Shares of Dollar General Corporation (NYSE: DG) turned green in midday trade on Wednesday. The stock has gained 16% in the past three months. The discount retailer is scheduled to report its fourth quarter 2023 earnings results on Thursday, March 14, before markets open. Here’s a look at what to expect from the earnings report:

Revenue

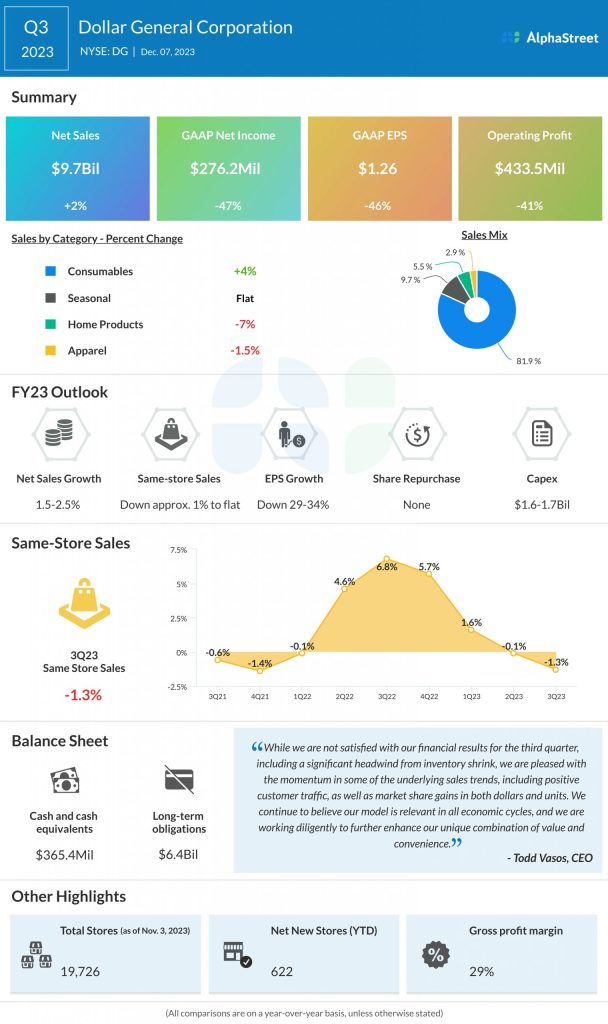

Analysts are projecting revenues of $9.78 billion for the fourth quarter of 2023, which indicates a drop of 4% from the same period a year ago. In the third quarter of 2023, net sales increased 2.4% year-over-year to $9.7 billion.

Earnings

The consensus estimate is for EPS of $1.74 in Q4 2023, which is down from $2.96 reported in the prior-year period. In Q3 2023, EPS decreased 46% YoY to $1.26.

Points to note

Last quarter, Dollar General benefited from sales growth and a rise in customer traffic. In an inflationary environment, customers tend to turn to discount stores for value and this trend will continue to benefit companies like Dollar General. However, same-store sales decreased 1.3% in Q3, mainly due to a drop in average transaction amount.

DG has been seeing a strain on consumer spending, which is likely to have continued in Q4. On its Q3 call, the retailer said it anticipates consumer spending to remain pressured in 2024, mainly in discretionary categories. The consumables category remains stable, with sales growth of 3.6% last quarter.

The company saw margins decline last quarter mainly due to higher shrink and higher discounts. The shift in sales mix towards low-margin consumables has also been impacting margins. These factors are likely to pressure margins in Q4, with shrink remaining a sizable headwind.

Dollar General continues to invest in its store fleet. Last month, the company hit a milestone with the opening of its 20,000th store. The expansion of the store base can help fuel revenue growth. The retailer has guided for 990 new store openings, 2,000 remodels, and 120 store relocations in FY2023.