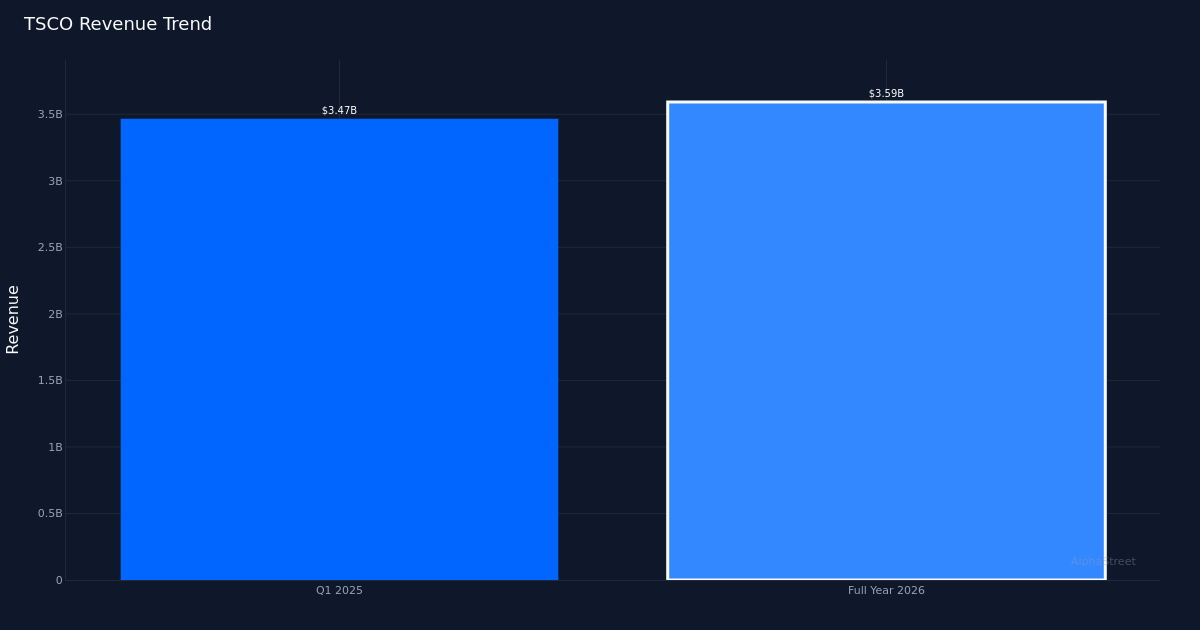

Mixed quarter. Tractor Supply Company (NASDAQ: TSCO) delivered a modest Q1 2026 performance that largely met investor expectations, with diluted EPS of $0.31 and revenue of $3.59B for the period. While the top line advanced 3.6% from the $3.47B recorded in Q1 2025, profitability weakened as EPS declined 8.8% from the $0.34 posted in the year-ago quarter. Net income reached $164.5M for the quarter, reflecting margin pressure in what remains a challenging environment for discretionary rural lifestyle purchases. The stock traded largely unchanged following the release, suggesting the market had appropriately calibrated expectations for this transitional period.

Sluggish comp momentum. The specialty retailer’s comparable store sales growth of just 0.5% for the quarter underscores the difficulty management faces in driving organic traffic and ticket growth across its mature store base. With 2,641 total stores in operation at quarter-end, the company’s footprint expansion continues, but the near-flat comp performance points to headwinds from consumer wallet pressure in rural markets and ongoing normalization after pandemic-era demand spikes for outdoor and agricultural products. The deceleration in same-store activity appears to be the primary culprit behind the margin compression that drove EPS lower despite modest revenue gains.

Guidance signals caution. Management’s forward outlook reflects a conservative stance on the balance of the year, projecting FY 2026 adjusted EPS in the $2.13 to $2.23 range. The full-year earnings guidance implies roughly flat to modest growth from current run rates, indicating the company does not anticipate a material near-term inflection in either traffic trends or gross margin recovery. This tempered outlook aligns with broader softness observed across discretionary retail categories serving price-sensitive customer segments.

Street remains divided. The analyst community shows mixed conviction on the stock, with Wall Street consensus standing at 12 Buy ratings, 15 Hold ratings, and zero Sell recommendations. This distribution reflects the investment debate surrounding Tractor Supply’s positioning: bulls point to the company’s defensible rural niche and store growth runway, while more cautious analysts worry about the pace of comp recovery and margin normalization. The lack of sell-side bearish calls suggests limited downside concern, but the predominance of Hold ratings indicates many analysts are waiting for clearer evidence of improving unit economics before upgrading their stance.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.