Shares of Dollar Tree, Inc. (NASDAQ: DLTR) rose more than 1% on Friday. The stock has dropped 17% year-to-date. The discount retailer is slated to report its third-quarter 2023 earnings results on Wednesday, November 29, before market open. Here’s a look at what to expect from the earnings report:

Revenue

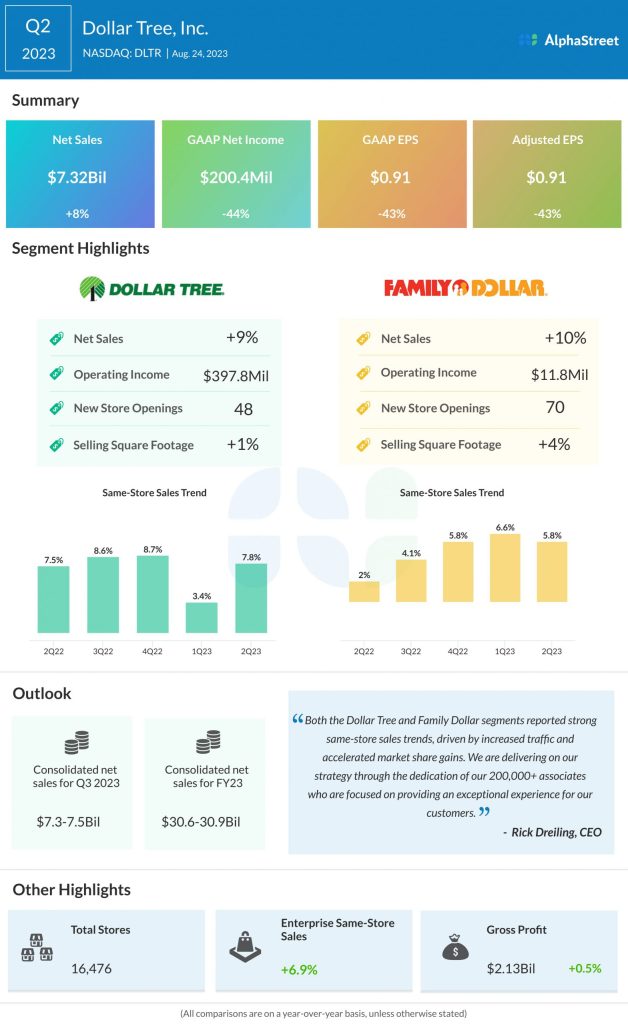

Dollar Tree has guided for consolidated sales of $7.3-7.5 billion for the third quarter of 2023. Analysts are projecting revenue of $7.4 billion for Q3 2023, which would represent a growth of 6.7% from the same period a year ago. In the second quarter of 2023, consolidated sales increased 8% year-over-year to $7.3 billion.

Earnings

Dollar Tree expects earnings for Q3 2023 to range between $0.94-1.04 per share. Analysts are predicting EPS of $1.01 for the third quarter, which compares to EPS of $1.20 reported in the prior-year period. In Q2 2023, adjusted EPS fell 43% YoY to $0.91.

Points to note

For the third quarter, Dollar Tree has forecasted a mid-single-digit increase in same-store sales for the enterprise and for both its segments. Last quarter, enterprise same-store sales rose 6.9%. Same-store sales for the Dollar Tree segment grew 7.8%, helped by a 9.6% rise in traffic, but was partly offset by a drop in average ticket. The Family Dollar segment saw same-store sales growth of 5.8%, driven by increases in traffic and average ticket.

Dollar Tree is expected to benefit from traffic growth as its price position and merchandising efforts help it cater well to customers seeking value. The retailer has seen strong growth in the consumables category which has helped offset the softness across discretionary categories. These positive trends have led to strong market share gains.

DLTR’s private brands are gaining traction among value-conscious customers. The expansion and improvement of its private brands assortment provide the company with a significant growth opportunity. In addition, Dollar Tree’s investments in its stores with new store openings and store renovations, as well as its merchandising initiatives are expected to drive benefits for the company.

At the same time, margins remain a concern. Last quarter, the retailer’s gross margin was impacted by a shift in sales mix towards low-margin consumables, as well as product cost inflation and elevated shrink. The company expects the shift in sales mix and unfavorable shrink trends to continue through the remainder of the year, which does not bode well for third-quarter margins.