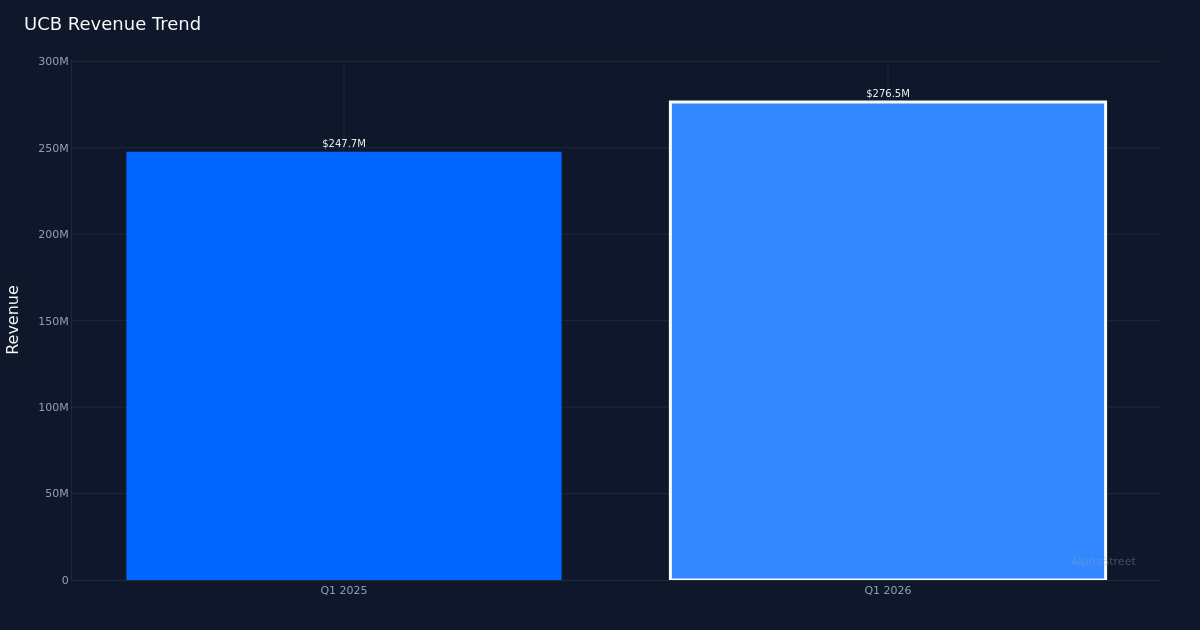

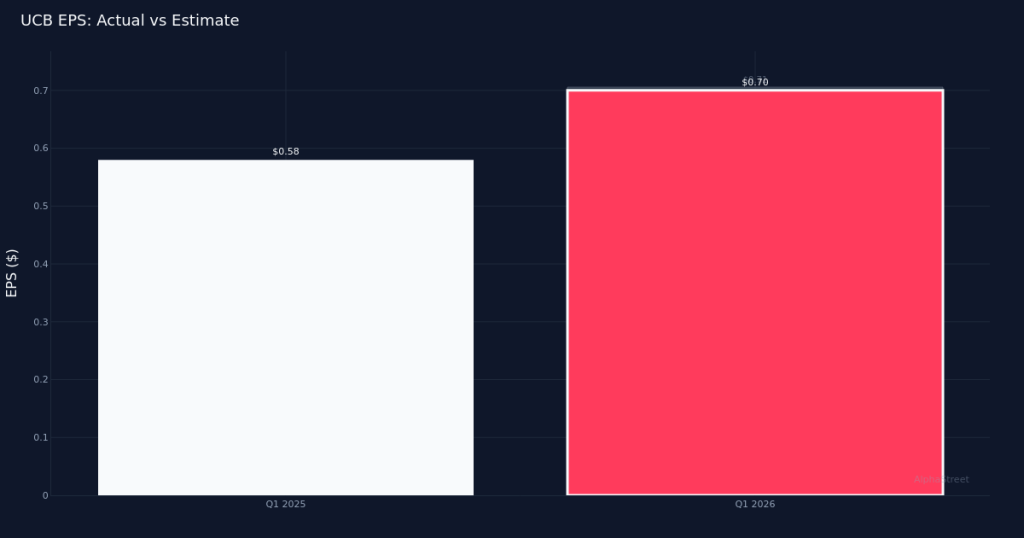

Narrow Miss. United Community Banks, Inc. (UCB) reported Q1 2026 operating earnings of $0.70 per share, falling just short of the $0.71 consensus estimate by 1.4%. Revenue totaled $276.5M for the quarter, representing a 12.0% increase from the $247.7M recorded in Q1 2025. Bottom-line profit came in at $84.7M as the regional bank navigated a challenging interest rate environment while posting solid top-line growth.

