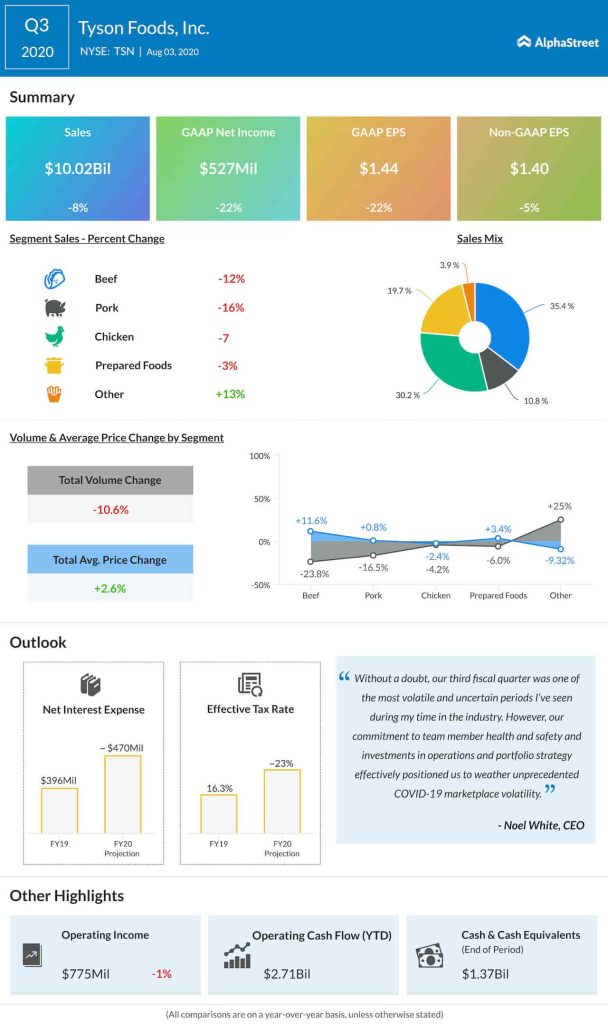

Shares of Tyson Foods Inc. (NYSE: TSN) have dropped 35% since the beginning of this year and 27% over the last 52 weeks. The stock is currently trading 5% below its 50-day moving average of $61.93. Despite facing challenges from the COVID-19 pandemic, the company has managed to remain fairly resilient in the current environment.

Looking ahead, Tyson is optimistic that factors like high demand for protein and momentum in its retail and ecommerce channels could fuel growth in the coming months for the company.

Tailwinds

Tyson’s scale across its products and brands gives it flexibility to adjust according to consumer demand across channels. The pandemic drove a higher demand for core retail and branded products which led to volume growth in the core retail line as well as share gains across these categories. In the third quarter of 2020, volumes grew 26% in retail.

Tyson is also seeing healthy performance in exports. A large part of the company’s export sales comprise of products that are not part of the American diet, and therefore export markets help in optimizing livestock utilization. A shortage in hog supplies due to African swine fever has presented Tyson with the opportunity to fulfil international demand through exports.

Tyson believes that growth in population and income levels globally will lead to a higher demand for protein and the company’s expansion into international markets positions it well to meet this growing demand.

The pandemic has also led to a rapid increase in demand for food through alternative channels like ecommerce. During the third quarter, ecommerce sales more than doubled year-over-year reflecting changes in consumer buying behavior.

The company expects to see high levels of ecommerce demand in channels like grocery and foodservice and plans to take advantage of this trend. Tyson believes its significant investments in automation and technology will help drive strong returns going forward.

Tyson is also broadening its offerings in alternative proteins and witnessed growth in distribution for its new plant-based protein offerings which were rolled out under its Raised & Rooted brand during the third quarter.

Headwinds

Although the pandemic led to increased demand across the retail channel, the foodservice channel witnessed declines. Looking ahead, a meaningful part of the company’s growth depends on food-away-from-home trends which in turn depend on communities remaining open.

The company continues to operate some of its facilities at reduced production levels. This has impacted raw material availability for its Prepared Foods segment and has taken a toll on the overall productivity.

Tyson incurred $340 million in incremental costs during the third quarter in relation to the COVID-19 pandemic, and the company expects some of these costs to continue at a lower run rate going forward.

Tyson also faces challenges from tariffs which present price disadvantages in many of its markets. The company believes the reduction or removal of tariffs could lead to an acceleration of global demand for US pork, beef and chicken.

Click here to read the full transcript of Tyson Foods Q3 2020 earnings call