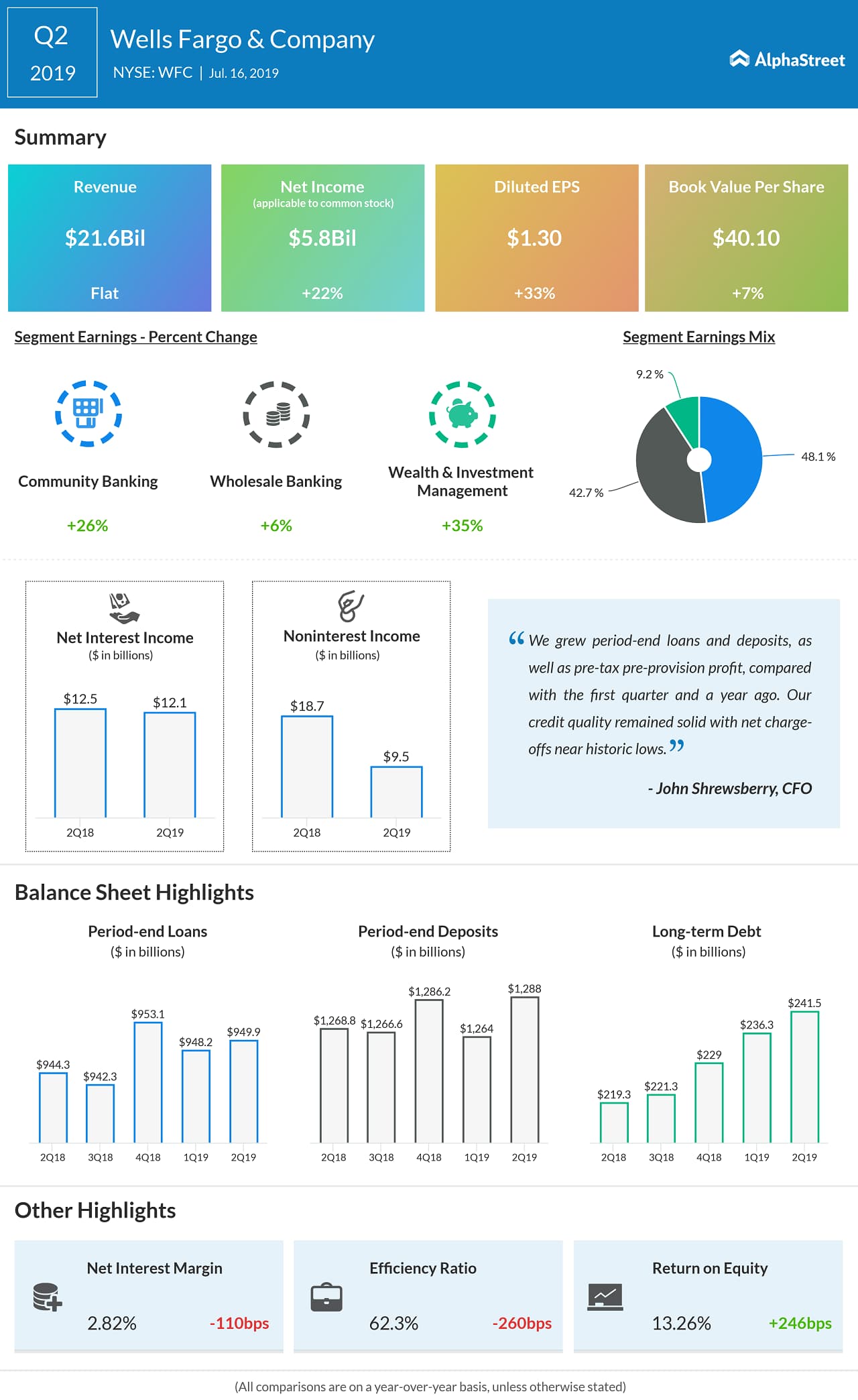

Wells Fargo (NYSE: WFC) reported EPS of $1.30 on revenue of $21.6 billion for its second quarter ended June 30, 2019. The banking firm surpassed the analysts’ views on the bottom line and topline. Wall Street had expected Wells Fargo to post a profit of $1.15 per share on revenue of $20.94 billion. The stock was down about 1% in the pre-market trading hours.

Revenue was flat compared with the prior-year quarter at $21.6 billion due to a decrease in net interest income, which decreased $446 million to $12.1 billion in the second quarter. Higher deposit costs and the lower interest rate environment reduced the net interest income.

“During the second quarter, we formed a new Strategic Execution and Operations Office that will focus on achieving operational excellence across our businesses to enable us to execute more effectively on our regulatory priorities and further drive our transformation,” said Interim CEO Allen Parker.

In June 2019, Wells Fargo received a non-objection to its 2019 capital plan from the Federal Reserve. As part of this plan, the San Francisco-based bank is expected to increase its third quarter 2019 common stock dividend to $0.51 per share, subject to approval by its Board of Directors.

This capital plan also includes up to $23.1 billion of gross common stock repurchases, subject to management discretion, for the four-quarter period from the third quarter of 2019 through second quarter 2020.

Also Read: Goldman Sachs Q2 earnings report

Wells Fargo’s peers JPMorgan Chase (NYSE: JPM) and Goldman Sachs (NYSE: GS) also reported their second quarter 2019 results today. JPMorgan beat quarterly estimates on tax benefit, and Goldman Sachs’ earnings and revenue declined but beat Wall Street’s estimates.

Wells Fargo stock has just advanced 1% in the year-to-date period while it dropped 16% in the past 12 months.