Shares of General Mills, Inc. (NYSE: GIS) stayed green on Wednesday. The stock has gained 18% over the past 12 months. The processed foods company is scheduled to report its fourth quarter 2023 earnings results on Wednesday, June 28, before market open. Here’s a look at what to expect from the earnings report:

Revenue

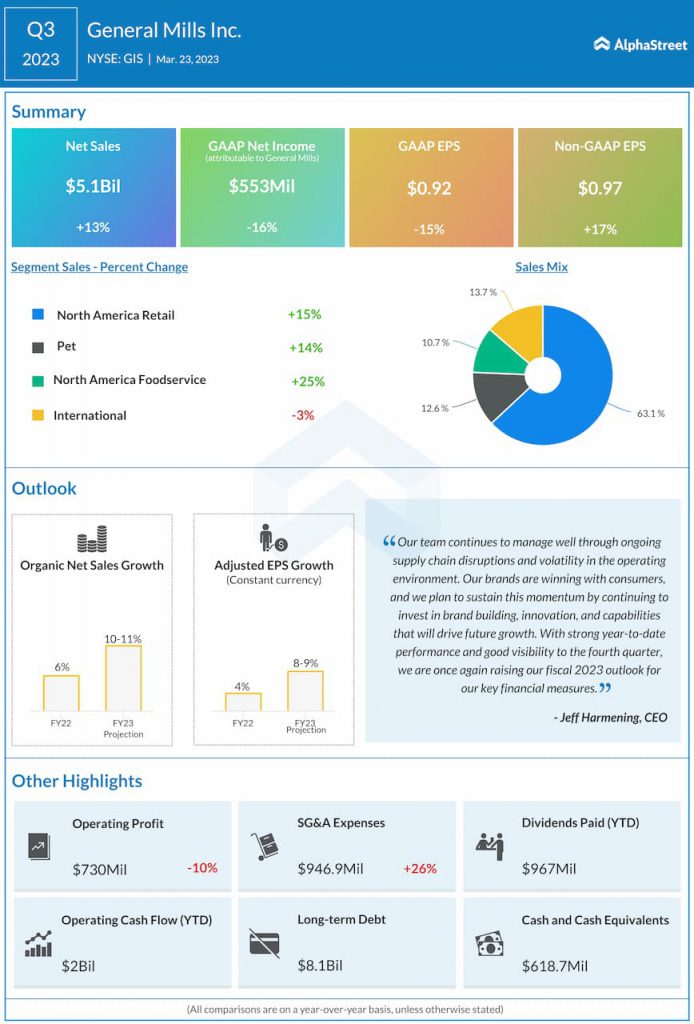

Analysts are projecting revenue of $5.17 billion for the fourth quarter of 2023, which would reflect an increase of over 5% from the same period last year. In the third quarter of 2023, net sales increased 13% year-over-year to $5.1 billion.

Earnings

The consensus estimate is for earnings of $1.06 per share in Q4 2023 which compares to $1.12 per share in the year-ago period. In Q3 2023, adjusted EPS rose 17% to $0.97.

Points to note

In Q3, General Mills’ top line benefited from price realization and mix. The company saw sales growth across most of its segments, with gains in Retail, Pet and Foodservice. The North America Retail segment benefited from growth in US Meals and Baking Solutions, US Snacks, and US Morning Foods while the Pet segment saw gains in dry dog and cat food, as well as dog treats. This momentum is likely to have continued into the fourth quarter.

The company’s progress in driving its Accelerate strategy is also likely to benefit its business performance. General Mills has been investing in its brands and business and reshaping its portfolio in order to drive growth. It has also been focusing on product innovation which has helped drive retail sales growth. The company has been trying out new products in the cereal and ice cream categories as well as new pet products like fresh dog food offerings and human-inspired pet treats.

General Mills’ gross margin in Q3 rose 160 basis points benefiting from net price realization and mix. This was partly offset by higher input costs. Operating profit dropped 10% YoY due to higher SG&A expenses and operating profit margin was down 380 basis points. The company has been undertaking pricing and productivity initiatives to help in margin recovery, which may have benefited it in the fourth quarter.