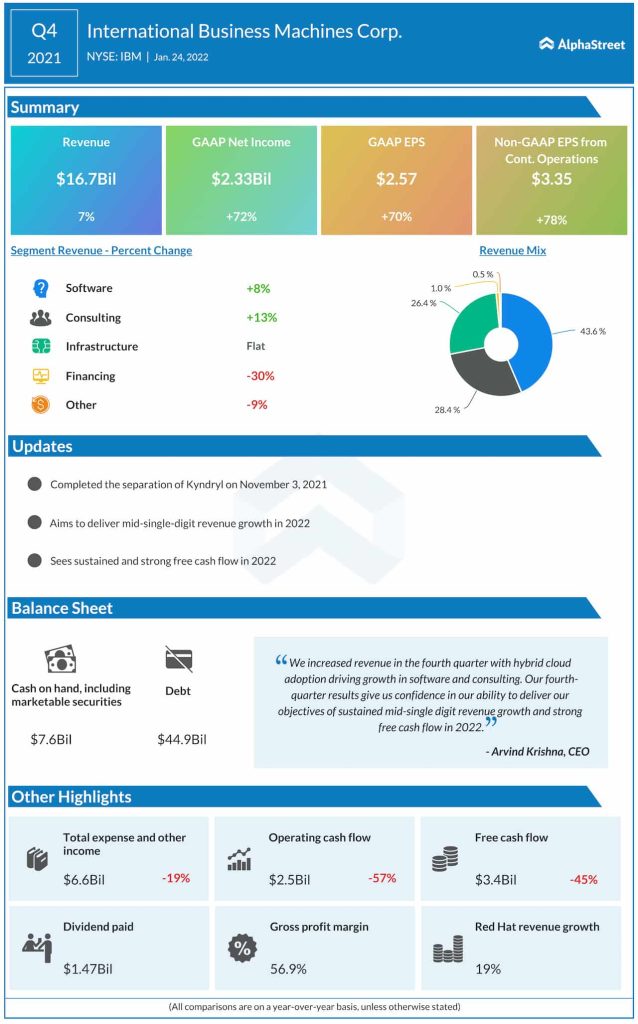

Over the years, IBM has maintained strong profitability — consistently recording better-than-expected earnings — thanks to its efforts to optimize the portfolio and effective go-to-market strategy. The company entered the new fiscal year on a mixed note, reporting an 8% increase in revenues to $14.2 billion and a decline in net profit to $0.81 per share. A double-digit increase in the software and consulting segments more than offset weakness in the other divisions.

Meanwhile, the relatively high valuation, combined with experts’ mixed views on the stock’s near-term gains, might discourage a section of investors, especially those looking for short-term engagement.

Q2 Data on Tap

Second-quarter results are expected to be published on July 18 after the regular trading hours. Market watchers are not very optimistic about the overall performance, and warn of a marked decline in revenues to $15.25 billion for the three-month period. The weakness in the top line could translate into a 2% drop in adjusted earnings to $0.28 per share.

“Over the last two years, we have been optimizing our portfolio, expanding our ecosystem, and simplifying our go-to-market to capture this demand. This quarter, we again had double-digit revenue growth in consulting, and software growth reflects solid performance across the portfolio. Our infrastructure business as always reflects product cycle dynamics,” said Arvind Krishna while interacting with analysts a few weeks ago.

Microsoft’s acquisition of Activision looks like a win-win deal. Here’s why

It was a roller-coaster ride for IBM’s stock so far this year, but it maintained an uptrend. Over the past six months, the shares gained about 3%, which is better than the general market trend. They closed the last trading session higher.