Stitch Fix, Inc. (NASDAQ: SFIX) is going through a rough patch after being hit by headwinds like the virus-related disruption and economic uncertainty. The online personal styling company has been struggling to stay profitable for quite some time. Faltering sales and a shrinking user base have forced the management to take measures like aggressive headcount reduction.

The company’s stock has slipped to an all-time low, with the weak third-quarter results adding to the downturn this week. Investor sentiment was dampened particularly by the loss of around 200,000 customers since last year. Overall, things don’t seem to be in favor of the company, which is yet to come up with a convincing revival plan. Though the stock is expected to hit the recovery path this year, the underlying weakness would remain a concern for investors.

Read management/analysts’ comments on Stitch Fix’s Q3 2023 results

On the plus side, SFIX is extremely cheap at the current valuation but is unlikely to bring meaningful returns to shareholders. When it comes to owning or selling the stock, it would be a good idea to wait until a clearer picture emerges.

Slowdown

Like most enterprises engaged in customer discretionary business, Stitch Fix’s sales got affected when people tightened their purse strings in response to the pandemic-induced financial uncertainty. But unlike others, the company failed to revise the business when market conditions improved.

From Stitch Fix’s Q3 2022 earnings conference call:

“In terms of the current macroeconomic environment, we continue to navigate the ongoing uncertainties that many in our industry are experiencing, including supply chain constraints, global inflationary pressures, and potential shifts in customer demand. We are optimistic about our path to capturing the opportunities ahead. Though these transformational moments take time, we are confident in the company we are building and our ability to overcome our current challenges.”

