It’s been a year since Elon Musk’s “taking private” tweet

debacle, but bear assaults seem to be a constant companion to his firm. Though

the CEO seems to have toned down a bit since then, the stock has hardly

recuperated. While Musk wanted to take Tesla (NASDAQ:

TSLA) private at $420, the stock is currently trading at $227.5, down 26%

in the trailing 12 months.

Tesla undoubtedly makes some of the best premium electric vehicles. But analysts and market watchers are questioning how long it can continue to do that. The rising pessimism is fuelled by five factors, which have gained relevance now more than ever before.

Weakness in China

The overall weakness in the Chinese automobile industry seems to have spread to the electric vehicles segment also. In July, sales of new electric vehicles fell 4.7%, as per data revealed by the China Association of Automobile Manufacture. This is not good news to Tesla, which is building a factory in Shanghai, using its very limited cash resources, to boost sales in this region.

The slowdown comes as a double-whammy in the backdrop of Yuan depreciation. Tesla may be forced to raise the price tag on its cars to offset the currency issue, making them more expensive to Chinese customers.

Separately, the weakness in British Pound and Euro should dent revenues coming from Europe.

READ: Virgin Galactic vs. Blue Origin: The race to suborbital space tourism

Tax credit expiry

The federal tax credit on electric vehicles have been halved recently to just $1,875 and will be completely taken off starting next year.

Separately, market observers predict a drastic fall in oil prices driven by an economic recession by around next year. With gas prices low and tax credit lifted, customers will have fewer reasons to shift to more expensive electric vehicles.

Losing investor/analyst

confidence

Tesla had never been a darling among the Wall Street analysts. Yet, being a public company, it cannot entirely stay indifferent towards their contribution to the stock movement. According to TipRanks, 14 out of 27 analysts covering the stock has a sell rating on it.

Making matters worse, disappointing earnings performances over the past few quarters are validating the criticisms of these analysts, taking a toll on investor confidence as well.

Recently, Korea Investment Corp, a major investor, halved its stake in the company, by selling 18,700 shares. It also raised its investment in Tesla rival General Motors (NYSE: GM) and initiated a position in another rival Uber Technologies (NYSE: UBER).

Disappointing bottom-line

performance

One of the most repulsive factors about this company is its inability to deliver promising bottom-line results. In three of the trailing four quarters, Tesla has lagged behind market estimates. In the most recent quarterly results, the Model 3-maker posted losses that were over three times wider than market estimates.

Tesla needs to give investors a long-term narrative to maintain their confidence.

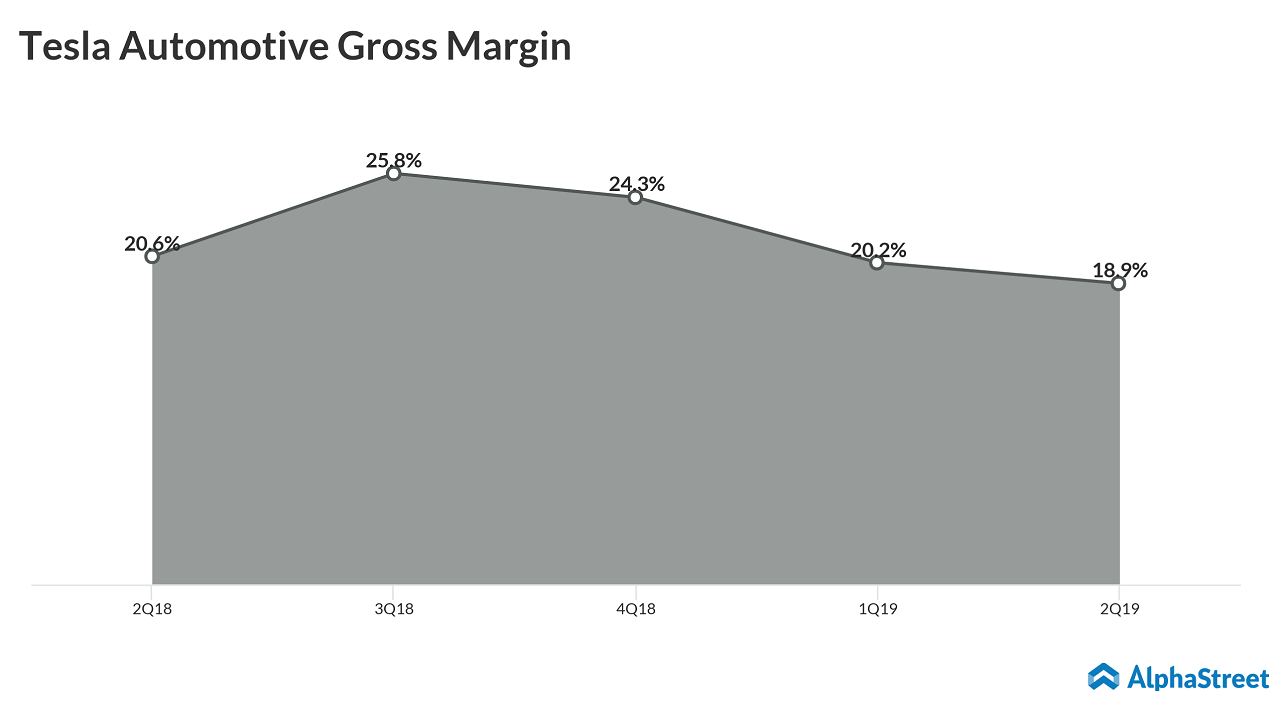

Downtrend in margins

According to sell-side analysts, the key to Tesla’s profitability lies in self-driving technology, which is also notorious for high cash burn. The instability in the executive level and lack of clarity with regards to autonomous driving in different regions of the world act as a headwind to the cash-strapped firm.

If Tesla continues to cut prices of vehicles at its home market, it would further squeeze margins, making it more difficult to become profitable in the long run.

Get access to timely and accurate verbatim transcripts that are published within hours of the event.