W. R. Berkley Corporation (NYSE: WRB) reported its fourth-quarter and full-year 2025 results on Monday, January 26, 2026, delivering a 21.4% return on equity and record underwriting income. While the headline figures demonstrate high-level profitability, the underlying data reveals a tactical shift in the company’s risk appetite as it navigates the divergence between primary insurance and reinsurance markets.

Financial Highlights: Robust Returns and Record Underwriting

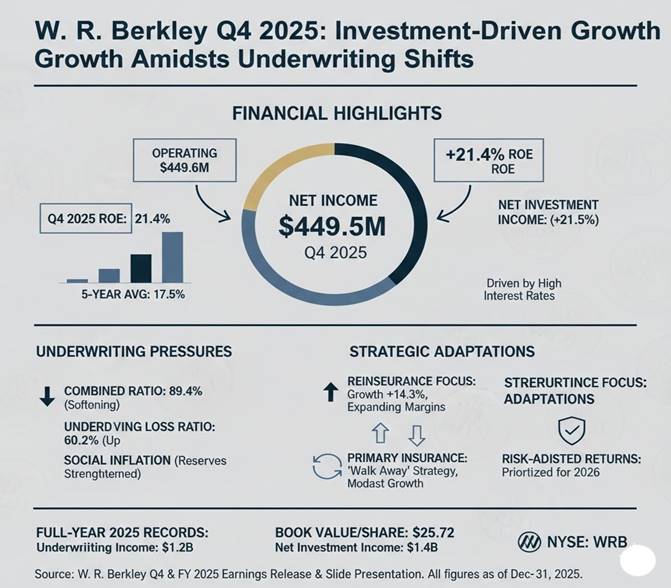

The company reported net income for the quarter of $449.5 million, or $1.13 per diluted share. Although this represented a decrease in net income compared to the $576.1 million reported in Q4 2024, operating income rose to $449.6 million ($1.13 per share), up from $410.4 million ($1.02 per share) in the prior-year period.

For the full year 2025, W. R. Berkley achieved record pre-tax underwriting income of $1.2 billion and record net investment income of $1.4 billion. These results culminated in a full-year net income of $1.78 billion.

Underwriting Strategy: Reinsurance Expansion Amidst Primary Pressures

A central theme of the report was the differing performance across segments. The consolidated combined ratio was 89.4%, a slight improvement from the market’s expectation but a shift from the 87.9% current accident year combined ratio (before catastrophes) seen in late 2024.

The company appears to be reallocating capital toward the Reinsurance & Monoline Excess segment, which saw significant growth, while the primary Insurance segment faced margin pressures. Gross premiums written for the quarter reached $3.6 billion, with net premiums written at approximately $3.0 billion. Management noted average rate increases (excluding workers’ compensation) of roughly 8.4%, though net premiums earned grew at a more modest pace, suggesting a disciplined “walk away” strategy from underpriced primary risks.

Social Inflation and Reserve Integrity

W. R. Berkley reported record pre-tax underwriting income, but results were tempered by the industry-wide challenge of “social inflation.” While property lines and workers’ compensation remained profitable, the company acknowledged the need for reserve strengthening in specific long-tail liability lines due to escalating litigation costs.

The underlying loss ratio (excluding catastrophes) stood at 60.2%, up from 59.4% in the prior year. This reflects the increasing cost of current-year claims, particularly in casualty lines where legal and medical inflation continue to put pressure on margins.

Investment Tailwind and Capital Management

Net investment income reached $385.2 million for the quarter, largely supported by a 21.5% increase in the core fixed-income portfolio. Higher interest rates have allowed the company to reinvest cash at yields exceeding its current book yield, providing a significant buffer for overall earnings.

W. R. Berkley ended the year with a book value per share of $25.72, a 16.4% year-over-year increase. The company continued its trend of aggressive capital return, utilizing share repurchases and dividends throughout 2025 to enhance shareholder value.

2026 Strategic Outlook: Prioritizing Risk-Adjusted Returns

Looking ahead, management remains focused on maintaining a 15% after-tax return on beginning equity. The company’s decentralized structure—operating through 58 independently managed units—is expected to be a primary advantage in identifying niche opportunities while avoiding segments where pricing does not match loss trends. With a cautious stance on primary commercial lines, the company signals that its 2026 growth will likely be driven by segments with the most favorable risk-adjusted pricing, notably in the reinsurance space.