After a prolonged slowdown, the restaurant industry is returning to normal patterns but macroeconomic uncertainties and high inflation are currently playing spoilsport for it. While the pandemic-related slump forced many small restaurants to close shop, big players like Darden Restaurants, Inc. (NYSE: DRI) mostly stayed unaffected and even expanded market share when markets reopened.

Darden’s revamped food delivery service helped it beat the pandemic woes to a large extent but the inflation-induced stress on customers’ personal finances is currently weighing on sales. With more interest rate hikes in the cards, the picture might get bleaker going forward. The situation demands the right balance between pricing and continued investment in the business.

The Stock

The Orlando-based company, which owns popular restaurant chains like Olive Garden and LongHorn Steakhouse, has been paying dividends for more than a decade. While the 3% yield looks impressive, the stock seems to have become less attractive for income investors after the company slashed the dividend in the past.

Read management/analysts’ comments on Darden’s Q1 results

DRI mostly outperformed the market this year, though it experienced continued volatility after peaking last year and lost about 22% since then. It is estimated that the stock, which is trading close to $120, will reach $138 in the next twelve months, which is slightly above its long-term average. Being the largest restaurant chain in the country, Darden has what it takes to overcome temporary headwinds and continue creating value for shareholders. It is a relatively safe bet for long-term investors. However, it will be a good idea to wait until the macro issues settle down before making buying/selling decisions.

When it comes to pricing, high input costs amid elevated inflation would remain a concern in the near future. Operating costs and expenses rose 16% in the most recent quarter. The good news is that the scale of the business, supported by the company’s large restaurant network, would help ease the impact of inflation on the bottom line to a large extent.

From Darden Restaurant’s Q1 2023 earnings conference call:

“We expect total inflation and our gap between pricing and inflation to have peaked in the first quarter. We also expect inflation to moderate throughout the remainder of the year while our pricing gap should narrow in both the second and third quarter and then reverts in the fourth quarter. And while we have commodities inflation risk in the back half of the year, we have pricing plans ready to put into action, which will help preserve our targeted gap to inflation for the year if we see inflation higher than our expectations.”

Key Numbers

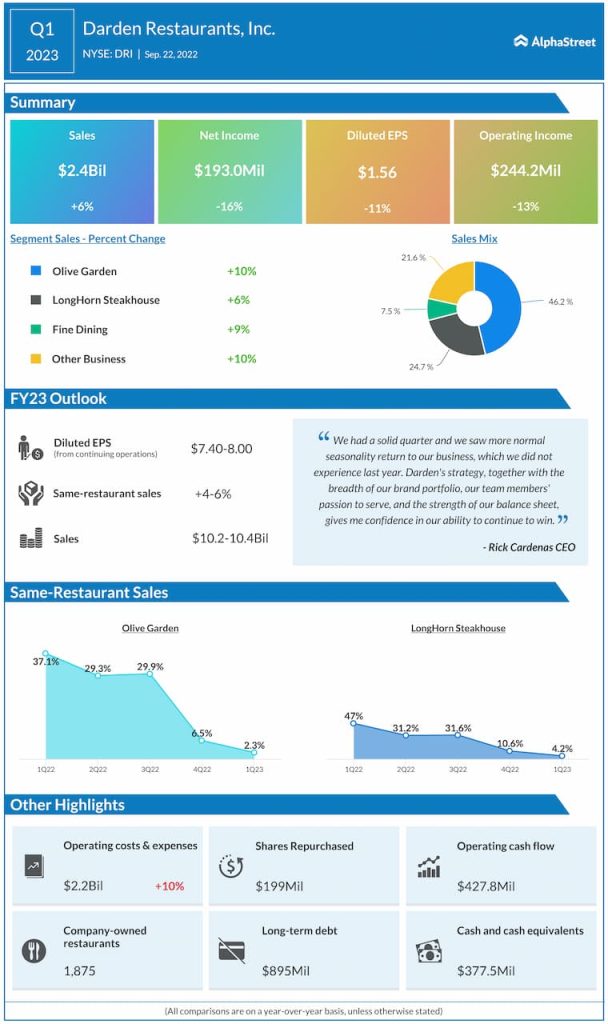

Darden’s net profit matched estimates in the first quarter, after exceeding expectations in the previous quarter. However, earnings declined 11% annually to $1.56 per share on revenues of $2.4 billion, which is up 6% year-over-year. All four operating segments registered growth, while comparable store sales continued to weaken. At the end of the quarter, the company had 1,875 company-owned stores. Meanwhile, the management reaffirmed its full-year outlook.

General Mills expects the inflationary environment to impact its FY2023 performance

Shares of Darden closed the last trading session lower, a trend that continued since it reported mixed first-quarter results last week. DRI has lost about 7% in the past six months.