Shares of McCormick & Company, Incorporated (NYSE: MKC) stayed green on Thursday. The stock has gained 13% year-to-date and 31% over the past three months. The spices and condiments maker is scheduled to report its second quarter 2023 earnings results on Thursday, June 29, before market open. Here’s a look at what to expect from the earnings report:

Revenue

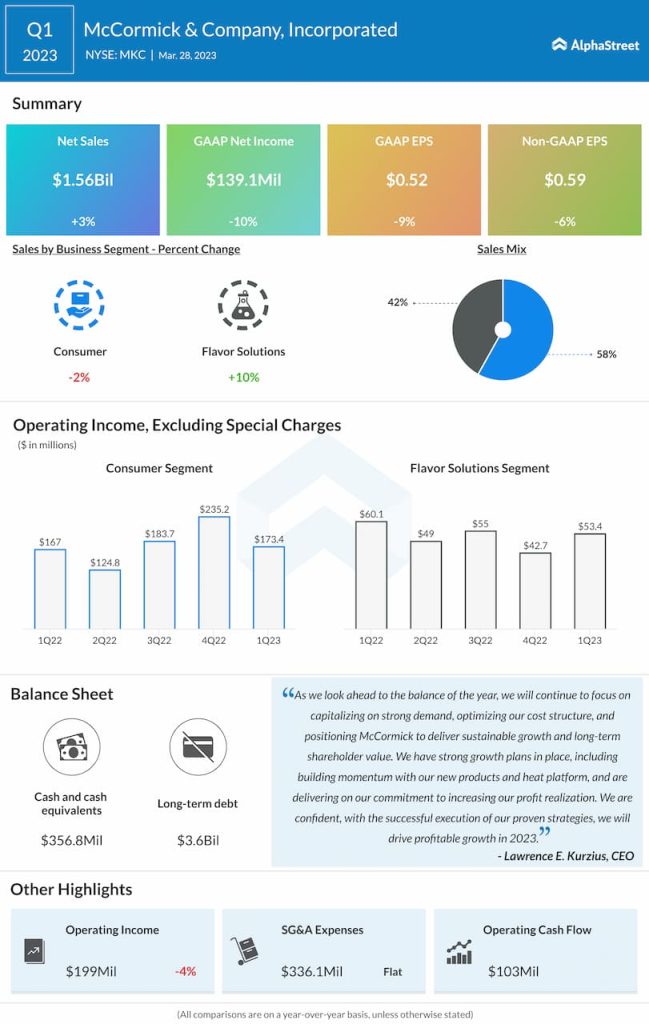

Analysts are projecting revenue of $1.67 billion for the second quarter of 2023, which would reflect a growth of over 8% compared to the same period last year. In the first quarter of 2023, sales increased 3% year-over-year to $1.56 billion.

Earnings

The consensus estimate is for earnings of $0.56 per share in Q2 2023, which would represent a 17% growth from the year-ago quarter. In Q1 2023, adjusted EPS was $0.59, down 6% YoY.

Points to note

During the first quarter, McCormick’s sales benefited from pricing actions although declines in volume and product mix caused a slight dent. The top line was also impacted by the Kitchen Basics divestiture, the exit of the Consumer business in Russia, and lower consumption in China due to COVID. The company expects sales to continue to benefit from pricing actions as well as the strength of its brand portfolio through the year. This bodes well for the second quarter results.

Consumers are giving more preference to healthy and flavorful cooking and McCormick is working to meet this demand through new and varied products. This is expected to have a positive impact on the business performance as well.

In Q1, the Flavor Solutions segment witnessed strong sales growth with gains across all geographic regions. The Consumer segment saw growth in the Americas although its overall results were impacted by the Kitchen Basics divestiture, the exit from Russia and the weakness in China. McCormick expects the Consumer business to pick up growth from the second quarter as it laps the impacts of these factors and the momentum to continue in the Flavor Solutions segment.

McCormick has been able to generate meaningful cost savings from its Comprehensive Continuous Improvement (CCI) and Global Operating Effectiveness (GOE) programs. These helped offset some of the impacts to gross margin from higher costs in Q1. Cost savings from these programs are expected to help mitigate inflationary impacts and aid margin recovery.