Financial Performance

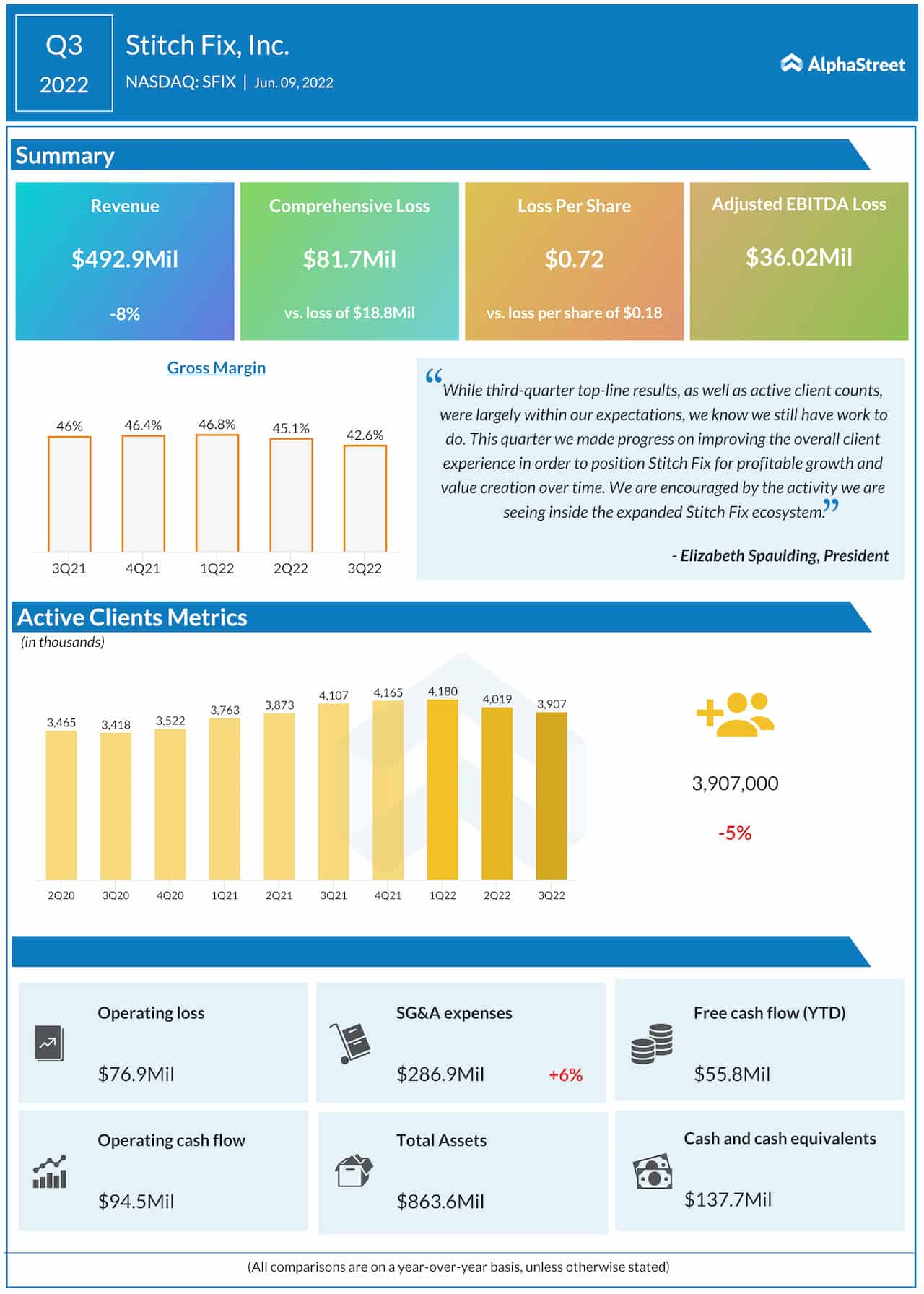

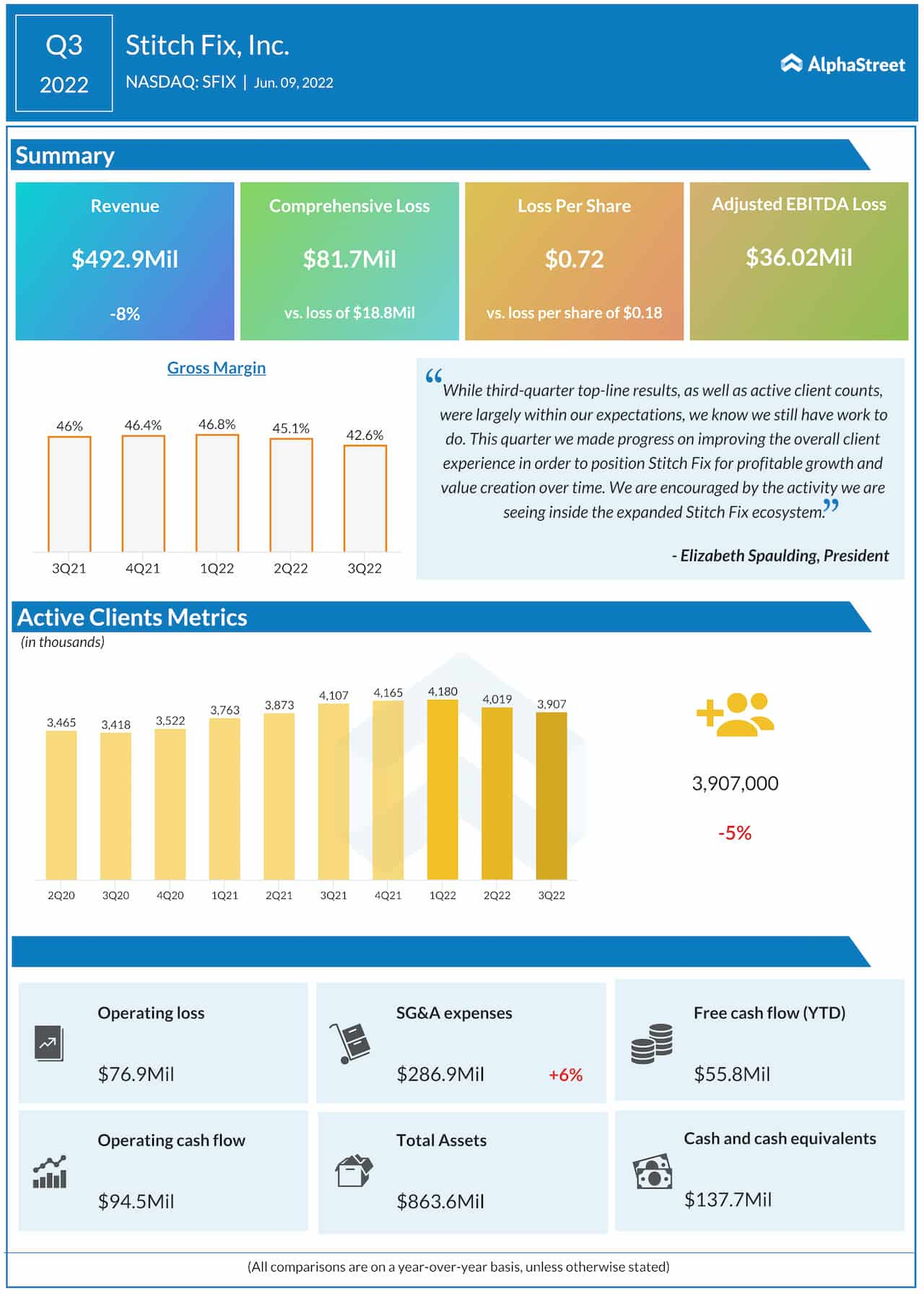

The financial performance in the most recent quarter was quite disappointing, with the bottom-line languishing in the negative territory hurt by an 8% fall in revenues to $493 million. The company has reported negative earnings for three consecutive quarters. Third-quarter loss widened sharply to $0.72 per share and missed Wall Street’s projection. Margins were squeezed by higher operating costs.

Nike set to create long-term shareholder value. Is the stock a buy?

The management is going for a major restructuring to streamline the struggling business, which includes laying off around 4% of the company’s workforce. While the initiative would result in additional costs in the near term, it is expected to bring the business back to profitability in the long term.

Extending the post-earnings slump, Stitch Fix’s stock closed the last trading session sharply lower. The value has more than halved in the past six months and the stock slipped into the single-digit territory.