The upcoming earnings report from Walmart Inc. (NYSE: WMT) is expected to offer fresh insight into the health of the broader retail sector and consumer sentiment. As shoppers increasingly balance value with convenience, investors will be watching closely to see whether the company’s scale, pricing discipline, and omnichannel investments continue to provide it a competitive edge in the challenging operating environment.

Q4 Report Due

The retail giant is preparing to report its fourth-quarter FY26 results on Thursday, February 19, at 7:00 am ET. On average, analysts following the business forecast total revenues of $188.58 billion for the quarter, representing a 9.85% increase from the prior-year quarter. The consensus earnings estimate for the fourth quarter is $0.72 per share, on an adjusted basis, compared to $0.66 per share in Q4 2025.

Over the past several months, Walmart’s stock has been in an upward spiral, gaining 25% in 2025. Last week, the shares climbed to a new high. While its dividend yield is modest compared to high-yield stocks, the company has earned its place among dividend kings, with several decades of consistent payout increases. Despite the recent rally, market watchers see more room for growth, and the majority of them recommend buying the stock.

ALSO READ: Highlights of Walmart’s Q3 2026 Earnings Report

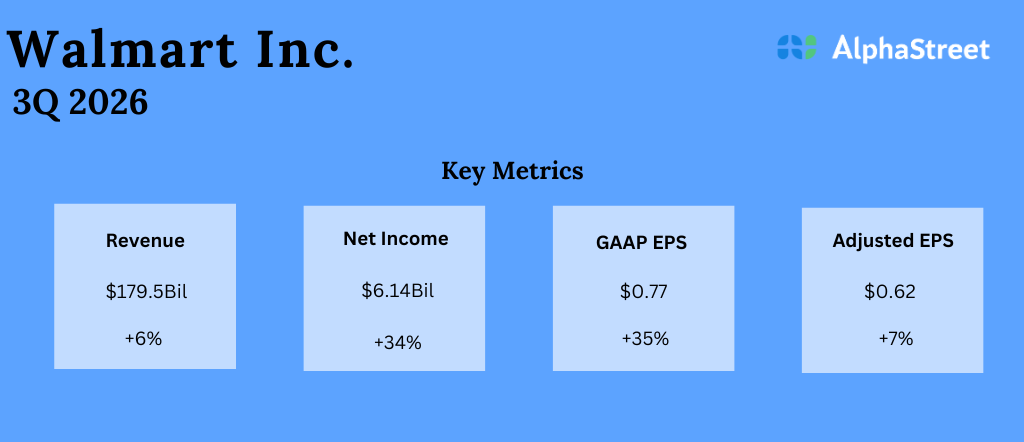

Strong Outcome

In the third quarter, revenues increased 5.8% year-over-year to $179.5 billion, with US comparable sales growing 4.5%. Earnings per share, excluding special items, rose 6.9% annually to $0.62 during the three months. On a reported basis, consolidated net income attributable to the company was $6.14 billion, up 34.2% from the prior-year period. Both revenues and earnings beat Wall Street’s estimates. Buoyed by the positive Q3 outcome, management raised its adjusted earnings guidance for fiscal 2026 to the range of $2.58-$2.63 per share. Full-year sales are expected to grow between 4.8% and 5.1% on a constant currency basis.

Walmart’s CEO, Douglas McMillon, said in the Q3 2026 earnings call, “As we look at our customers and members here in the US, they’re still spending, with upper and middle income households driving our growth. We continue to benefit from higher-income families choosing to shop with us more often. Middle-income households have been steady, and while lower-income families have been under additional pressure of late, we’re encouraged by how our teams are meeting them with greater value across necessities, and doing what we can to help them stretch their dollars further.”

Strategy

As one of the world’s largest retailers, Walmart often serves as a bellwether for consumer spending trends. With household spending patterns continuing to shift, the company’s strategy now emphasizes affordability, private labels, and digital expansion. Walmart’s hybrid model—combining its traditional big‑box strength with e‑commerce innovation—has helped it navigate challenges such as rising competition and inflation‑driven pressure on consumers. The company is also moving into higher‑margin businesses like online ads, memberships, and expanded third‑party seller platforms, underscoring its intent to grow beyond price leadership.

The average price of Walmart’s stock over the past twelve months is $101.62. The stock had a modest opening this week, and the softness continued on Tuesday. The shares were trading down 1.5% in the afternoon.