Trustmark Corporation (NASDAQ: TRMK) reported fourth-quarter 2025 net income of $57.9 million, concluding a fiscal year of record earnings characterized by expanded net interest margins and growth in core lending. The regional financial institution posted diluted earnings per share (EPS) of $0.97 for the quarter, exceeding the consensus analyst estimate of $0.91, while total revenue reached a record $799.8 million for the full year.

Following the announcement, Trustmark shares saw a modest appreciation of approximately 1.3% in early trading, as investors weighed the earnings beat against a slight narrowing of the deposit base on a linked-quarter basis.

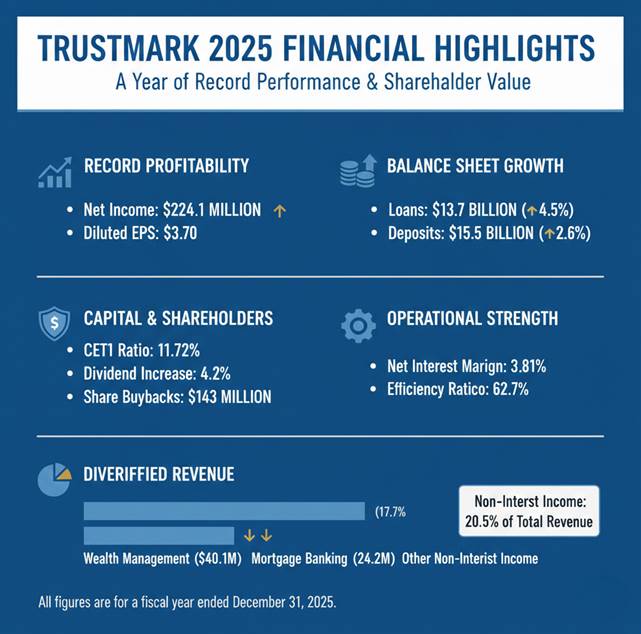

Capital Allocation and Shareholder Returns

During the fourth quarter, the board of directors authorized an increase to the quarterly cash dividend, raising it 4.2% to $0.25 per share. The company also maintained an active capital return profile, repurchasing $43.0 million of its common stock during the final three months of the year.

For the full year 2025, Trustmark returned approximately 61.8% of its net income to shareholders through a combination of dividends and the repurchase of 2.2 million shares. The corporation entered 2026 with a newly authorized $100 million share repurchase program, signaling a continued focus on capital management despite shifting macroeconomic conditions.

Financial Performance and Asset Quality

The bank’s fourth-quarter revenue totaled $204.1 million, a 0.9% increase from the previous quarter. This growth was primarily supported by a net interest margin of 3.81%, which remained resilient despite the costs associated with refinancing $125 million in subordinated debt during the period.

Key annual performance metrics included:

Net Income: $224.1 million for the full year, a record for the company.

Return on Average Tangible Equity: 12.97%.

Loan Growth: Loans held for investment rose 4.5% year-over-year to $13.7 billion.

Credit Quality: Net charge-offs were 0.13% of average loans for the year, though the fourth quarter saw a specific $7.6 million charge-off related to a single, previously reserved commercial credit.

While total deposits grew 2.6% year-over-year to $15.5 billion, the bank reported a $131 million linked-quarter decline. Management attributed this decrease largely to a $219 million reduction in public fund balances, which was partially offset by a 4.4% annual increase in core commercial and personal deposit accounts.

2026 Strategic Outlook

Trustmark’s 2026 guidance projects mid-single-digit growth in both loan and deposit volumes. The bank expects its net interest margin to stabilize between 3.80% and 3.85%, supported by a cost of deposits that decreased to 1.72% in the fourth quarter.

Non-interest income, which accounted for 20.5% of total revenue in 2025, is expected to grow as the bank expands its wealth management and insurance segments. Wealth management revenue specifically reached an all-time high of $40.1 million in 2025, an increase of 7.7% over the prior year.

Macroeconomic and Sector Environment

The results reflect a broader trend among mid-sized regional lenders seeking to balance loan yields against the rising cost of funding. Trustmark’s efficiency ratio of 62.7% and its Common Equity Tier 1 (CET1) ratio of 11.72% suggest a defensive posture designed to withstand potential credit normalization. The bank noted that while criticized and classified loans decreased significantly throughout 2025, the provision for credit losses will likely normalize in 2026 as the industry adjusts to a more stable, yet higher, interest rate environment compared to the previous decade.