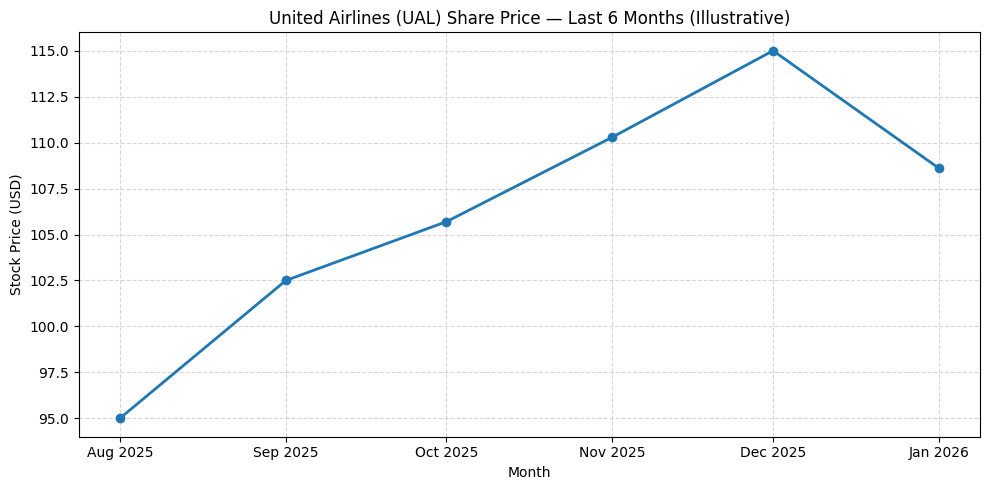

Market Reaction and Share Performance

United Airlines Holdings Inc. shares rose in extended trading on Tuesday after the airline reported fourth quarter earnings that beat analyst expectations and delivered record quarterly revenue. United’s stock was up about 3% to 4% after the results. Over the past 52 weeks, United’s shares have traded in a wide range as travel demand recovered from pandemic lows, with the stock up modestly year-to-date ahead of earnings.

Quarterly Results Overview

United reported fourth quarter 2025 revenue of $15.4 billion, the highest quarterly revenue in company history, up about 4.8% year-over-year. Diluted earnings per share were $3.19, with adjusted earnings per share of $3.10, within its guidance range of $3.00 to $3.50 and above the consensus expected level. Net income for the quarter was approximately $1.0 billion. TRASM (total revenue per available seat mile) fell about 1.6% while capacity rose 6.5% compared with the prior year, reflecting continued network growth and mix changes.

Revenue, Margins and Cash Flow

Fourth quarter pre-tax earnings were about $1.3 billion, with an 8.6% pre-tax margin, reflecting higher unit revenue and disciplined cost control. CASM (cost per available seat mile) declined modestly year-over-year, and CASM-ex (excluding fuel and special items) was slightly higher. United ended the year with $15.2 billion in liquidity, generated $8.4 billion in operating cash flow and $2.7 billion in free cash flow for full-year 2025.

Full-Year Performance

For the full year, United reported $4.3 billion in pre-tax earnings and $10.20 diluted EPS, with adjusted EPS of $10.62, both up versus 2024. Total operating revenue for 2025 was about $59.1 billion, a year-over-year increase and the highest annual figure in company history. Net income for the year was roughly $3.4 billion. The company repurchased about $640 million of shares during the year and maintained net leverage near 2.2x.

Operational Highlights

United said it operated the largest mainline schedule in its history in Q4 and full year 2025, carrying an average of more than 496,000 passengers daily and posting the lowest seat cancellation rate among major U.S. carriers. Premium cabin revenue grew about 9% and loyalty revenue rose around 10% year-over-year in the fourth quarter, offsetting softer performance in cargo.

Network and Customer Metrics

The airline flew a record 181 million passengers in 2025. It also registered its highest quarterly unit revenue of the year, supported by strong demand in premium seating and loyalty programs. United said revenue per available seat mile showed momentum into early 2026.

Capital Allocation and Balance Sheet

United ended Q4 with solid liquidity. It returned capital to shareholders via share repurchases during the quarter and year. The airline also maintained disciplined balance sheet management with total debt and lease obligations near $25 billion at year end.

Outlook and Management Commentary

Management characterized the results as showing “strong revenue momentum” carrying into 2026 and highlighted demand from premium and corporate travelers. The company expects to take delivery of more than 100 narrowbody aircraft and about 20 widebody Boeing 787s in 2026. United also reaffirmed its forecast for 2026 adjusted EPS in the range of $12 to $14 per share as travel trends continue.

Analyst Activity

There were no major analyst upgrades or downgrades tied directly to today’s earnings announcement at the time of writing. Market commentary noted revenue strength amid mixed macro travel trends and cost pressures that affect the broader airline sector.

Sector and Macro Environment

United’s results come as the travel industry contends with mixed global macro conditions, including inflationary costs and shifting consumer demand. Airlines are focused on premium services, loyalty programs, and network optimization to drive unit revenue. Broader macro pressures on discretionary travel and business spending remain important factors for investor assessments.