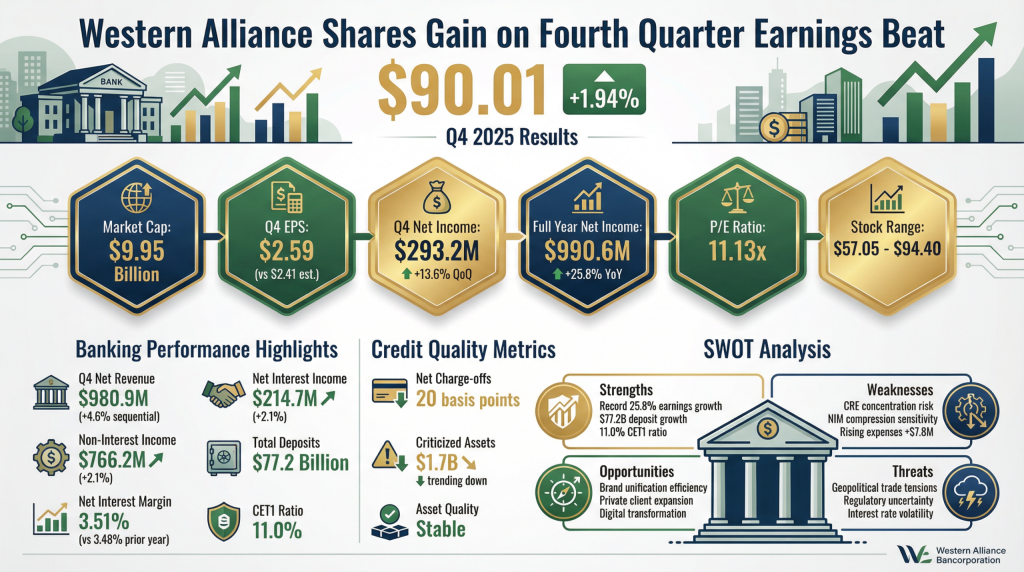

Strengths

- Record Earnings: Net income grew 25.8% for the full year 2025, demonstrating strong operational recovery.

- Deposit Growth: Total deposits reached $77.2 billion, with high growth in noninterest-bearing balances.

- Capital Position: CET1 ratio of 11.0% provides a robust buffer above regulatory requirements.

Weaknesses

- Concentration Risk: Significant exposure to Commercial Real Estate (CRE) and specialized tech sectors.

- Margin Compression: NIM remains sensitive to deposit repricing and competition for funding.

- Non-Interest Expense: Salaries and professional fees increased by $7.8 million in the final quarter.

Opportunities

- Brand Unification: Consolidation of legacy brands into “Western Alliance Bank” is expected to drive marketing efficiency.

- Private Client Expansion: New hubs in Beverly Hills and Las Vegas target high-margin affluent banking.

- Digital Transformation: Investment in cybersecurity and digital channels to improve efficiency ratios.

Threats

- Geopolitical Volatility: Trade wars and tariffs could stress the credit profiles of commercial manufacturing clients.

- Regulatory Uncertainty: Potential changes in “Large Financial Institution” (LFI) thresholds could increase compliance costs.

- Interest Rate Volatility: A “higher-for-longer” rate environment may increase loan default rates in sensitive industries.