Shares of Starbucks Corporation (NASDAQ: SBUX) stayed red on Monday. The stock has dropped 8% in the past three months. The coffeehouse chain is scheduled to report its earnings results for the fourth quarter of 2025 on Wednesday, October 29, after market close. Here’s a look at what to expect from the earnings report:

Revenue

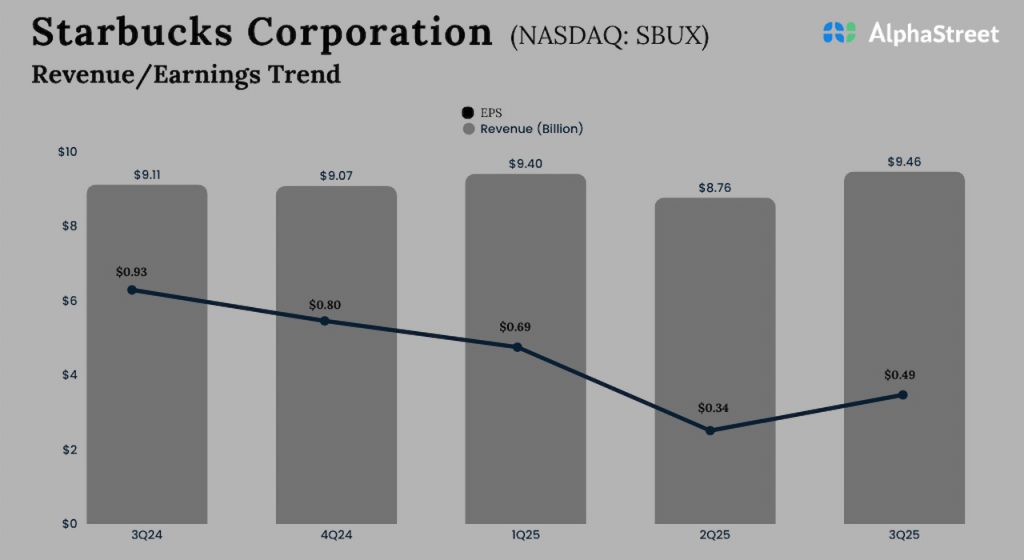

Analysts are projecting revenue of $9.37 billion for Starbucks in the fourth quarter of 2025, which implies a 3% growth versus the prior-year period. In the third quarter of 2025, total revenues increased nearly 4% year-over-year to $9.45 billion.

Earnings

The consensus estimate for earnings per share in Q4 2025 is $0.56, which points to a 30% decline from the year-ago quarter. In Q3 2025, adjusted EPS decreased 46% YoY to $0.50.

Points to note

Starbucks has been seeing a continued decline in its comparable store sales driven by slow traffic, especially in the North America segment and its largest market, the US. The drop in transactions were partly offset by a rise in average ticket. Meanwhile, the International segment has seen a rise in transactions which were, however, offset by a drop in average ticket.

The company continues to make progress on its Back to Starbucks strategy, with gains from Gen Z and millennial customers, and improvements in full-day transaction comps and positive morning transactions. Its in-cafe, drive-thru, and digital businesses are performing well, and it is seeing growth in its delivery business, which recorded a 25% growth in transactions YoY in Q3. It is also making progress in menu innovation.

SBUX is working on uplifting its coffeehouses and has planned for at least 1,000 uplifts across North America by the end of calendar year 2026. These uplifts are expected to improve customer experience and drive growth. As part of its turnaround efforts in North America, the company announced plans to reduce its store count by around 1% and eliminate around 900 non-retail partner roles in the region.

Meanwhile, the International business is performing well with momentum across regions like the UK, Europe, Middle East and Africa (EMEA), Turkey, and Latin America. The company sees significant opportunity for growth in its international markets.

Due to the dynamic consumer environment, Starbucks remains cautious about any significant changes in its US business in Q4 and believes the benefits from its Back to Starbucks strategy will become more evident in 2026. Tariffs and coffee prices remain causes for concern. The company’s margins are expected to remain pressured by its growth investments in the near term.