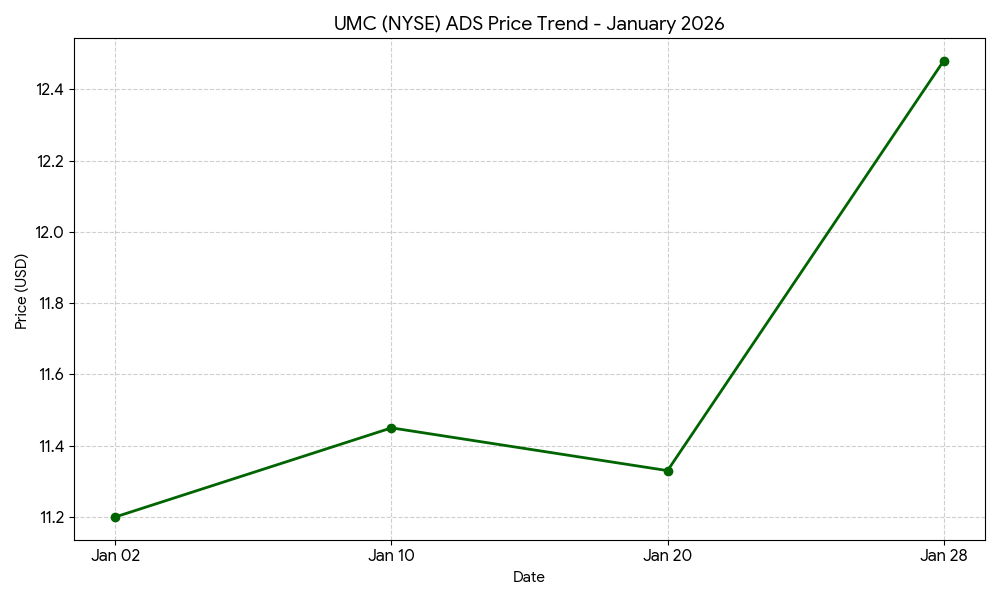

United Microelectronics Corporation (NYSE: UMC; TWSE: 2303), a global semiconductor foundry, saw its shares increase sharply on Wednesday. The company’s American Depositary Shares (ADS) closed at $12.48, representing an intraday increase of 10.15%. The move followed the announcement of the company’s unaudited financial results for the quarter and fiscal year ending December 31, 2025.

Market Capitalization

As of the market close on January 28, 2026, the market capitalization of United Microelectronics Corporation is approximately USD 28.52 billion. In Indian currency terms, this valuation is approximately INR 2,40,430 crore.

Latest Quarterly Results

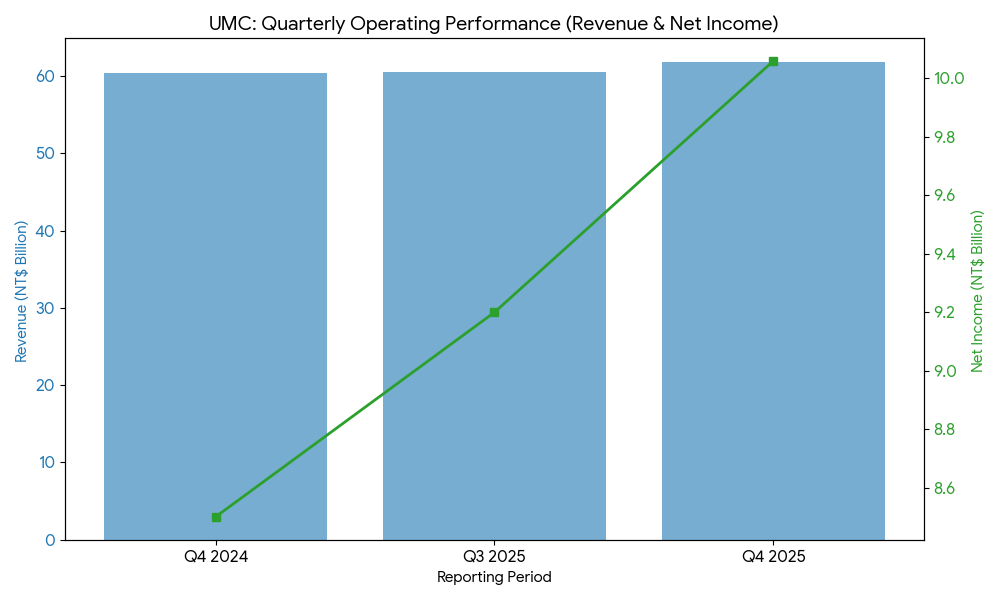

For the three-month period ending December 31, 2025, UMC reported consolidated revenue of NT$61.81 billion ($1.97 billion). This reflects a **2.4% increase** compared to NT$60.39 billion in the fourth quarter of 2024. Net income attributable to shareholders was NT$10.06 billion, an increase from NT$8.50 billion in the prior-year period.

Segment Highlights (Technology Node Revenue Share):

- 22/28nm Nodes: 36%

- 40nm and below: 53% (Cumulative)

- Capacity Utilization: 78%

- Wafer Shipments: 994,000 (8-inch equivalent)

FINANCIAL TRENDS

Full-Year Results Context

For the full fiscal year 2025, UMC reported total consolidated revenue of NT$237.5 billion, a growth of 2.3% from NT$232.3 billion in 2024. Annual net income reached **NT$41.7 billion**, resulting in earnings per share (EPS) of NT$3.34. This represents a directional contraction in earnings from the NT$3.80 reported in 2024, despite the increase in total revenue and a 12.3% rise in annual wafer shipments.

Business & Operations Update

During 2025, UMC completed the Phase 3 facility expansion at its Singapore Fab 12i. In December 2025, the company licensed imec’s iSiPP300 technology to expand its silicon photonics capabilities for high-speed connectivity applications. Additionally, the company reached production milestones in its collaboration with Silicon Storage Technology for embedded SuperFlash memory on the 28nm platform.

M&A or Strategic Moves

UMC is currently executing a 12nm technology collaboration with Intel. The company also announced a Memorandum of Understanding (MOU) with Polar Semiconductor to enhance onshore manufacturing capabilities in the United States. No new acquisitions were disclosed during the fourth-quarter reporting session.

Q&A Focus

The interaction between analysts and management regarding margins highlighted several “moving parts” affecting the company’s bottom line.

- Depreciation Headwinds: CFO Chih-tung Liu addressed concerns over gross margins, citing higher depreciation from recent tool installations as a primary factor for the “high-20% range” guidance for Q1 2026. Depreciation is expected to see a low-teens annual increase throughout 2026.

- Geopolitical and Tariff Risks: Management was asked about the impact of recent global trade policies. They acknowledged that while visibility for the second half of 2026 remains limited due to geopolitical factors, their geographic diversification (particularly the Singapore and U.S. footprints) is designed to mitigate these risks.

Guidance & Outlook

For the first quarter of 2026, UMC management issued guidance anticipating flat wafer shipments and firm average selling prices (ASP). The gross profit margin is projected to be in the “high-20% range” with capacity utilization in the “mid-70% range.” The company has set a 2026 capital expenditure (CAPEX) budget of $1.5 billion, primarily directed toward its Singapore expansion and specialty technology development.

Performance Summary

UMC shares rose 10.15% today as the company reported Q4 revenue of NT$61.81 billion. While annual EPS declined to NT$3.34, the company achieved record revenue from its 22nm platform. Investors are monitoring the 2026 CAPEX plan and the stability of utilization rates across mature nodes.