Revenue Growth Shines. The quality of this quarter’s results lies squarely in the revenue performance, with the double-digit year-over-year expansion suggesting genuine business momentum rather than financial engineering through cost management. The 12.0% revenue increase demonstrates UCB’s ability to grow its core banking franchise, though the slight earnings miss indicates some pressure on the expense side or credit quality metrics. Net interest margin came in at 3.6% for the quarter, a critical profitability metric for regional banks that reflects the spread between interest earned on loans and interest paid on deposits.

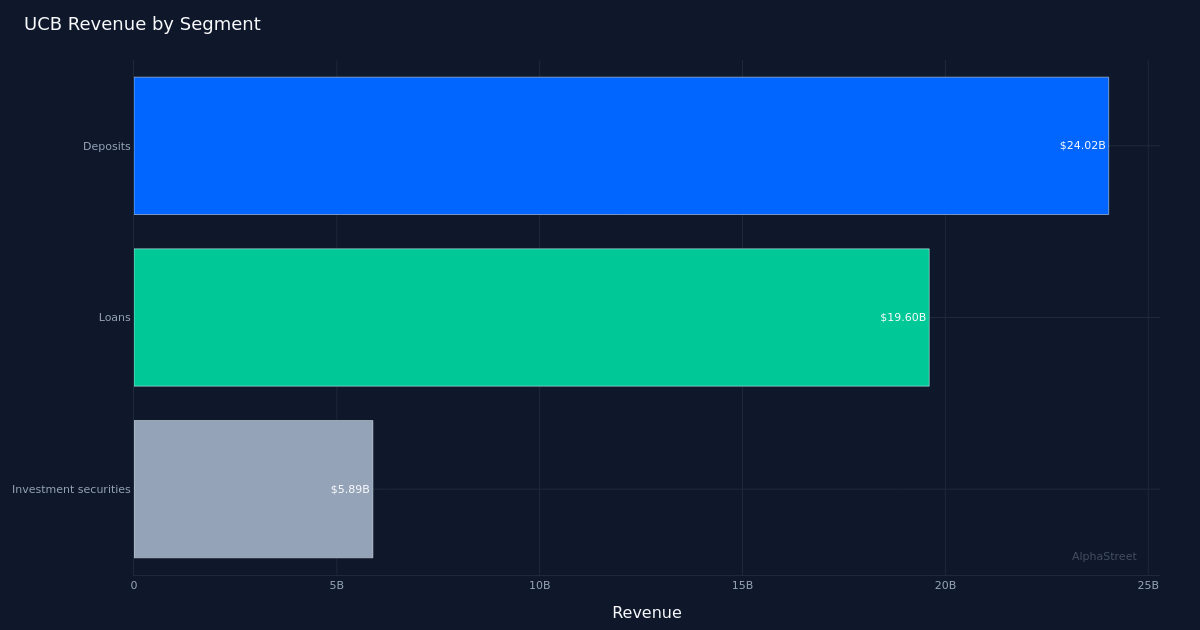

Loan Portfolio Drives Performance. Loans generated $19.60B in revenue for the quarter, underscoring the company’s bread-and-butter lending operations as the primary growth engine. This substantial loan book reflects UCB’s established presence across its regional footprint and its ability to deploy capital into interest-earning assets. The company operated $28.18B in total assets at quarter end, providing a sense of scale for this Southeast-focused regional bank as it competes against both larger national institutions and smaller community players.

Muted Market Reaction. The stock traded largely unchanged following the report, suggesting investors had appropriately calibrated expectations for a modest miss and viewed the strong revenue growth as offsetting the slight earnings shortfall. This neutral response indicates the market is taking a balanced view of UCB’s performance, neither punishing the company for the 1.4% miss nor rewarding it for the robust top-line expansion. The analyst community maintains a cautious stance with Wall Street consensus standing at 3 buy, 6 hold, and 0 sell ratings, reflecting a wait-and-see attitude toward the regional banking sector amid ongoing macroeconomic uncertainty.

Profitability Under Scrutiny. The disconnect between strong revenue growth and the earnings miss warrants attention from investors. While the 12.0% revenue expansion provides a solid foundation, the inability to translate that growth into earnings upside raises questions about either operating leverage or credit provisioning requirements that may be pressuring margins. The 3.6% net interest margin will be a key metric to monitor in coming quarters as regional banks balance deposit costs against loan yields in an evolving rate environment.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.