Shares of McCormick & Company, Incorporated (NYSE: MKC) gained over 1% on Monday. The stock has dropped 7% over the past three months. The condiments maker is slated to report its second quarter 2025 earnings results on Thursday, June 26, before market open. Here’s a look at what to expect from the earnings report:

Revenue

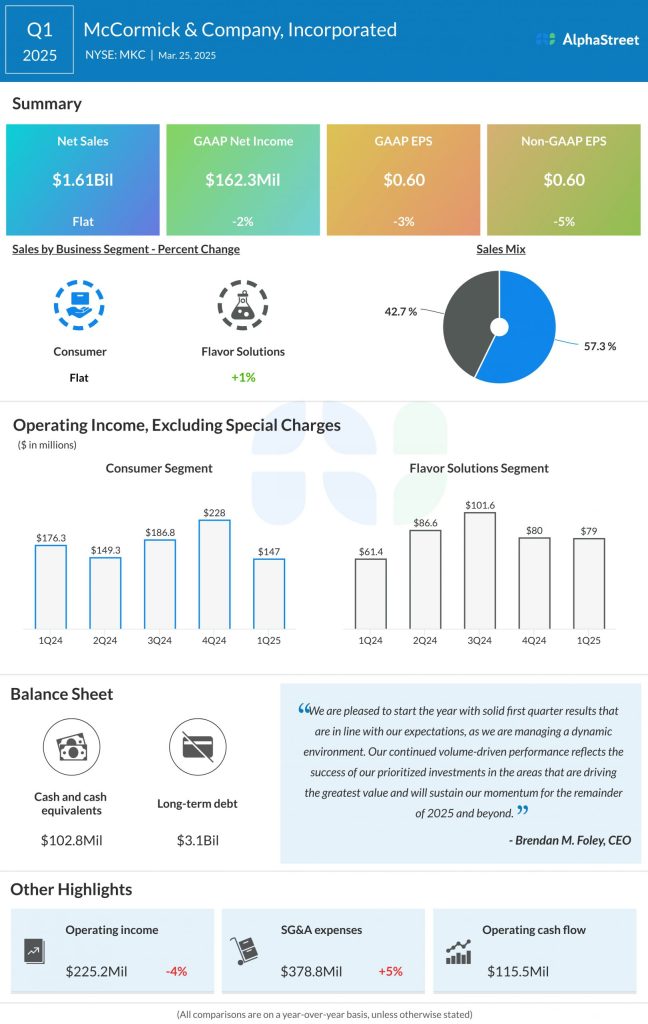

Analysts are projecting revenue of $1.66 billion for McCormick for the second quarter of 2025. This implies a 1% rise from the same quarter a year ago. In the first quarter of 2025, net sales remained flat year-over-year at $1.60 billion.

Earnings

The consensus target for earnings per share in Q2 2025 is $0.66, which indicates a decline of 4% from Q2 2024. In Q1 2025, adjusted EPS decreased 5% YoY to $0.60.

Points to note

McCormick continues to operate in a challenging macro environment with consumers seeking value and tightening their budgets as they deal with economic uncertainty and rising costs. In addition, consumers are becoming more health-conscious. These trends have led to a rise in more at-home cooking and an increase in demand for flavor.

The company is working on launching new products or innovating existing ones to meet consumers’ needs for healthy options. It is focusing on areas where it sees maximum growth potential. These factors can be expected to drive momentum in the second quarter.

At the same time, MKC is seeing softness with some of its CPG customers and QSR customers. The foodservice industry is facing headwinds from slow traffic. These challenges are likely to have continued in the to-be-reported quarter.

Although MKC is expected to see an increase in SG&A expenses, it is also expected to benefit from cost savings from its CCI program. These cost savings are anticipated to help boost margins as well.