Shares of Delta Air Lines Inc. (NYSE: DAL) were up 2% on Friday. The stock has gained 47% year-to-date. The airline company is scheduled to report its second quarter 2023 earnings results on Thursday, July 13, before market open. Here’s a look at what to expect from the earnings report:

Revenue

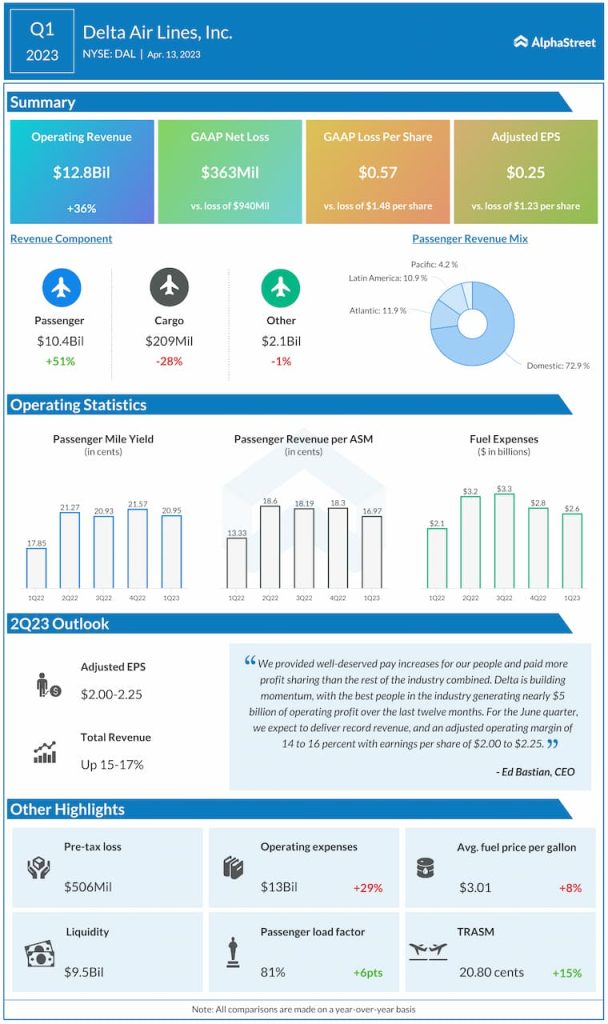

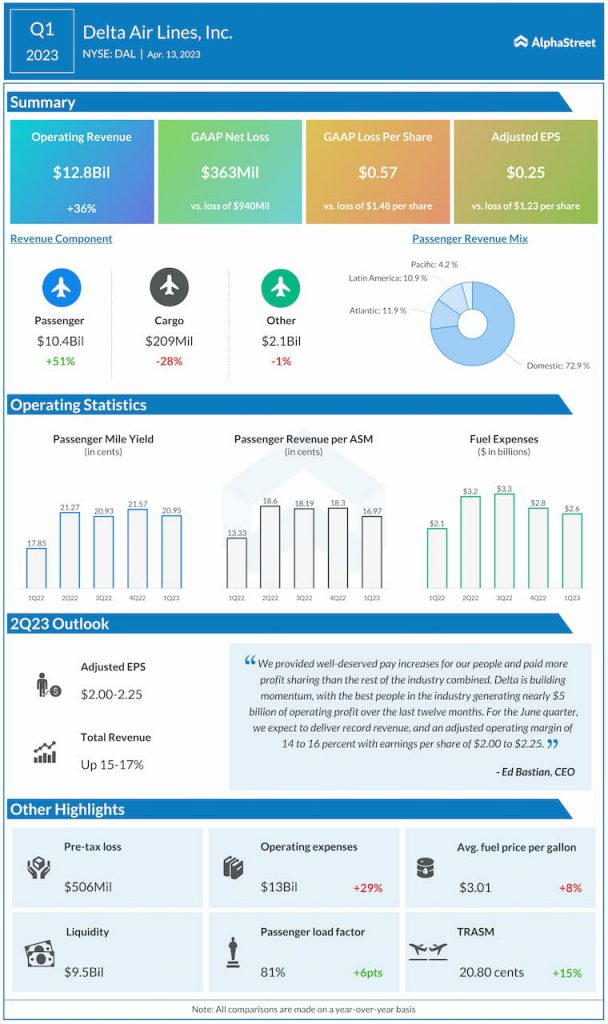

Delta recently raised its revenue forecast for the second quarter of 2023 and currently expects its top line to grow 17-18% year-over-year. Analysts are estimating revenue of $14.4 billion, which would reflect a 17% growth from the same period a year ago. In Q1 2023, GAAP operating revenue grew 36% YoY to $12.8 billion.

Earnings

Delta also raised its earnings guidance for Q2 2023 and now expects EPS to range between $2.25-2.50. Analysts are projecting EPS of $2.36 for the second quarter which compares to EPS of $1.44 in the prior-year period. In Q1 2023, adjusted EPS was $0.25.

Points to note

The demand for air travel continues to be strong. Factors such as strong employment, higher wages and the convenience of the hybrid work model are working in favor of travel demand. In addition, the majority of the airline industry’s revenue is coming from higher-income customers or premium customers. All of these trends benefit Delta.

Delta is seeing a favorable revenue environment. The company expects its unit revenue for the second quarter to be flat to up 1%. Capacity is expected to be up 17% YoY in Q2. There is strong demand for leisure travel among premium customers and the company expects a stable corporate travel environment. Delta is also seeing growth in revenue from its premium products. They are a significant contributor to unit revenues and they are growing steadily.

For the second quarter of 2023, Delta expects operating margin to be 16%. This compares to operating margin of 11% in the prior-year quarter. In Q1 2023, operating margin was down 2.2%. The company expects CASM ex-fuel to increase 1-3% YoY in Q2. In the first quarter, CASM ex-fuel was up 4.7% YoY.