Shares of Lamb Weston Holdings, Inc. (NYSE: LW) were down over 1% on Wednesday. The stock has dropped 7% over the past three months. The frozen potato products maker is scheduled to report its fourth quarter 2025 earnings results on Wednesday, July 23, before market opens. Here’s a look at what to expect from the earnings report:

Revenue

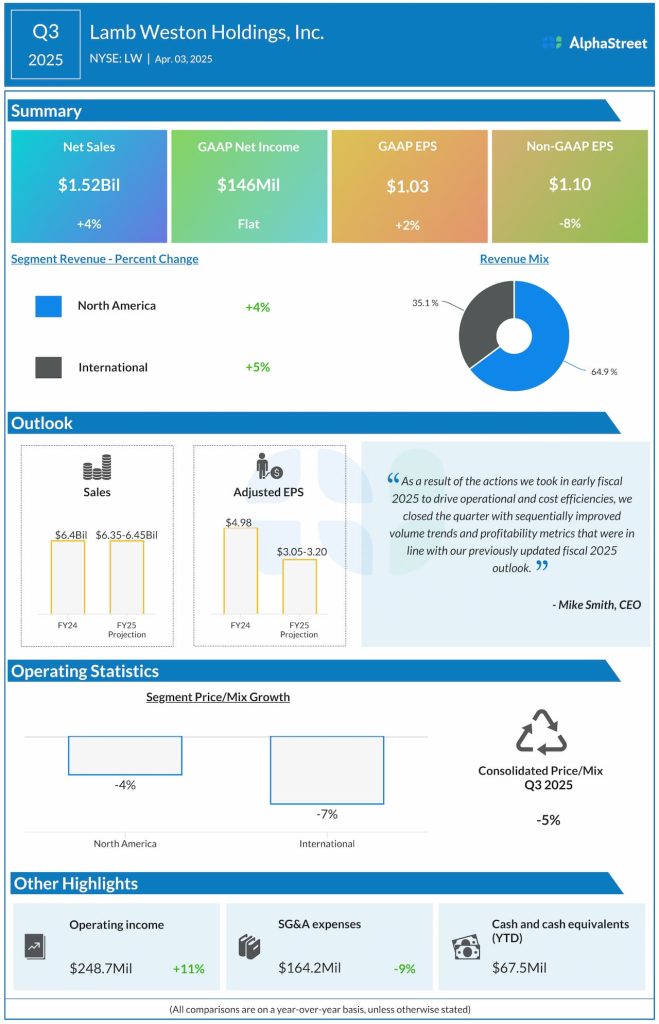

Analysts are projecting revenue of $1.59 billion for Lamb Weston in the fourth quarter of 2025, which indicates a 1% dip from the same period a year ago. In the third quarter of 2025, net sales increased 4% year-over-year to $1.52 billion.

Earnings

The consensus estimate for earnings per share in Q4 2025 is $0.64, which implies a decline of 18% from the prior-year quarter. In Q3 2025, adjusted EPS decreased 8% YoY to $1.10.

Points to note

Lamb Weston continues to operate in a challenging environment with economically pressured customers looking for value. As projected earlier, headwinds from soft restaurant traffic are expected to persist and take a toll on the company’s performance. The majority of LW’s sales in North America come from food-away-from-home channels, mainly quick-service restaurants (QSRs). In the third quarter, QSR traffic in the US was down 2% YoY.

Last quarter, Lamb Weston saw growth in total sales and volume as well as across its segments as it replaced volumes lost in the previous year and gained volumes through customer contract wins. However, softness in restaurant traffic partly offset these gains. Lost QSR customer volume and soft restaurant traffic are anticipated to impact fourth quarter results.

Lamb Weston is focusing on expanding its relationship with its existing customers as well as winning new customers through partnerships and product innovation. These initiatives are anticipated to drive yields over time. In addition, the company’s efforts to rationalize capacity and reduce costs are expected to generate benefits.